GLENN CURTIS

Feb. 27, 2020

People approaching retirement age with little in savings may have a bumpy road ahead. But certain steps can build a nest egg as rapidly as possible to ensure at least some money will be there for support in retirement.

1. Fully Fund Your 401(k)

An employee in this age category who is offered a 401(k) at work should consider funding it to the maximum amount. To provide you with a sense of how powerful maxing out a 401(k) can be, consider the following:

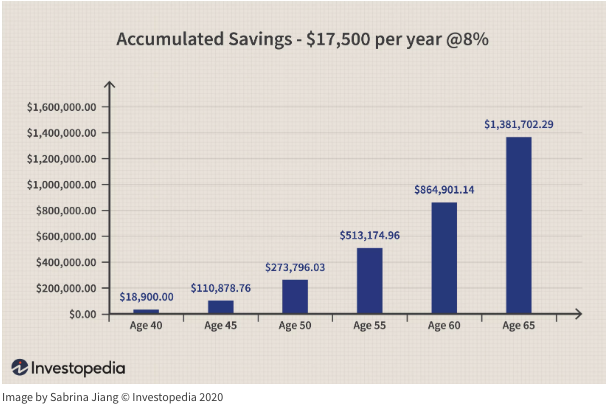

An individual who is 40 years old and who contributes $17,500 annually to a 401(k) could accumulate more than $1.3 million in savings by age 65. This assumes an 8% return and no employer contributions (see the figure below). That's a powerful savings tool, and it's evidence that workers nearing retirement should seriously consider funding their 401(k)s as soon and as much as possible. If this individual increases savings by a catch-up amount of $5,500 at age 50, this would lead to an additional $271,000 in savings. Note that for 2020, these figures are $19,500 and $6,500 (catch-up) for a total of $26,000 and even more earnings potential.

"Factoring in no growth at all, if you can sock away $24,000 a year from age 50 to age 60 (11 years), that’s $264,000 more saved for even the earliest unpenalized retiree. An extra $250,000-plus saved prior to retiring can make or break an income-producing portfolio lasting throughout retirement," says Martin A. Federici, Jr., AAMS®, MF Advisers, Inc., Dallas, Pennsylvania.

2. Contribute to a Roth IRA

Roth IRAs offer investors a great way to save and grow money on a tax-deferred basis. There are some income limitations. For 2020, for example, if you are single and your modified adjusted gross income (MAGI) is $124,000 or more a year, your contribution limit is reduced; if you are single and your MAGI is $139,000 or more your contribution limit is nil. For married folks filing jointly, there are contribution limitations for those with MAGI of $196,000. And at or above $206,000, the contribution limit is nil. (The figures for 2020 are $124,000 to $139,000 for singles; $196,000 to $206,000 for married filing jointly)

How much can one potentially sock away with a Roth? Consider the following example:

A 40-year-old who invests $6,000 each year (the 2020 limit) and obtains an annual rate of return of 8% has the potential to accumulate more than $473,726 by age 65. Even a person who waits until age 50 and starts saving $6,500 per year (using the same return assumptions) can save as much as $190,000 by age 65.

A fully funded Roth IRA and 401(k) can help to rapidly build retirement assets.

3. Consider Home Equity

While a home should not usually be considered a primary source of retirement income, it can provide liquidity during retirement. To that end, older individuals might consider borrowing against the equity in their homes in order to fund living expenses. "A large portion of the population has most of their wealth tied up in real estate properties. This can be used in many ways to fund retirement. You can use the home equity line (HELOC) to draw from when needed, or you could sell, downsize and live off the equity. Whatever you choose, it is important to consider the impact on your monthly income. People are living longer than decades ago, so it is important to make sure you can have a sustainable income for many years to come," says Kirk Chisholm, wealth manager at Innovative Advisory Group in Lexington, Massachusetts.

A reverse mortgage may make sense because lending institutions may shorten repayment periods and increase repayment amounts for older borrowers. Selling a primary residence outright and moving to a smaller and less costly home may also make sense for older individuals. In many cases, they no longer need a big house, as children are usually off on their own.

However, selling a home should not be taken lightly. After all, in many instances, it takes the homeowner 30 years to accumulate full equity ownership in the house. Therefore, it would be a shame not to obtain the largest amount possible from a sale.

That said, individuals should consider current market conditions and whether it is the most advantageous time to sell. Naturally, homeowners should also consider any tax consequences. Married homeowners who file a joint tax return can generate profits of up to $500,000 without owing federal tax on capital gains. For single individuals, the limit is $250,000. This is assuming that you meet certain requirements: The home being sold must be your primary residence and you must not have benefited from the capital gains exclusion on another home during the past two years. Additional requirements are explained in IRS Publication 523, available from the IRS.

Finally, if you're not just moving to a smaller place in your own neighborhood, factor in the cost of living in the area you might be relocating to before making the decision. In other words, it's wise to make sure that real estate prices and the cost of everyday items like groceries are generally lower than where you live now.

4. Take Your Deductions

It's important to note that standard deductions aren't for everyone. In fact, if you have a large amount of mortgage interest, deductible taxes, business-related expenses that weren't reimbursed by your company, and/or charitable donations, it probably makes sense to itemize your deductions.

Sit down with a CPA and go over your personal situation to determine whether it makes sense to itemize. Then get in the habit of saving receipts and keeping good records. Remember, in the end, it's not always what you make, but what you save that counts – particularly as you get closer to retirement.

5. Tap Into Cash Value Policies

While tapping an insurance policy for its cash should be considered a last resort, if the original need for the insurance is no longer there, it may make sense to cash out. However, before ever canceling any policy or accessing its cash value, you should first consult a tax advisor and an insurance professional to review your individual needs.

6. Get Disability Coverage

Don't forget to either obtain disability coverage or make certain that your job offers some sort of group disability benefit. The idea behind obtaining such coverage is simple: to protect yourself and at least a portion of your income and nest egg just in case the worst should happen.

Your chances of becoming disabled depend on your career and your lifestyle, but according to data released by the U.S. Census Bureau in 2019, approximately 40.7 million Americans report some level of disability. That's a substantial number—12.7% of "the U.S. civilian non-institutionalized population," according to the report. It means that in order to protect your income and improve the chances that you will retire with some form of a nest egg, it makes sense to at least consider some form of disability coverage.

"Disability insurance is important to protect your savings," says Elyse Foster, CFP®, Harbor Financial Group, Inc., Boulder, Colo. "Contact your employer or professional association for the most cost-effective options."

The Bottom Line

Individuals in their 40s and 50s who have done little or no retirement planning are certainly at something of a disadvantage. However, with the proper planning and a willingness to save and invest, the odds are not insurmountable.