By Julie Cazzin, with Allan Norman

Sept. 27, 2021

Have you ever viewed a reverse mortgage commercial and wondered whether it would help you maintain and enhance your retirement lifestyle?

One of my clients certainly did. They knew they didn’t have quite enough money and they didn’t want to scale back their lifestyle, work more or sell their home. As a result of seeing the commercial, we ended up modelling a few comparisons:

- Continue living in their home using a reverse mortgage versus selling their home at a future date and renting an apartment;

- Providing a blend of taxable and non-taxable income using a reverse mortgage versus all taxable income from a registered retirement income fund (RRIF);

- Delaying Canada Pension Plan (CPP) benefits until age 70 using a reverse mortgage versus using a RRIF to bridge the income gap between age 65 to 70;

- And, paying off a mortgage with a reverse mortgage versus keeping the mortgage.

iStock-1066106810.jpg

In most cases, the advantage, as measured by the largest estate value, went to the reverse mortgage. My clients and I were a little surprised at the results, but it all started to make more sense when we dug into the reasons why.

If you are not familiar with how a reverse mortgage works, both HomeEquity Bank and Equitable Bank provide good explanations on their websites to get you started. But, in general, a reverse mortgage is a loan, or a series of loans, that allow you to get money from your home equity without the fear of ever being forced out of your home.

Reverse mortgages take part of the equity in your home and convert it into payments to you, a kind of advance payment on your home equity. It is only for homeowners aged 55 years and older and you can borrow up to 55 per cent of the current value of your home, depending on your age.

Now, let’s look a bit deeper. For the different comparisons tested above, we assumed a reverse mortgage rate of five per cent. The current rates are between four and five per cent and the current bank prime is 2.45 per cent. We also selected a reverse mortgage requiring an initial loan of $25,000 followed by additional loans of $12,000 a year or more as required, rather than the more traditional account with a more significant upfront loan.

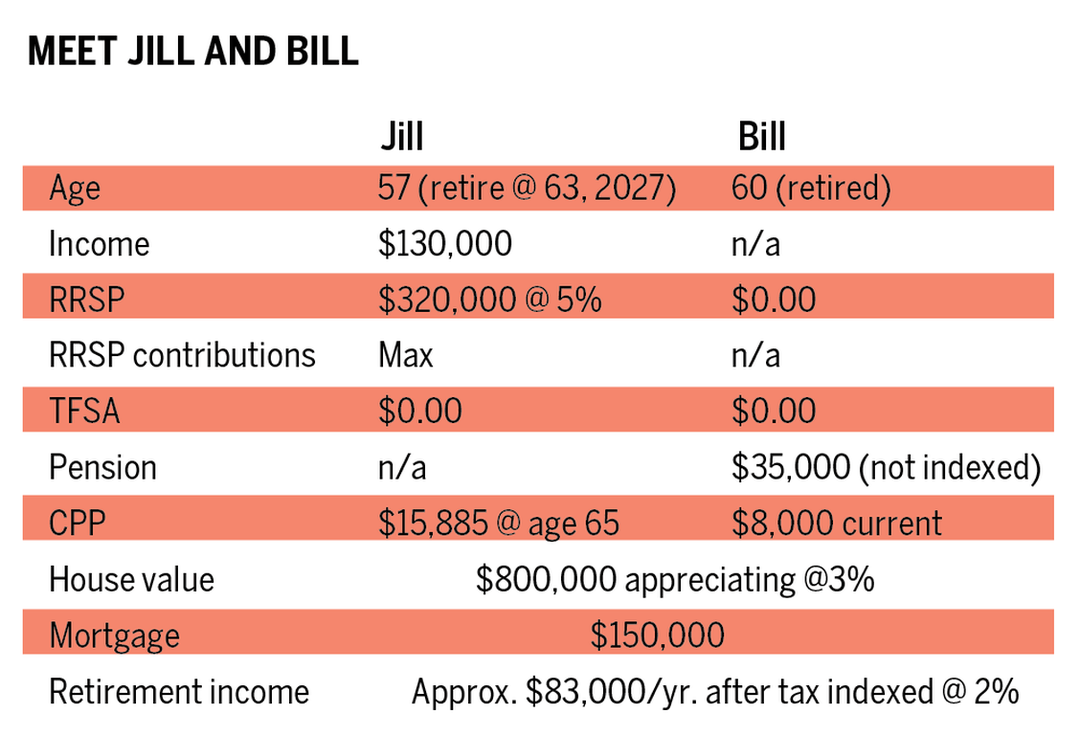

The clients’ details are as follows:

In Jill and Bill’s current situation, they’ll run out of money when Jill reaches age 81, although they’ll still have income from CPP, Old Age Security (OAS) and Bill’s pension, as well as a home worth $1,750,000. At age 81 (2042), we modelled selling the house, investing the proceeds at five per cent (made up of a combination of dividends and capital gains), and renting versus doing a reverse mortgage starting at age 81 (in 2042).

The final after-tax estate value in 2054, or age 90, for the former scenario was about $1.43 million, while the reverse mortgage came in at around $1.59 million.

Does it make sense that the reverse mortgage is coming out ahead?

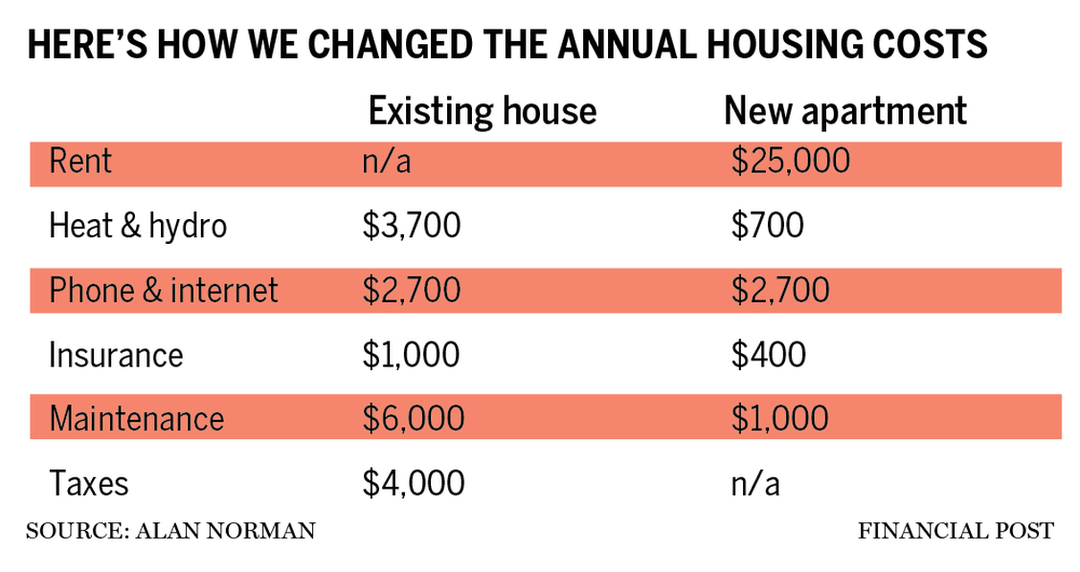

This is how we changed the annual housing costs:

The annual apartment expenses are lower than their home, but there is a $25,000 annual rent payment. In contrast, the amount drawn from the reverse mortgage in 2042 was $21,000 at five-per-cent interest ($1,050), which doesn’t have to be paid from investments and accumulates as part of the loan. With a reverse mortgage, you have the option of making payments, and the final loan will be paid off when the home is eventually sold.

In 2042, the home would be worth about $1.06 million and appreciating at three per cent ($31,920), resulting in a home value of almost $1.1 million in 2043. In this case, the home is appreciating faster than the loan is growing. Not only that, the home is appreciating in value tax free.

In selling the home in 2042 and renting, we assumed the proceeds would go into a non-registered account earning five per cent (again, made up of a combination of dividends and capital gains).

Tax is paid each year on the investment distributions and a larger capital gains tax is paid when the investments pass through the final estate.

In this case, it appears that the tax savings associated with accumulating wealth in a principal residence have overcome the interest accumulation of the reverse mortgage. If we had maximized tax-free savings accounts (TFSAs) rather than non-registered accounts, we would have seen different results.

For our second comparison, we wondered if it would make more sense to start a reverse mortgage when Jill turns 63 and then borrows $12,000 per year for the rest of her life. Our thinking was that the $12,000 would represent tax-free income, reduce the amount needed from RRIFs, and may open Jill and Bill up to more government credits and benefits. We also thought it would prolong the life of the RRIF.

We compared that to doing the same reverse mortgage, but selling the home, paying off the reverse mortgage, investing the proceeds and renting in 2041 when Jill turned 81.

In both cases, $12,000 per year was borrowed from the reverse mortgage starting in 2027. Borrowing stopped in 2041 for the sell, invest, rent solution. The after-tax estate value in the sell, invest, rent solution in 2054 was about $1.39 million, while maintaining the reverse mortgage through life grew the estate to $1.56 million.

In the end, there wasn’t much difference between our first comparison and our second comparison, and starting a reverse mortgage early in retirement or delaying it until RRIFs were depleted. We may have had a more significant result if my clients were closer to the guaranteed income supplement (GIS) or OAS clawback thresholds.

The third solution we modelled considered delaying Jill’s CPP until age 70 and using a reverse mortgage, rather than her RRIF, to supplement her income until then.

In this case, rather than comparing estate values, we compared the pre-tax net worth at Jill’s age 79 in 2043 when she would have depleted her RRIF if she had not done a reverse mortgage. We found that by using a reverse mortgage and delaying CPP and RRIF income to age 70, Jill and Bill’s pre-tax net worth was $1.9 million at Jill’s age 79, compared to $1.68 million if a reverse mortgage wasn’t done and Jill drew from her RRIF instead while delaying CPP to 70.

The final comparison we modelled was for fun. We wanted to see what would happen if Bill and Jill came into retirement with a traditional mortgage of $250,000 rather than their current mortgage of $150,000.

Does it make sense to pay off a traditional mortgage with a reverse mortgage when retirement starts? Our thinking was that if they have to make annual mortgage payments of $16,608, that money has to come from Jill’s RRIF. To get $16,608 after tax from a RRIF means having to draw about $23,700 when your marginal tax rate is 30 per cent.

Maybe it’s better not to draw that much from the RRIF and instead set up the reverse mortgage, stop making mortgage payments, and keep more money in the RRIF to accumulate.

We measured their pre-tax net worth when Jill reaches age 76 in 2040 and her RRIF is depleted, and found that it was $1.53 million if they kept the mortgage, and $1.6 million if they opted for a reverse mortgage.

Again, there is a slight advantage to the reverse mortgage.

We thought all the results were interesting. I’m not trying to convince you that reverse mortgages are fantastic and everyone should get one, but perhaps you should keep yourself open to the idea if your financial planner suggests a reverse mortgage or a similar approach.

One final note: the modelling of the different solutions assumed real estate values and investment returns will continue to rise. The reality is that they might or they might not. The purpose of modelling is to get you engaged in thinking, and participating. You may discover something new in these strategies that could put more money in your pocket after retirement.