Sean Hanlon, Contributor

July 17, 2020

Entering 2020, the US economy and markets were on stable footing for the most part. The Federal Reserve had reversed its so-called policy mistake of raising rates too quickly at the end of 2018 and plugged a hole in liquidity issues in short-term funding markets amongst financial institutions at the end of last year. The US economy was growing at a solid and consistent 2% pace, with optimism running high on continuing the longest US economic expansion in history into a new decade. Though, however ironic, a quote by socialist Vladimir Lenin summarizes what happened next; “There are decades when nothing happens, and there are weeks when decades happen”, where the latter certainly applies to the Spring of 2020.

US equity markets were still making new highs into mid-February on the back of a Phase 1 US/China trade agreement despite reports of a novel flu-like disease wreaking havoc around a market in Wuhan, China. By St. Patrick’s Day, a nationwide lockdown due to the COVID19 virus had flipped life as we know it on its head. Fear pummeled capital markets, with liquidity paramount, as mounting unemployment and uncertain cash flows threatened corporate, municipal, and personal budgets. A predictable explosion of civil unrest spread across the country, sparked by racial injustice and exacerbated by frustration with the shutdown and election year partisanship.

Congress, however, came together in a bipartisan way to unleash trillions of dollars in emergency stimulus by tentatively plugging holes in consumer incomes and balance sheets of majorly affected industries. In addition, an acronymic avalanche of programs from the Federal Reserve (Fed) has released trillions more and so far, solved severe liquidity concerns in financial markets. The ferocity and breadth of the stimulus have encouraged increased risk taking into historically high valued equities, pulling forward future returns and perpetuating behavior that over time increases the fragility, due to excess leverage that caused the need for so much monetary support in the first place. Congress is now working on a fresh round of stimulus for the millions of citizens and municipalities that continue to be affected by COVID19, but the social and economic effects are such that there will be a “new normal” where the pre-COVD19 paradigm exists solely in the past.

Economic Backdrop

The shutdown has produced one historically bad statistic record after another as we wait for the most important verdict of the economic growth number from the hardest-hit 2nd quarter. Real, or inflation-adjusted, Gross Domestic Product (GDP) fell by an annualized -5.0% in the 1st quarter versus 4Q19, according to the final estimate from the US Bureau of Economic Analysis. The Atlanta Fed GDPNow estimate is currently expecting a -40% drop for the 2nd quarter, which is a welcome improvement from the over -50% estimate as recently as early June.

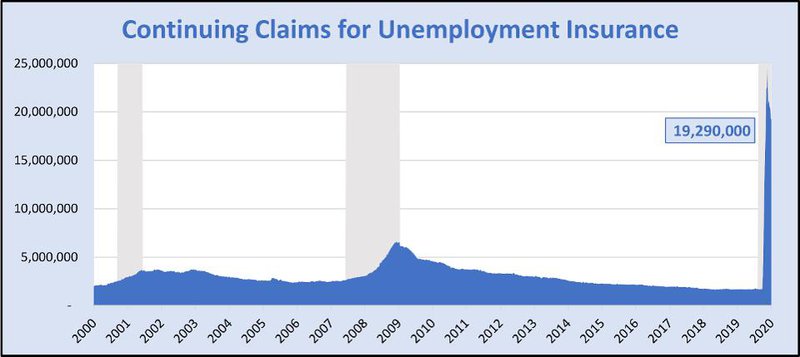

Chart created by Hanlon with data provided by Federal Reserve Bank of St Louis (FRED) and the National Bureau of Economic Research (NBER) for gray-shaded recessions.

Week after week, over a million people are still applying for first-time unemployment insurance, albeit at a decreasing rate from the record of near 7 million people at the beginning of the shutdown in March. Continuing claims remain high but have been falling as those in the decimated foodservice and tourism industries have started to return to work, which led to the largest consensus estimate miss of a Non-Farm Payrolls release - with an increase of 2.5 million people surprising the -7.5 million estimate by a whopping 10 million people and the official unemployment level at 13.3% versus an expected 20%. While this is an incredible rise from the 3.5% half-century low in unemployment from the beginning of the year, the unanticipated results prompted a White House press conference with a celebratory tone about the state of the economic rebound.

While the headline unemployment numbers were shockingly high, the additional weekly $600 unemployment insurance bonus resulted in more than two-thirds of laid-off workers effectively receiving a pay raise, including one-fifth of recipients receiving benefits equal to double their prior pay. Combined with the one-time stimulus checks, personal incomes rose by 10% in April despite widespread layoffs. This has presented lawmakers with a conundrum, as they now must convince unemployed workers to return to the workforce (and potentially take a “pay cut”), while still offering a lifeline to those with no current job prospects. The extra $600 will expire at the end of July, and with Congress on recess, its prospects for extension look murky. Alternative proposals are being floated, such as a $450-per-week bonus for going back to work.

Hope for a so-called V-shape recovery has waned since that early-June payroll report as the sustained levels of new claims foreshadows a disturbing trend for a broader set of industries in the post-COVID19 economic environment. Many survey-based indicators have started to improve, even if contracting at a decreasing rate, with the manufacturing Purchasing Managers’ Index (PMI) rebounding from the April low of 41.5% to 43.1% with a level of 50% being the threshold between contraction and expansion. Non-manufacturing or service sector PMI has rebounded to 45.4% from 41.8% in April, also still contracting but at a slower rate. Service sector business activity and new orders had large rebounds in May, while employment in this report is still firmly in negative territory, indicating cause for concern in the broad service sector which represents roughly 70% of American non-farm payrolls.

Measures for inflation have dropped since the shutdown began, as plummeting demand led to the April seasonally adjusted annualized reading of -0.8% for the Consumer Price Index (CPI). The Core measure (excluding volatile readings for food and energy), at -0.4%, had its largest month-on-month decline since the 1957 inception of the series and its first back-to-back monthly declines since 1982. The headline CPI number for May declined again, falling -0.1%, though COVID-related effects have led to food prices and food prices at home to have risen by 4.0% and 4.8% year-on-year from May of 2019, respectively, which combined with rebounding energy price may continue to put pressure on many households’ discretionary budgets.

As the massive estimate miss on June payroll data illustrates, we are in a highly uncertain environment as the COVID19 pandemic has introduced new variables, via government restrictions and stimulus measures. These opposing forces have made estimates and forecasts for economic data wildly unpredictable, which inevitably leads to both upside and downside economic surprises that become the catalyst for major swings in financial markets.

US Equity

With the Fed effectively negating the potential for a liquidity crisis, the opening of fiscal spigots led to a jump in savings and reportedly a flood of retail investors piling into markets that had drawn down -30% or more. Growth and momentum names were in particularly high demand, with an improved tailwind of an expected acceleration in the remote work paradigm due to the COVID19 outbreak. Multiples for many companies in the software and digital infrastructure industries easily regained or even surpassed prior heights thanks to lofty expectations for increasing addressable markets. The flood of liquidity had nowhere to go besides financial assets with the economy essentially shutdown, with many businesses delaying capital investment and consumers unable to spend in the real economy even if they wanted to. Even the consumer discretionary sector was able to reach a new high after the panic, although that was due to large weightings to a certain online retail giant and home improvement stores that were largely able to remain open during the shutdown.

Chart created by Hanlon with data provided by Investors FastTrack, using Vanguard Value ETF (VTV) to represent value and Vanguard Growth ETF (VUG) to represent growth.

The beaten-down financial sector rallied from mid-May until early June as part of a “value” push, with growth/momentum names having run as far as they could and finding upside on relative valuation and yield differential. The sector was unable to maintain the thrust, with increased credit loss provisions cutting into profitability as clouds continue to form in the consumer and commercial credit landscape despite all the liquidity. Banks have been instructed by the Fed after the most recent stress tests to pause dividend increases and suspend share buybacks (which have become politically tricky across industries) through the 3rd quarter, in order to preserve capital. Other sectors most exposed to another COVID-related economic deceleration, including energy and industrials, are also off their post-panic highs on news of rising cases and hospitalizations. The S&P 500 is trading at just under 20x the 2021 Operating Earnings estimate of $161.28, which has been revised lower by over -15% from the January pre-pandemic estimate. This forecast represents an optimistic 50% increase on the 2020 shutdown-impaired estimate. If the 2021 estimate holds true, it would equate to a 2.7% growth rate from 2019’s Operating Earnings of $157.12.

Developed International Equity

European and Japanese markets have performed better on a relative basis since May of 2020 as the expansion of stimulus measures and relatively successful suppression of COVID19 infections are forecasting an economic rebound, allowing markets to make up ground on US outperformance. Japan has so far managed to limit virus spread and deaths without the complete shutdown experienced by western nations, which is quite a feat considering the high population density and average age which have ironically weighed on economic growth for decades. The Bank of Japan has continued to add to its portfolio of Japanese assets, which includes a large chunk of the country’s equity ETFs while unleashing a mammoth $1 trillion of fiscal spending to support the world’s 3rd largest economy. This brings Japan’s total spending during COVID19 close to the US’s response, but a whopping 40% of annual GDP.

Incredibly, Brexit is still creating an overhang on businesses in the UK and Euro-area as the two sides struggle with coming to acceptable terms on a trade deal beyond the transition period, with fishing rights and the Irish border agreements providing particular sticking points in maintaining fairness within industries but across borders. The two sides are due to restart face-to-face meetings that have remained at a standstill over “unrealistic positions” during continued virtual meetings, while a fall deadline threatens to resolve in a standard World Trade Organization (“WTO”) agreement that both sides also find unacceptable. The US has levied tariffs on several European goods, with threats of more, due to WTO-confirmed anti-competitive behavior on the behalf of the European Union (“EU”) in the aircraft market. The EU has threatened reciprocal tariffs in response, exacerbating the global slip in multilateral cooperation while both the EU-based Airbus and US-based Boeing BA struggle with COVID19 related struggles.

Emerging Market Equity

Relations between the US and China have notably deteriorated under the surface since the signing of the Phase 1 deal, despite official reports of continued cooperation. Markets are likely discounting the Trump administration’s willingness to allow a total breakdown in negotiations prior to the election despite China’s inability to fulfill its commitment of agricultural purchases due to circumstances surrounding COVID19. US political rhetoric regarding the handling of COVID19, Hong Kong, the South China Sea, and now a territorial dispute with neighboring India has been just that, rhetoric, but threatens to derail the already tenuous relationship. Both sides are seemingly planning for a future with at-best, less cooperation, and at-worst, conflict, as multi-national corporations continue to adjust supply chains accordingly.

In the meantime, emerging markets have lagged US markets year-to-date but have outperformed in May and June thanks to having coronavirus cases peaking and re-opening earlier than in the US. Global stimulus efforts have also had a spillover effect, easing US dollar liquidity concerns and making up for falling US demand for imports. The opening of US dollar swap lines by the Federal Reserve has also helped resolve concerns in emerging markets, while efforts are also being made so liquidity concerns don’t turn into solvency problems for international issuers of US dollar-denominated debt. The recent pullback of the greenback versus many EM currencies highlights the efficacy of the programs, though more will certainly be needed if trade doesn’t pick-up.

Fixed Income

The top-performing asset class so far this year has been long-dated US Treasury securities. The US 30-Year Treasury Note yield dropped from 2.3% at the beginning of the year, to a low near 1.0% in early March, while finishing June just above 1.4%. The flight to safety trade combined with Fed interest rate cuts and open market purchases helped offset $2.3 trillion in new issuance during the 3 months ending May 31st by the US Treasury Department, who also added a new 20-Year Treasury tenor to help finance the COVID19 response stimulus. The Fed will likely have to continue these Treasury purchases, which also include mortgage-backed securities, municipal bonds, corporate bonds, and bank loans to small and medium-sized businesses, or risk higher borrowing costs for all.

Chart created by Hanlon with data provided by Investors FastTrack. Long term (20+Year) Treasury Bonds represented by iShares Long Term Treasury ETF (TLT), Investment Grade Corporate Bonds by iShares US IG Corporate Bond ETF (LQD), and High Yield

The announcement that the Fed would buy corporate bonds and corporate bond ETFs, including high yield bonds, came as a surprise to markets and led to a large single-day jump for corporate bond ETFs on April 9th. Though technically illegal, the Fed is using a loophole that allows the US Treasury to first buy the bonds or broad ETFs, and then buy them from the Treasury. This has allowed many corporations to find favorable terms for issuing debt despite the extra risks posed by the pandemic, significantly reducing credit spreads for all except the most vulnerable, lowest rated debt on the market.

While the Fed’s “Deus ex Machina” intervention may have allowed many zombie companies to kick the can down the road, a prolonged economic downturn will inevitably bring an uptick in defaults. Credit quality has been deteriorating, with high yield ratings downgrades outpacing upgrades at a 7-to-1 rate, and the trailing-twelve-month rate of defaults reaching 5% for the first time since 2016. Despite these risks, we see pockets of opportunity within high yield, particularly in bonds of “fallen angels”, investment-grade companies that are downgraded to high yield.

Commodities and Alternatives

It was an incredibly wild and historic 1st half for oil prices. After starting the year over $60 per barrel, the front month WTI Crude Oil front-month oil futures contract hit nearly -$40 per barrel of oil on the last day of contract trading in April. Full domestic storage and complete disappearance of demand due to COVID19 led to speculators having to pay people to offload contracts for the right to buy oil. Needless to say, the US energy sector has been rocked by volatility and uncertainty, with many companies responsible for the US energy boom in recent years unlikely to make it through without substantial US assistance. While eligible companies may tap borrowing facilities or public markets, many will have to fend for themselves because overt assistance will likely be accompanied by another supply flood from OPEC members.

Real Estate Investment Trusts (REITs) have underperformed so far in 2020 due to cash flow uncertainty post-COVID19. Retail and mall REITs have been under pressure for quite some time, with the pandemic accelerating viability concerns for traditional retail. REITs in the commercial space are also in question thanks to work from home, while skilled nursing facilities struggle with rising costs and liabilities related to the pandemic. REITs may remain under pressure as the fallout from the pandemic is worked through, however, they are one of the last areas of the market to find yield if the underlying asset values can maintain through the uncertainty.

Final Thoughts

Markets are data-driven in the long-term yet can experience amazing volatility in the short-term, as we just witnessed. We will have more clarity in the coming months, but there are still numerous uncertainties surrounding how the global economy moves towards a full economic recovery. Markets are constantly searching for equilibrium. Many argue that the first quarter sell-off was an overreaction, and others say that markets have become overly reliant on government stimulus and central bank rescues. This dependence only exacerbates the potential volatility if future stimulus measures prove insufficient or ineffective. How much stimulus is enough, and can the long-term health of the US balance sheet handle it?

The COVID19 pandemic has permanently impacted global views on economics, medicine, technology, societal structure, and more. The pandemic will eventually end, but the implications will carry forward in decades to come. The weight of the lives lost to this terrible disease will be felt for generations. As always, however, we choose to remain optimistic for the future and focus on the ways that society can learn and evolve from this catastrophe. As capital is diverted towards medical research at a frenetic pace to find a vaccine for COVID19, a likely side effect will be the invention of drugs and treatment methods that can be applied to other diseases as well, along with advancements in sanitization and disease tracing that could combat future pandemics. Technology, likewise, is being pushed forward by the shift from physical to virtual office space, spurring breakthroughs in cloud computing and networking.

These are trying times, but we will persevere by taking steps to stay healthy and positive. Keep in mind, this is not a destination, it’s a transition.

© 2024 Forbes Media LLC. All Rights Reserved

This Forbes article was legally licensed through AdvisorStream.