Kevin Carmichael

Sept. 8, 2021

The Bank of Canada said the economic recovery remains on track, an expression of faith in the recovery that suggests policy-makers could still further reduce their purchases of federal bonds this year despite evidence the economy struggled throughout the spring.

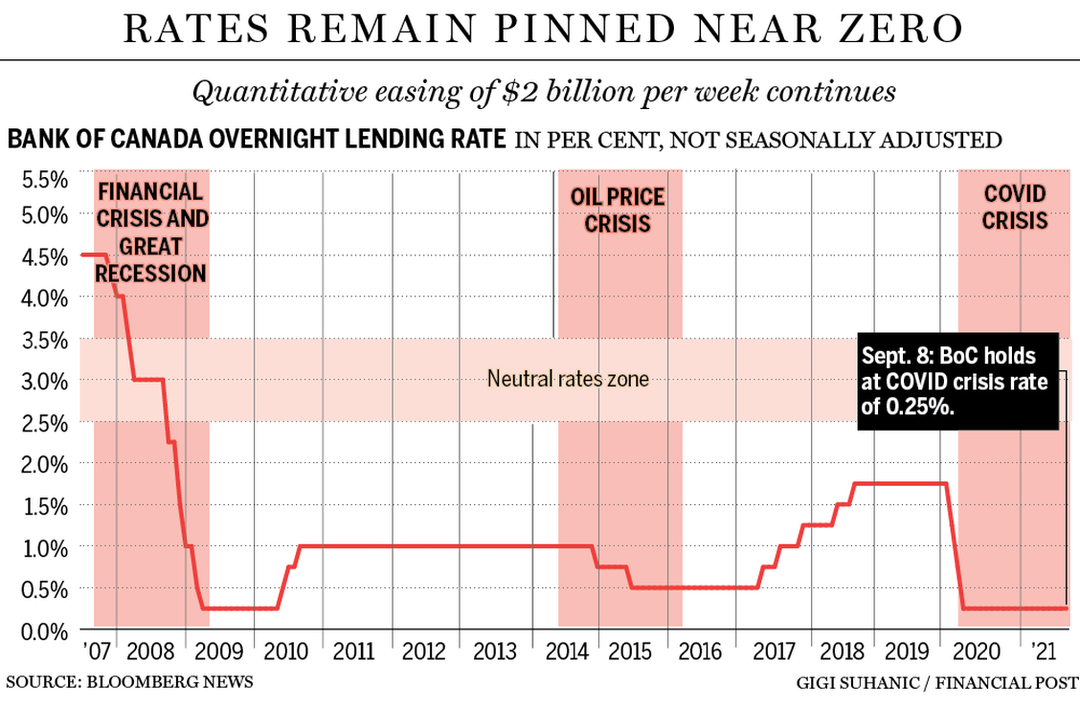

As expected, Governor Tiff Macklem and his deputies opted to leave the current level of stimulus unchanged at the end of their latest round of interest-rate deliberations on Sept. 8. The election raised the bar for a shift in policy, as Macklem would only risk becoming a campaign issue if economic conditions demanded it. They didn’t, allowing the governor to make the central bank’s latest interest-rate decision into a non-event.

The Bank of Canada kept the benchmark borrowing rate at 0.25 per cent, reiterating that it intends to leave it there until at least the second half of next year. Policy-makers also re-upped their pledge to buy roughly $2 billion worth of Government of Canada bonds every week, a commitment that was lowered from $3 billion at the end of the previous round of policy deliberations in July.

“The bank continues to expect the economy to strengthen in the second half of 2021, although the fourth wave of COVID-19 infections and ongoing supply bottlenecks could weigh on the recovery,” the Bank of Canada said in its update policy statement.

The central bank’s confidence in the recovery might surprise some people. Gross domestic product (GDP) contracted at an annual rate of 1.1 per cent in the second quarter, while policy-makers had been anticipating growth at annual rate of about two per cent. It was a notable miss.

But the Bank of Canada’s leaders mostly shrugged it off, saying the recovery continues to unfold roughly as they assumed it would when they last updated their outlook in July. The Bank of Canada predicted then that GDP would grow six per cent in 2021 and 4.6 per cent in 2022 after contracting by more than five per cent last year.

Forecasting during the pandemic has been difficult because models based on history are ill-equipped to deal a truly unique global calamity. Sometimes the surprises have been positive. The Bank of Canada had assumed in January that the third-wave of COVID-19 infections would cause the economy to contract in the first quarter, and instead it grew at an annual rate of 5.5 per cent. So to a certain extent, the recovery is ahead of where the central bank thought it would be at the end of last year.

“Employment rebounded through June and July, with hard-to-distance sectors hiring as public health restrictions eased,” the Bank of Canada said. “This is reducing unevenness in the labour market, although considerable slack remains and some groups – particularly low-wage workers – are still disproportionately affected.”

Macklem has said repeatedly this year that he is looking for a “complete” recovery that returns employment levels to what they would have reached if not for the crisis. Still, he has to keep an eye on inflation, which surged 3.7 per cent in July from a year earlier, matching the largest increase since 2011. The Bank of Canada’s target is two per cent.

Inflation, as measured by the consumer price index, “remains above 3 per cent as expected, boosted by base-year effects, gasoline prices, and pandemic-related supply bottlenecks,” the statement said. “These factors pushing up inflation are expected to be transitory, but their persistence and magnitude are uncertain and will be monitored closely. Wage increases have been moderate to date, and medium-term inflation expectations remain well-anchored.”