SAM SIVARAJAN

Aug. 12, 2019

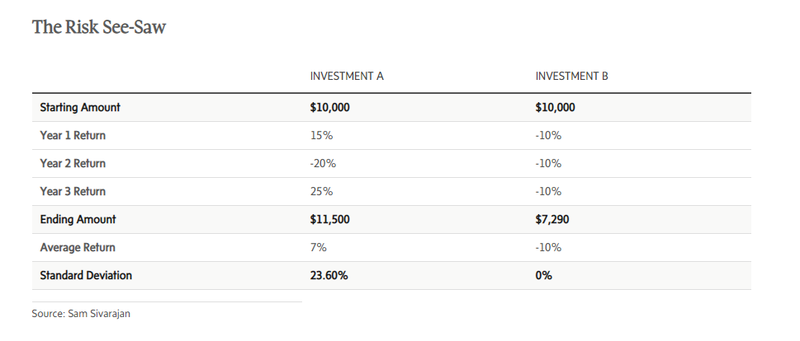

Canadians are faced with choices about risk every day. Risk is the four-letter word of investing, but it is poorly understood. Consider, for example, the two different investments in the accompanying table: Investment A and Investment B.

Which investment do you prefer? A or B?

I would be surprised if anyone did not prefer A. After all, you end up with more money after 3 years.

Now, let me ask you – which investment is riskier?

According to investment orthodoxy, Investment A is riskier! Why? Because, it has a higher standard deviation (or volatility of returns) at 23.6% than Investment B at 0%.

Doesn’t that strike you as odd? Losing money 3 straight years in a row and losing almost 30% of your original investment is considered to be less risky than making $1,500 over three years (although with a bit more of a roller-coaster ride). No one I know would consider Investment A “riskier” than B.

Fundamentally, the issue arises because risk – in the investment sense – is multi-dimensional. There are at least four different types of risk that need to be considered when investing:

- Volatility – this is the standard measure of investment risk and it focuses simply on the variability of returns. One investment that has “zero” volatility is a savings account at a Canadian bank. However, that zero volatility comes at a price – a very low return on investment.

- Shortfall – this is the measure that, in my experience, most investors are concerned about – running out of money or not having a target amount at the target date (i.e. $100,000 down-payment for house purchase in 5 years, etc.). But volatility and shortfall risks sit on a see-saw – if you want lower volatility risk (e.g. the savings account), you have to accept higher shortfall risk (e.g. outliving your money in retirement).

- Liquidity – this is the risk of not being able to convert your investments into a cash quickly and without a haircut. I remember a potential client I met in 2009 – the individual was worth several hundred million dollars. Yet, he told me that he had declared bankruptcy a few weeks earlier. How is this possible? Well, he was worth several hundred million dollars in assets but none of them were liquid in the credit crisis. He did not have the cash flow to pay the loan servicing costs.

- Capital loss – this is the risk of actually losing money in an investment – in other words, buying it for $100 today and selling it for $90 in a year’s time. But, in many ways, this is the easiest risk to manage. Buy a single stock or investment and the risk of capital loss is quite big – invest in a fund or a portfolio of stocks and the risk goes down significantly. Hold the fund or portfolio for 5, 10 or more years, and the risk of capital loss, historically, has been virtually negligible.

Investing successfully means that you need to understand that risk is multi-dimensional. And it always involves a trade-off between the different types of risk. Not taking volatility risk means that you are automatically taking shortfall risk (or liquidity risk).

Most wealthy Canadians that I have worked with understand this key point – that different risks need to be traded off. They also know that risk is the currency with which they buy return. If you don't want much downside risk (i.e. potential for loss), then you have to accept that you won’t have much upside potential.

There is no right or wrong decision here – just understand that not taking risk is taking risk. That is true for investing. That is also true for most decisions in life – inaction can be as risky (or more) than action.

This Globe and Mail article was legally licensed by AdvisorStream.

© Copyright 2025 The Globe and Mail Inc. All rights reserved.