Rick Miller, Contributor

Dec. 19, 2020

When can I stop working for a living? If you are over 40, and almost certainly if you are over 50, you’ve asked yourself that question at least once. That’s not quite the right question, and it’s probably not the whole question you are asking.

For most people, the question is: “when can I retire and still live the way I want to live?” or maybe “when can I retire and live the way I’ve become accustomed to living?”

To take on the whole question requires thinking a lot about risk – longevity risk, investment risk, health risk, family risk.

- You (and your partner) may live longer than you think you will – many people underestimate.

- Financial markets, especially the stock market, are subject to booms and busts. A big stock market bust during your retirement could disrupt even your most careful planning.

- A major health event could be very expensive. Long term care can be very costly if it lasts for several years.

- Family issues can also introduce unexpected costs. Children can lose their jobs, divorce, or become ill. They may need extra schooling or medical care. Many retired parents feel compelled to help, using precious resources they saved for their “golden years.”

The future is an uncertain place, and retirement is long. Your retirement is likely to last thirty years or more, during which your financial flexibility will decrease – you won’t be able to work more hours, look for a higher paying job, or plan to work more years before retiring, you’ll already be retired!

Think back thirty years from 2020. That’s 1990. In 1990, who predicted 9/11, the rise of the Internet, or Google, Amazon AMZN , Facebook, and Netflix NFLX ? What about President Barack Obama or President Donald Trump? I have a strong suspicion that you’ve experienced important events in your own life that you didn’t predict in 1990.

We won’t cover the risks and unpredictability in this article. Instead, we’ll focus on basic concepts, clarifying the fundamental issues that arise when you consider how you’ll live the way you do now without any earned income.

Perhaps surprisingly, you already have a retirement plan. There is a year when you could retire and keep on living the way you live now without any earnings. If you save a lot each year and don’t spend very much, it could be this year. If you don’t save much and spend a lot, you might not be able to retire until your 90s!

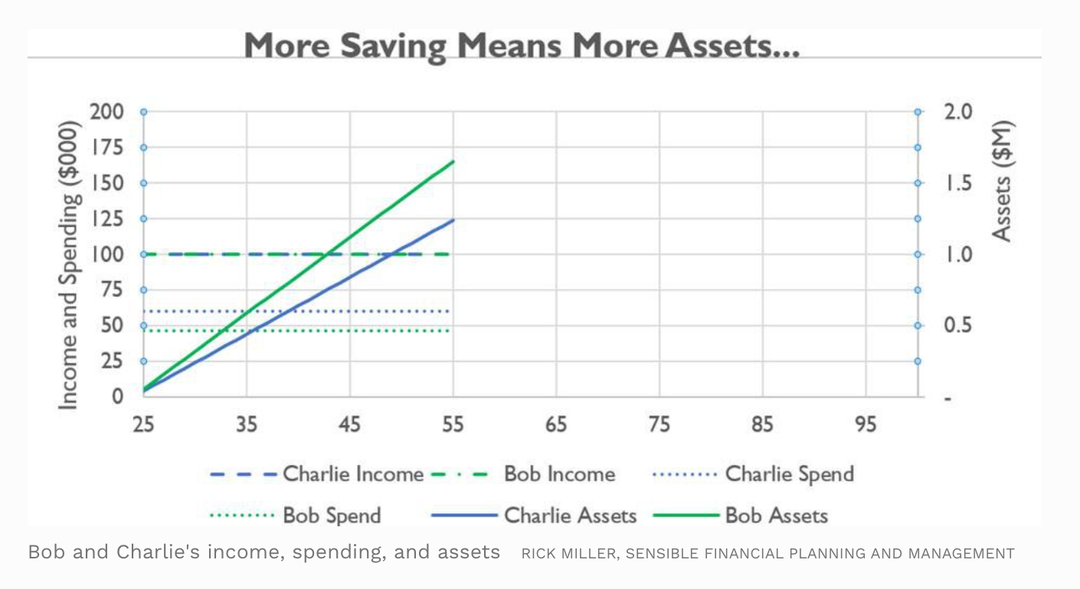

We’re going to start with a simple world, and two people who live there. The world has no taxes, no Social Security, no stock market, and 0% interest rates. Bob and Charlie are both 55 now, and they have been working since they were 25. Each earns $100,000 per year. Their spending and saving are different, though. Charlie spends $60,000 per year and has saved $1.24M. Bob spends $46,667 and has $1.65M in savings.

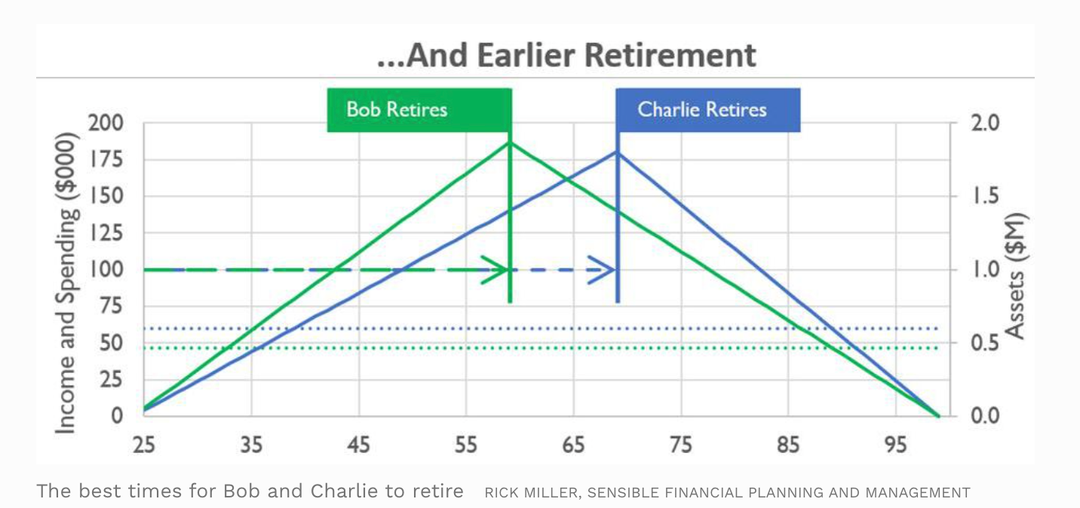

When can they retire? Bob has more assets and spends less than Charlie. He can (and will) retire earlier – at 60 versus 70 for Charlie. He’ll have more assets when he retires - $1.87M – than Charlie will ($1.74M). So, save more, spend less – retire earlier – and spend less in retirement, too. Save less, spend more – retire later – and spend more in retirement. Both Bob and Charlie will spend all of their assets in retirement, just using them up as they reach age 100.

In the real world, people do pay taxes and they do have access to Social Security benefits. How do we think about retirement readiness while accounting for this additional complexity? Conceptually, two basic notions are still the same:

- Maintain your living standard throughout your life, both before and after retirement

- Use all your savings to support your retirement living standard

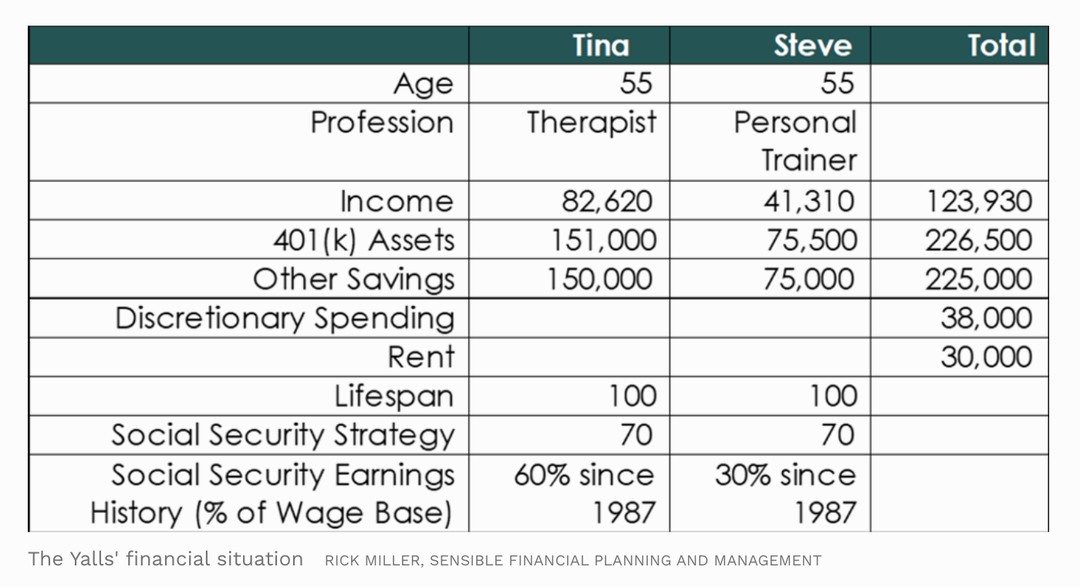

The Yalls are a 55-year-old couple with a straightforward financial situation, trying to figure out when they can retire. We know (see the table) what they earn, how much they have in assets, their planning horizon, and when they plan to take their Social Security benefits.

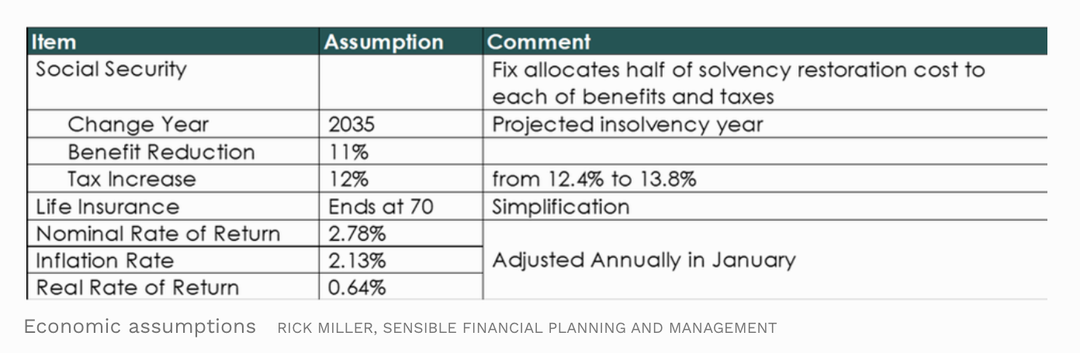

We also know (chart below) about the world they live in, and especially, what’s coming: future investment returns, inflation, and potential changes in Social Security retirement benefits.

Armed with all of this information, we can project how much they could spend on discretionary spending (their living standard) every year from now through the end of retirement, depending on when they retire. Their retirement year determines the amount of savings they’ll have accumulated. Each additional year of work allows one more year of saving, and one more year of investment returns on their savings. Each year of work also supports an increase in their Social Security retirement benefits.

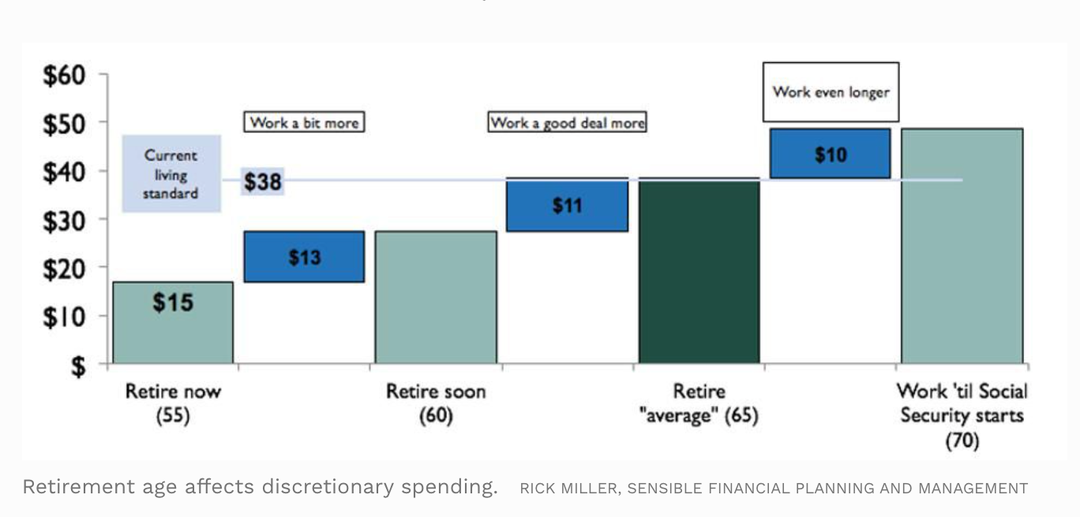

Recall that the Yalls spend $38,000 per year on discretionary items. The ages 55 and 60 are too early to retire. If they retire now, at 55, they’ll be able to afford only $15,000. Waiting until 60 to retire will enable them to spend $27,000 per year – still short of their current living standard. At 70, they could spend $49,000 – even more than they spend now. They don’t need to wait that long. Retiring at 65 is the “Goldilocks” year – just right. Their withdrawals from taxable accounts and from their IRAs starting when they retire, coupled with their Social Security benefits, will allow them to spend $38,000 per year on discretionary items, after they’ve funded their rent and paid their income taxes and Medicare Part B premiums.

Just as with Bob and Charlie, the Yalls’ spending and saving strategies imply a retirement strategy – a date when they can afford to retire and keep spending what they are used to spending.

You have an implicit retirement strategy, too. The big question is whether your implicit strategy aligns with your articulated strategy – the date that you (and your partner) have decided will be your last day of work.

The foregoing content reflects Rick Miller’s opinions and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions, or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns.

Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

By Rick Miller, Contributor

© 2024 Forbes Media LLC. All Rights Reserved

This Forbes article was legally licensed through AdvisorStream.