David Rodeck

Nov. 2, 2023

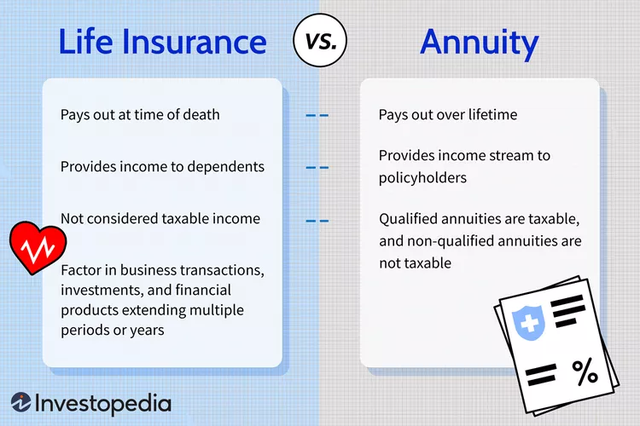

Annuity vs. Life Insurance: An Overview

At first glance, life insurance and annuities might seem like opposites. Life insurance is primarily used to pay your heirs when you pass away. An annuity grows your savings and pays you income while you’re still alive. However, some life insurance policies let you build savings while alive,

and annuities can include a death benefit payment. Here’s how these two options compare and when each makes sense.

KEY TAKEAWAYS

- Life insurance and annuities both allow individuals to invest on a tax-deferred basis.

- Life insurance pays an individual's loved ones after they die.

- Annuities take payments upfront and turn them into future income, including the option of guaranteed income for life.

- Both annuities and life insurance have several options to grow your savings.

- Life insurance is better for leaving an inheritance, while annuities have more investment and income guarantees.

Investopedia / Sabrina Jiang

Annuity

Annuities are a type of insurance contract designed to turn your money into future income payments. You buy an annuity with either one lump sum payment or many payments over time. You can set up the annuity with a growth period, where it builds your savings. The return depends on the type of annuity. For example, a fixed annuity pays a guaranteed interest rate. A variable annuity lets you invest your savings in mutual funds.

When you’re ready, you can start collecting income payments from the annuity. You can set these payments up over a fixed period or have them guaranteed to last for the rest of your life. For this reason, annuities can be a form of insurance against living too long and running out of money.

You can set up a death benefit on an annuity contract. With this feature, the annuity would give your heir a payout based on the contract terms and your balance. For example, if you bought an annuity for $500,000 and collected $300,000 of income payments, the annuity death benefit might pay the remaining $200,000 to your heirs.

Life Insurance

With a life insurance policy, you sign up for a certain size death benefit. If you pass away while covered, your heirs receive this death benefit. There are different types of life insurance policies. Term life insurance only provides the death benefit. It’s also temporary and expires after a set number of years.

Permanent life insurance policies can last your entire life. Permanent policies also build cash value, money you can take out while you're alive. Your cash value earns a return that can grow over time. The return depends on the type of policy. A whole life insurance policy pays a fixed interest rate. A variable life insurance policy lets you invest in subaccounts, like mutual funds, and your growth depends on how your investments perform.

Through cash value, you can use life insurance to save for future goals like retirement. You can then withdraw or borrow against the cash value using a policy loan.

Important: The younger you are, the lower your premiums will be, but older people can still purchase a life insurance policy.

Health Underwriting to Qualify

Most life insurance policies require you to take a medical exam and pass health underwriting to qualify for a policy. If you have health issues, life insurance costs more. You could even be denied a policy altogether. For this reason, building savings through life insurance cash value is generally more effective if you buy a policy when you are younger and healthier.

Annuities do not require health underwriting. You are guaranteed to qualify. You just need to have money to buy the contract.

Policy Benefits

Life insurance is more effective at creating an inheritance for your heirs. Your premiums can turn into a much larger death benefit. Your heirs also receive the life insurance death benefit income-tax-free. Annuity death benefits are smaller relative to life insurance. Your heirs would also owe income tax on your annuity investment earnings.

Annuities offer better investment and income benefits while you’re alive. Your return is higher because you aren’t also paying for life insurance coverage. Instead, all the money is put toward an investment. Annuities also offer more income options, like guaranteed income for life. Life insurance does not.

Taxes

Both life insurance and annuities delay taxes on your earnings while the money stays in the contract. With life insurance, you can withdraw up to what you paid in premiums tax-free. If you withdraw your gains, you owe income tax on them.

You can also take out your cash value through a loan. You do not owe income tax for policy loans. However, the insurer will charge interest on your outstanding loan. You can decide never to pay off the policy loan with the plan that the death benefit will pay it off when you die. That way, you never owe income tax on your cash value gains.

Annuity taxes depend on how you bought the contract. If you purchased the annuity using pre-tax retirement funds, like from a 401(k) or Individual Retirement Account (IRA), then your future income payments are 100% taxed as income.

Note: If you bought the annuity using after-tax dollars, your future income payments will be a combination of a tax-free return of your premiums and taxable gains. Your insurance company would tell you how much of each annuity payment is taxable.

Early Access to Your Money

Life insurance is better for early access to your money, especially if you might need the money before retirement. Once you have cash value, you can withdraw or borrow it at your convenience. There are no age requirements for when you can take out the money.

With an annuity, you agree to keep your money in the contract for a minimum number of years. If you make a large lump sum withdrawal or cancel before the agreed date, the insurance company will deduct a sizable surrender fee. The annuity might allow you to withdraw a specific amount with no penalty, such as 10%, but not the rest.

If you are younger than 59½ when you cancel or make a lump-sum withdrawal, the IRS will also charge a 10% early withdrawal penalty and income tax on your gains. Because of these taxes and penalties, annuities are best used as long-term retirement planning investments.

Can I Convert My Life Insurance to an Annuity?

You can convert your life insurance to an annuity if your life insurance has cash value. The annuity will then invest and generate income based on your cash value balance. You give up the life insurance death benefit for more income and investment guarantees. However, you cannot convert an annuity into life insurance.

What Are the Downsides of Annuities?

Annuities can have a costly surrender charge if you cancel early. The fee can potentially be 7% or more of your account balance. Annuities lock up your money for years. They can also come with considerable annual fees for their investment and income guarantees. Finally, annuities based on stock market investments can be complicated and difficult to understand.

Do Annuities Stop at Death?

Whether annuities stop at death depends on what income option you select. Payments stop at your death if the income is based only on your lifetime. You can also request a minimum number of payments, like 20 years. If you die before 20 years, the remaining payments will go to your heirs. Adding extra income guarantees will reduce the monthly payment.

Bottom Line

Cash value life insurance and annuities can both help you accomplish a number of goals. However, these strategies can be complex and take considerable amounts of money. Consider discussing these strategies with a financial advisor before buying into either financial product.