Ron Lieber

Feb. 27, 2020

Ignore predictions and seek perspective.

When the stock market falls, as it has all week, there is a natural desire to search for explanations and consult crystal balls. While the spread of the coronavirus has been a catalyst, nobody knows exactly why the market moved the way it did, including whether underlying economic troubles are contributing to the severity of the gyrations. And nobody can tell you how the virus will affect the United States, including whether the outbreak’s short-term economic impact will reduce long-term profits.

And you are a long-term investor, right?

Most of us fall into that category if we are saving for retirement. We invest in stocks because doing so has consistently proved to be a good way to buy a little piece of capitalism. Hold on long enough to a diverse collection of stocks, and the system has tended to generously repay patient people over six or seven decades of working, saving and drawing down a portfolio.

Still, declines like the one investors experienced this week rarely feel good. And maybe you’re getting queasy about the economic implications of an outbreak that could force millions of Americans to shut themselves in for a while. If so, remind yourself of the following: Stocks are how your savings fight inflation, the market is not an absolute proxy for your personal finances, and you’re playing a long game — the very same points I raise every time we’ve worried about the stock market in recent years.

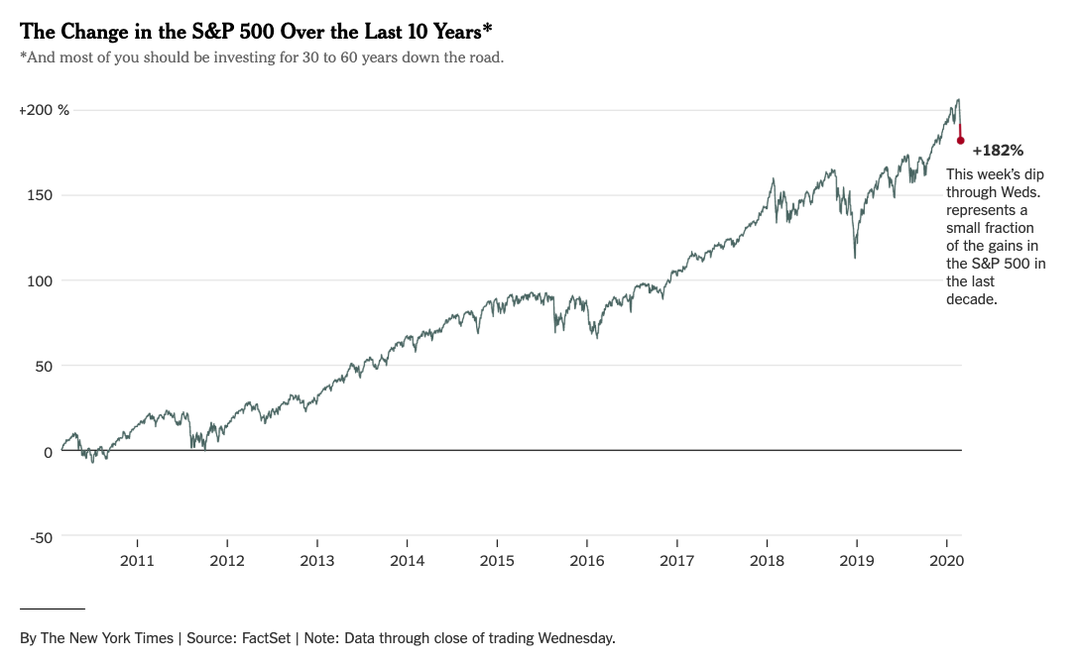

Look at that spiffy chart.

Isn’t it pretty? If you’ve been invested in the stock market for much of the past decade, all of that 180 percent-plus gain is yours on paper, even with a few rough days this week.

This is amazing.

Bull markets generally don’t last this long. Maybe this is the end, and if it is, so be it. Stocks will fall 10 percent and flatline for a while. Or maybe they drop 20 percent. Or 40. But wherever they bottom out and start rising again is likely to be higher than the average price you paid for your stocks over the past 10 or 15 years.

When people are yelling on (or at) the television, it always helps to stop and remind yourself why they’re doing it. Many of those TV yellers are professional investors trying to time the markets by selling high and buying low or on dips. Your goal isn’t the same.

Your aim is to find a way to put your money in an investment that will grow over time at a rate that outpaces inflation. And you want to do that without taking on so much risk that it could all go to zero and stay there.

Owning a big basket of stocks and paying very little for the privilege, say via an index mutual fund or exchange-traded fund, is generally the best way to execute this strategy.

That’s not going to change any time soon, because capitalism isn’t going anywhere. (If you’re worried about so-called socialism, we’re a long way from a potential Bernie Sanders nomination or presidency — let alone the implementation of any policies that could fundamentally alter the stock market.)

Defining net worth.

The phrase “net worth” is wrongheaded, as if the only reasonable sum of our financial selves is assets minus liabilities. Next year may bring a big market bounce, or a pay raise, and your capacity for earning more ought to be part of the equation. Besides, net worth need not equal self-worth.

Nevertheless, a positive and rising dollar figure is a fine thing. So take a look at the other pieces on the asset side of your equation. A decent chunk of it might be home equity. Did that fall a lot in the last few days? No? Good. Do you expect your bond mutual funds to fall as far as any money in stocks might? Again, probably not.

Remember, stocks are just a part of what you’re worth.

The horizon is a long way off.

Stocks are for the long haul: There are several decades between graduation and retirement (or a couple of decades between the arrival of a new baby and college graduation).

If you’re on the cusp of retirement, keep in mind that the big idea here is to live at least 20 more years, which is usually plenty of time for stocks to bounce back from even an extended decline in the stock market. (And things can indeed look grim for a while, as they did between 2000 and 2010 when U.S. stock prices for the biggest companies more or less made no upward progress even if you were investing your dividends along the way.)

If college for your children is imminent or you’re building a down payment fund for a house purchase in the next year or two, you probably shouldn’t have much money in stocks. Do you have money in a target-date mutual fund as part of a 529 college savings plan? Check to see how much of it is invested in stocks — and whether that figure makes you comfortable.

This may be your first big test.

If you’re in your 20s and just started investing in the past couple of years, I don’t envy you.

You may remember parents watching helplessly as half of their home equity and their retirement investments evaporated, at least on paper, after the 2008 financial crisis. If a parent also lost a job, and you took on perhaps more student loan debt than anyone in the family had hoped, it’s no wonder that you’d be reticent about investment risk.

A multiday decline, in your first few years of managing to put a bit of money away, can be harrowing. Putting long-term savings someplace safer is probably tempting, and perhaps it’s the only way for you to sleep better at night. But long-term returns in bonds will most likely be lower, so permanently moving money into them means you’ll need to save that much more to meet your goals.

Take your time.

Smartphone news notifications and television chyrons are insistent, and they suggest a kind of urgency. Even if they don’t explicitly say you should act now, it’s easy to feel that immediate action is necessary.

It isn’t. Not today, and probably not tomorrow, either. Plenty of people reading this will spend 75 years in the stock market, more if you count any college savings your parents invested for you when you were an infant.

So, stop. Think. Talk to someone with more experience, or a sober-minded approach. Shift a bit of your portfolio to cash if it helps your anxiety. But drastic investment moves are sensible only when there have been drastic changes in your life, like a big new job or consequential medical news. And that hasn’t happened for most of us this week.

Matt Phillips contributed reporting.

c.2025 The New York Times Company