David F. Smith

Sept. 21, 2017

In this time of moderate interest rates, some people are considering investing in rental property. If the biggest chunk of the monthly cost of ownership – the mortgage payment – can be frozen for 30 years while rents gradually increase, the resale value of the property escalates and all the while you enjoy the income and tax benefits, then you could have a win-win on your hands. There are some big “ifs” in that statement, but they mostly have to do with the investment property itself (will it be the gem you thought it was? will you avoid the tenant from hell?) rather than the financial and tax issues.The interest rate for a 30-year fixed mortgage is currently around 4.01% according to bankrate.com as of February 2017, and the tax code is really tilted for home ownership and investment.

Do Think About the Tax Advantages

- Interest, taxes, insurance and other expenses are deductible against the property’s income, while losses can usually be deducted against your other income. (To learn more, read Tax Deductions For Rental Property Owners.)

- Depreciation is another tax deduction. It’s basically an allowance for wear and tear, usually over 27.5 years, or 3.636% of the purchase price of the buildings (not the land) per year.

- Rental properties can be sold, and the proceeds rolled into other rental property without paying capital gains taxes.

Do Consider Different Types of Property

If you do decide you want to invest in a rental property, you can do it a lot of different ways:

- a rental unit in your existing home or on your existing property

- an apartment in an existing multifamily condominium or cooperative

- a house or apartment in a community that you might want to retire to

- a house or apartment in the area where your children are attending college as an alternative to student housing

- a vacation home by a lake, beach or ski slope, where you can use it for two weeks of the year without compromising the tax advantages (For more, see Tax Breaks For Second-Home Owners.)

Don’t Forget You’ll be a Landlord

Each of these has its own bundle of advantages and pitfalls, and some people just don’t like the idea of being a landlord. Managing a property, and tenants, requires some time and energy, and it helps if you can do minor repairs yourself. If you were to buy a two-family house in an improving neighborhood, for example, live in one unit and rent the other, you could find your own cost of shelter (home expenses combined with rental income and depreciation on the rental unit) approaching free or exceeding it within a few years.

Do Your Real-estate Homework

Researching rental property should be at least as rigorous as if you were buying a place to live in. You must know the market specifics, zoning laws and trends for both rentals and home sales of the type and in the location you are contemplating, including schools, transportation, recreational resources, shopping, etc., as well as what is popular in the demographic you will want as tenants. Don’t forget to consider foreclosures, since all the foreclosing bank usually wants is the balance owing on the mortgage.

Look for something timeless like waterfront, or proximity to a college campus, or an older house in a stable community or one that is in the beginning phases of a comeback. Beware the “golf course syndrome,” in which the investment rental property on a new golf course becomes dated in a few years while newer, fancier golf course/housing developments are being built in the same general area, depressing the prices of the older houses.

In doing your calculations, remember that a tenant paying top dollar has a right to expect a near-instant response to any problem, large or small. Renters who know they are paying a little under market will tend to be a little less demanding. If the prospect of managing your own rentals is daunting, your real estate broker can likely make a referral to a property manager or caretaker; an online search will also find specialty property managers. Just be aware that hiring a property manager will eat into your returns.

Don’t Neglect to Run the Numbers

Smartphone apps and online mortgage calculators like Investopedia's calculator can help you with this. Using calculators is helpful because they allow you to gauge the true cost of your monthly housing costs. For example, they all allow you to enter cost, down payment, taxes, insurance, and, of course, the interest rate, to arrive at your expected monthly payment.

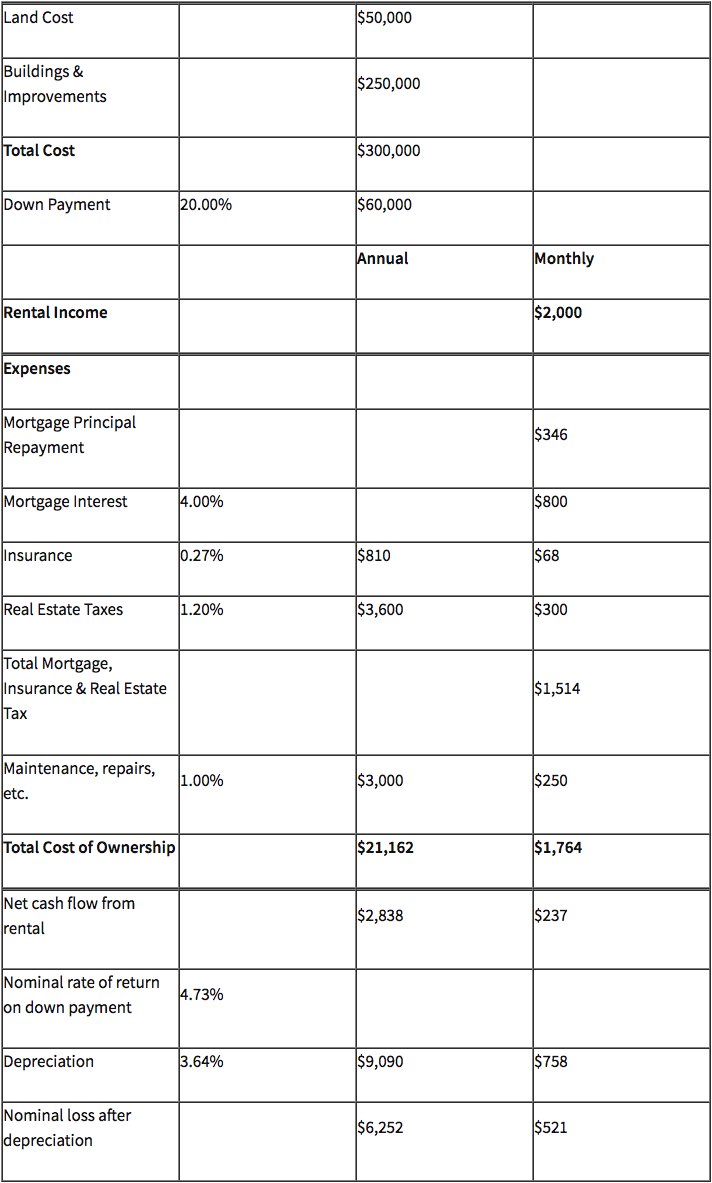

Then, once you've gathered your numbers using a tool like the mortgage calculator above, you can plug those into a worksheet like the one below to figure out whether a particular property makes sense for you.

For your calculations, figure that a rental property will not get as low a mortgage rate as a primary home will. In this example, a four-bedroom house costing $300,000 is rented for $2,000 per month. The 20% down payment is $60,000, and the 30-year fixed interest rate on the $240,000 balance is 4%. Taxes, insurance, and a maintenance budget bring the monthly cost to $1,764, yielding a nominal profit of $2,838 per year, or 4.73% of the down payment per year. That’s much better than a savings account and better than most blue-chip stocks pay in dividends, although maybe not as much as you could earn in the stock market in a good year. But when you figure in depreciation, the nominal gain of $2,838 becomes a loss of $6,252, which can be applied against other income.

Depending on your tax bracket, that could amount to several hundred dollars of tax savings to add to the positive cash flow, not to mention the possibility, though not a certainty, of increasing value over time.

The Bottom Line

Investing in real estate for income is not for everyone, but if you have a long investment horizon, a tolerance for the inherent risks and are handy with a hammer, the benefits can be truly substantial.