Julia Carpenter

May 31, 2019

A combination of factors—the shadow of the 2007-09 recession, mounting student debt and a changing job market—are hindering millennials’ financial progress.

These forces and their consequences became especially apparent in the responses to Janet Adamy and Paul Overberg’s piece on millennials approaching middle age in crisis.

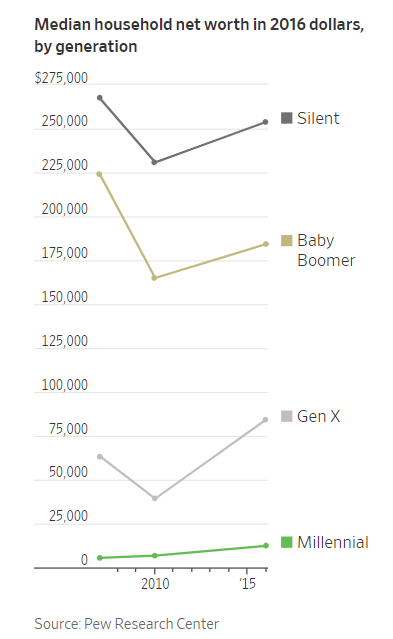

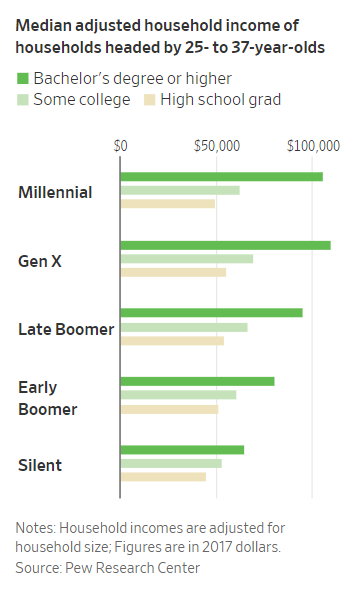

Compared with previous generations, millennials are earning less and swimming in more student debt. Traditional assets, like property or a home, are becoming more expensive relative to wages and unattainable for many. Many millennials who can’t buy property or invest in the stock market early enough will miss out on potential profits, as prices climb.

In response to readers’ requests for advice, we’ve put together a three-part guide:

DEBT

“If my young self knew what I was doing when I signed my life away on the dotted line just to go to school then I probably would never have gone.”—Danielle Cooper

OK, so you have debt

Who doesn’t?

Americans carry $1.5 trillion in student loan debt, and the average millennial student-loan balance in 2017 was $10,600, according to the Federal Reserve.

Credit card debt continues to be a problem for young people. According to a 2019 report from the New York Federal Reserve, student-loan and credit-card delinquencies have been rising since 2017.

Assess the big picture

Total together your student loan debt, credit card debt and any outstanding loans, like a personal one from your parents and friends, and your pending car payment. If you have other debt, add that to the total as well.

Once you have the full amount staring you in the face, you can make a plan.

Minimum payments matter

If you work at a traditional job, start by setting a calendar reminder for a bimonthly payday. Then set another calendar reminder for making payments from your account.

Next, consider the minimum payments. Paying only your minimum payments will keep you in debt longer. Understanding your interest rates can help you craft a strategy to bust that cycle.

If you are unemployed or work freelance, set your own calendar reminder to pay your bills by the deadlines.

Think about interest

Because interest is already at work on your debt, some kinds of debt are more “urgent” to handle than other kinds.

This is why a lot of personal finance advice-givers suggest prioritizing paying down your debt with the highest interest rate. If you have debt on multiple credit cards, for example, deploying what’s known as the “snowball” strategy means you tackle the one with the highest interest rate first. It may not be your biggest debt, but it’s the most pressing because with the interest, that smaller amount of money owed will only grow more quickly.

If you are googling “consolidation,” “refinancing” and other debt repayment plans

When you consolidate debt, you combine it into one monthly payment. This can make paying down debt easier, but it can also affect your credit score—so do your research.

INCOME

“I’m a millennial, with an associate degree. Will I struggle forever?”—Bashir Hopewell

How to get paid more

One report from the St. Louis Federal Reserve found that young millennial families are at risk of becoming a “lost generation.” Median wealth levels of a family headed by someone born in 1980 was 34% lower than what researchers had expected of past generations.

Are you being paid well? Should you switch jobs? These are big questions, as the economy reaches full employment. Researching your salary, knowing your market value and talking with your peers could help you take steps to be paid more competitively.

…and where does your income go?

Tracking your spending for a single month can be incredibly helpful in discovering expenses you can get rid of.

ASSETS

“My wife and I struggle living paycheck to paycheck and I still dream of a day when I am debt-free, have a home and a saving account.”—Jessica Padilla

First, set aside $400 for emergencies

Almost 40% of Americans don’t, but consider setting aside a small amount from every paycheck. Put it in a high-interest savings account where it can grow slowly over time and be easy to access when you have an emergency.

Start thinking about retirement

Yes, it feels far away. Yes, it’s hard to plan your life that far in advance.

But if you’re lucky enough to work for an employer that offers a 401(k) match, take advantage of it. If you don’t have a 401(k), consider a Roth IRA, which will allow you to take money out for emergency expenses, and a health savings account, which will help you escape tax penalties, should you need to withdraw for a medical expense.

If you can’t buy a house

A lot of your peers need help buying property, too. You will have other assets. It is going to be OK.

Still feeling behind?

Consider all these things at once—your debt, income and potential assets. They all work together.

When you’re so far behind and so intimidated by the big picture, it’s hard to even getting started righting the ship, let alone catch up to the benchmarks set by your parents and grandparents. But Justin Pritchard, a certified financial planner in Montrose, Colo., says there are reasons for millennials to stay hopeful.

“The question is: Do they really want to be exactly like the previous generations?” said Mr. Pritchard.

Write to Julia Carpenter at Julia.Carpenter@wsj.com

Copyright 2019 Dow Jones & Company, Inc. All Rights Reserved.