Dynasty Trust

Summary:

As the name suggests, a dynasty trust allows individuals with significant wealth to provide for multiple generations of descendants.

Typically, a dynasty trust is (a) structured to last the maximum term permitted by law (in perpetuity in some states) allowing trust assets to remain un-depleted by transfer taxes for the entire term of the trust, (b) irrevocable and includes a spendthrift provision which protects trust assets from spendthrift beneficiaries, ex-spouses, and unforeseen creditors and lawsuits, and (c) funded with amounts that take full advantage of the grantor's gift and estate tax basic exclusion amount and generation-skipping transfer (GST) tax exemption.

The result: the depletion of trust assets is minimized, asset growth potential is maximized, and principal is preserved to benefit future heirs.

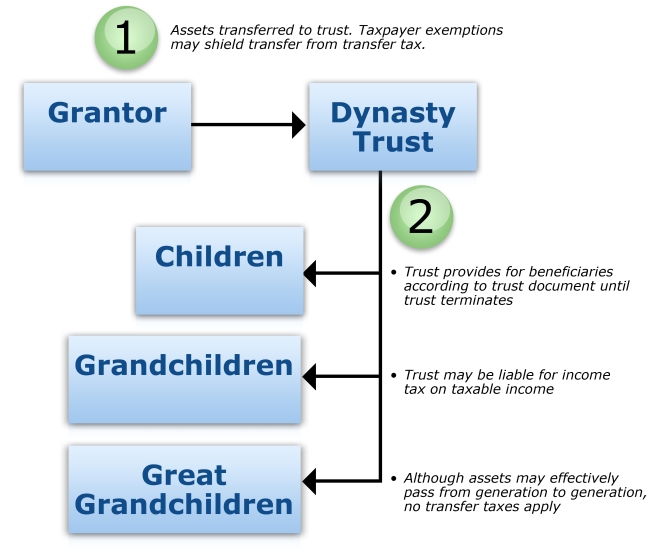

What is a dynasty trust?

Each time one taxpayer transfers wealth to another, the transfer is potentially subject to federal transfer taxes, including gift and estate tax. The federal transfer tax system is designed to impose a tax on each and every generation (e.g., father to son, son to grandson, etc.). The transfer tax system accounts for the fact that a transfer might "skip" a generation by passing from parent to grandchild, for example. This is accomplished by imposing an additional tax whenever transfers of wealth are made to persons who are more than one generation below the taxpayer (e.g., father to grandson). This additional tax is called the generation-skipping transfer (GST) tax. GST tax is imposed at the highest estate tax rate in effect at the time of the transfer.

Additionally, many of the individual states impose their own transfer taxes. Together, these taxes can take an enormous bite whenever wealth is being handed down, and eventually eat away a family's fortune. This can be troublesome to individuals with substantial wealth who would prefer to have their legacies benefit their own family members. It's from these circumstances that the dynasty trust evolved.

A dynasty trust is created to provide for future generations while minimizing overall transfer taxes. With a dynasty trust, a taxpayer transfers assets to the trust. This transfer, from the taxpayer (the grantor) to the trust, is potentially subject to transfer taxes (although the taxpayer may use his or her gift and estate tax basic exclusion amount and GST tax exemption to shield the transfer from tax). The trust then provides for future generations for as long as it exists. Although the trust assets effectively move from generation to generation, there are no corresponding transfer tax consequences.

How does a dynasty trust work?

Structuring the trust to last for generations

At one time, the laws of all 50 states prohibited a trust from lasting beyond 21 years after the death of the last beneficiary alive at the time the trust was created. This rule against perpetuities has been modified or abolished in many states. A trust created in one of those jurisdictions can be structured to last for many generations. Even in states that still maintain the rule, a trust can be created that will last for a substantial period of time.

Leveraging tax advantages

Although assets will be subject to transfer taxes when initially funding the trust, the assets (and subsequent appreciation) will be untouched by transfer taxes for as long as they remain in the trust.

Typically, dynasty trusts are funded with amounts that take full advantage of the grantor's gift and estate tax basic exclusion amount and GST tax exemption. The federal gift and estate tax basic exclusion amount is $13,990,000 (in 2025, $13,610,000 in 2024), and the GST tax exemption is also $13,990,000 (in 2025, $13,660,000 in 2024). These amounts can be doubled if both spouses are funding the trust. Though dynasty trusts can be created at death through a will or living trust, it may be more advantageous to create this type of trust during the grantor's life because, if planned properly, the trust can continue to be funded transfer tax free with annual exclusion gifts ($19,000 (in 2025, $18,000 in 2024) per trust beneficiary).

As this type of trust is taxed more heavily on income, it may be more advantageous to fund the trust with non-income-producing property, such as growth stocks, tax-exempt bonds, and cash value life insurance. Other appropriate assets might include real estate, discounted property, and property expected to highly appreciate.

Protecting and preserving principal

To enjoy the tax benefits summarized above, access to trust property by the beneficiaries must be limited. The grantor can decide how narrow or broad the beneficiary's access will be within those limits. For example, a grantor who wishes to give a beneficiary as much control as possible can name the beneficiary as trustee, and give the beneficiary the right to all income and the right to consume principal limited by the ascertainable standards (i.e., health, education, maintenance and support). The beneficiary can be given even more control by granting a special (or limited) testamentary power of appointment (i.e., the power to name successive beneficiaries, but not to himself/herself, his/her creditors, his/her estate, or the creditors of his/her estate).

On the other hand, a grantor who wants to restrict access to the trust as much as possible can name an independent trustee who has sole discretion over distributions coupled with a spendthrift provision. The trustee will have full authority to distribute or not distribute income or principal to the beneficiary as the trustee deems appropriate. The spendthrift provision will prevent the beneficiary from voluntarily or involuntarily transferring his or her interest to another before actually receiving a distribution.

The greater the restrictions, the less likely creditors or other claimants will be able to reach trust property.

Suitable clients

- High net worth individuals

- Individuals with family heirloom assets (e.g., vacation home or jewelry) or who desire to keep assets within the family for more than one generation

Example

John and Mary, a married couple, own property with a net value of $10 million, which they would like to pass on to their children and future generations. John and Mary's financial planner describes the following three scenarios:

- Scenario 1 --John and Mary leave $10 million outright to their two children.

- Scenario 2 --John and Mary leave $10 million to a trust for the benefit of their two children and then distributed to grandchildren.

- Scenario 3 --John and Mary leave $10 million to a dynasty trust created in a state that has no rule against perpetuities.

Assume that a generation is 26 years, the estate basic exclusion amount and the GST tax exemption are $6,995,000, the estate tax rate is 40%, the growth rate is 7%, principal is not spent, and state variables and income taxes are ignored.

In scenario 1, $10 million passes to John and Mary's children free from estate taxes. In 26 years, the money grows to approximately $58 million, but after estate taxes are deducted, John and Mary's grandchildren receive approximately $40 million.

In scenario 2, $10 million passes to the trust free from estate taxes. In 26 years, the money grows to approximately $58 million and is distributed to John and Mary's grandchildren.

In scenario 3, $10 million passes to the dynasty trust free from estate taxes. In 26 years, the money grows to approximately $58 million. 26 years later, the money grows to approximately $337 million that can provide benefits to John and Mary's great-grandchildren and beyond.

Of course, this is a hypothetical illustration only, and is not indicative of any specific investment.

Advantages

- Can be structured to preserve family wealth for generations

- Minimizes transfer taxes

- Can be structured to protect assets from spendthrift beneficiaries, spousal divorce claims, and unforeseen creditors and claimants

Disadvantages

- Trust is irrevocable

- Leaves future generations with limited flexibility to manage changes in circumstances