By Veronica Dagher and Anne Tergesen

Aug. 11, 2023

No amount of money can make retirement worry-free, but $5 million might come close.

Retiree Pat Frey, in pink, regularly takes nature walks with a friend. REBECCA STUMPF FOR THE WALL STREET JOURNAL

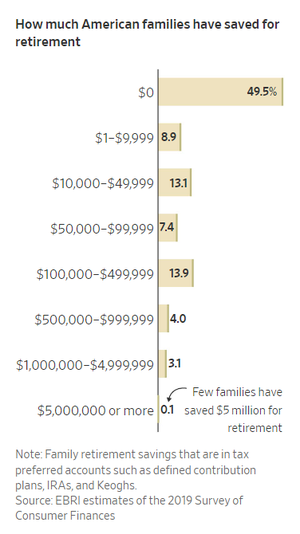

Few Americans manage to save anywhere near that sum in their 401(k)s and individual retirement accounts. A $5 million retirement nest egg puts you in the top 0.1% of households, according to an Employee Benefit Research Institute analysis of retirement accounts using the 2019 Survey of Consumer Finances.

To find out what $5 million buys in retirement, we spoke to retirees around the country with savings in that ballpark.

Most never expected to be multimillionaires but were diligent about saving from early on in their careers.

Though they are less concerned about outliving their money than many retirees we have profiled, they aren’t all living in luxury. Some haven’t bought new clothes in years. Others continue to work part-time.

They splurge on world travel but, like most older Americans, worry about their health and their families.

And money alone also doesn’t answer the other question retirees wrestle with: How to find purpose and meaning in this chapter of life?

PHOTO: JACK THOMPSON FOR THE WALL STREET JOURNAL

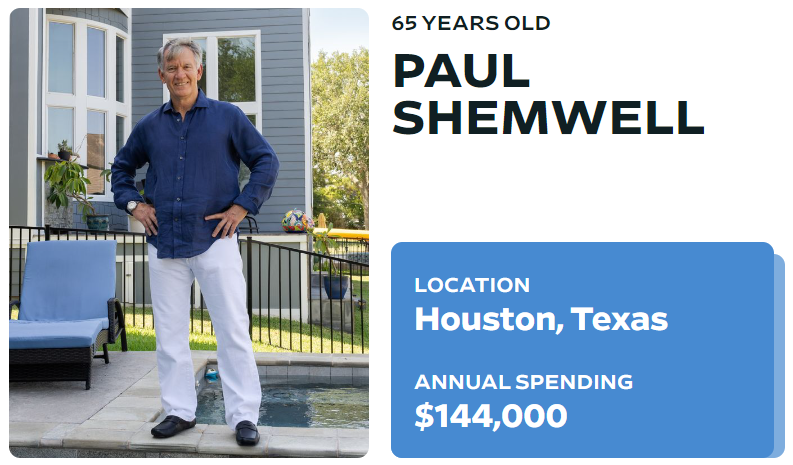

Paul Shemwell landed in retirement in December after four decades flying commercial planes and jet fighters.

Though the 65-year-old feels financially secure with about $6.1 million socked away, he hasn’t mapped out a flight plan for what comes next.

The casual approach is a big change for the former pilot, who honed his strategic thinking skills throughout his 13 years in the Air Force. His time in the service also taught him to weigh his options carefully, a philosophy that is guiding him in retirement.

He stopped flying after 28 years working for Southwest Airlines, but travel remains his passion. He has four trips planned this fall, wanderlust that costs him about $3,000 a month. He spends another roughly $9,000 a month on expenses such as property taxes and home and car insurance.

His days usually start with a workout or a tennis lesson. An avid skier, he already purchased a pass for this season and plans at least one scuba-diving trip a year.

Shemwell turned down several job offers to return to the cockpit, partly because he didn’t need the money.

He plans to take Social Security upon reaching full retirement age, which will add about $40,000 a year in annual income.

Life as an empty nester is another big change. His son is a sophomore in college and his daughter starts college this fall. Shemwell, who is divorced with joint custody, said he makes it a priority to be deeply involved in his kids’ lives.

His airline schedule gave him the flexibility to attend most of his children’s tennis and football games. Now that they are both away at school, he wants to travel to see them play.

Shemwell now spends more time with his friends, meeting them for lunch most weekdays.

He’s not an active trader yet follows the market. His portfolio is 95% stocks, mostly index funds, with a few individual equities such as Apple.

His father lived into his late 90s so Shemwell is unworried by his heavy stock allocation.

“My plan is to continue living within or below my means, stay invested and have something to leave to my kids,” he said.

Shemwell has roughly $300,000 left on the mortgage of his Houston home. He refinanced to a 2.99% interest rate so he is in no rush to pay down the debt.

He drives a 2016 Infiniti that has about 80,000 miles. The car, along with the used Mercedes he bought for his daughter, is paid for. He pays his credit-card bill in full each month.

“I like to keep things simple,” he said.

PHOTO: KATE MEDLEY FOR THE WALL STREET JOURNAL

Jay Myer built up enough savings to retire early from his software-sales career in 2020 after decades of maxing out contributions to his 401(k).

At 25, Myer read a book by Vanguard founder John Bogle that espoused low-cost index funds. He bought individual stocks, too, following the advice of renowned stock picker Peter Lynch to buy what you know. For Myer, now 61, that meant technology stocks and shares in companies he did software deals with, including Home Depot, which he purchased decades ago for a split-adjusted $3 a share.

“I was young to be reading about retirement, but it made a lot of sense to me. If you lower your investment cost, you’ll keep more of the profits,” said Myer, whose retirement account is invested in seven Vanguard index funds.

He and his wife, Anita, 60, drove used cars and stuck to a budget so Myer could contribute the maximum annual limit to his 401(k) account from age 22 on. Anita worked as a dental hygienist until their second son was born in 2000.

Myer said his decision to retire early was partly inspired by his stepfather, a small-business owner who enjoyed traveling and spending time with grandchildren.

“He showed me you could let go of the workplace and reidentify yourself,” said Myer.

Losing a steady paycheck was scary at first. When the market tumbled in 2020, he scrutinized the couple’s every purchase, down to the napkins, but quickly realized that doing so was unnecessary, given their healthy nest egg.

The couple now has $4.2 million, half in retirement accounts and half in taxable accounts.

Using the proceeds from the recent sale of their Atlanta home, the couple paid $925,000 for a house in Cary that is 2 miles from their older son’s family, who they see often.

They spend about $130,000 annually, including $5,000 on property taxes. Each month, they spend around $700 on food and $1,000 on health insurance. (Since they are currently spending from cash reserves, the couple’s taxable income is low enough to qualify them for insurance subsidies.)

To maximize his monthly benefit, Myer says he’ll wait to take Social Security until age 70.

The couple considered selling some individual stocks to put more into bonds but were deterred by the capital-gains tax they would owe on their profits. They decided instead to leave their biggest winners to their two sons.

The Myers, who budget about $20,000 a year for travel, are planning a trip to Spain, where their younger son is living this year.

Both love to cook and garden. Myer said he is enjoying unstructured time.

“Now that I have more time, I have learned to embrace boredom and slow down and accept sometimes that reading a book or riding my bike is enough,” he said.

PHOTO: RYAN YOUNG FOR THE WALL STREET JOURNAL

For Dr. Henry Hwu, work is part of what makes for a satisfying retirement.

While the Irvine, Calif., surgeon used to put in up to 80 hours a week, he now works part time and around his vacations. “And boy do I like to travel,” Hwu, 72, said.

An immigrant from Taiwan, Hwu said he and his late wife came to the U.S. in 1979. After studying surgery for five years in Chicago and completing a fellowship in colorectal surgery in Michigan in 1986, Hwu moved to Southern California, where he and his wife raised three children.

Before reaching his medical practice’s mandatory retirement age of 65, Hwu started reading books (and, he says, Wall Street Journal articles) about retirement. He took up golf and pickleball and bought a guitar, resurrecting a hobby he had had little time for since medical school.

But after retiring in 2016, he missed work and began accepting assignments at his former practice.

Every morning, he asked himself what he would do that day. “I didn’t like that feeling,” said Hwu, whose wife died just after he retired.

Hwu travels up to three months a year, visiting his 98-year-old mother in Taiwan or exploring Scotland, France, Germany, Japan and Switzerland, where he once bought so much chocolate for friends his suitcase broke.

Hwu often brings his guitar. While in London recently, he gave a street musician 20 pounds to step aside so he could play “Let It Be Me,” by the Everly Brothers. “I don’t know how people liked it, but there was an audience standing in front of me,” said Hwu.

Hwu still enjoys attending medical conferences and reading medical journals.

At a conference in 2017, he met the only surgeon at a rural hospital in Los Alamos, N.M. Hwu now travels to Los Alamos to relieve the surgeon for a few days most months. There, he enjoys hiking and seeing his son, an accountant in Albuquerque.

When home, Hwu takes guitar lessons and often sees his daughter and baby granddaughter.

His home is worth $1.5 million. He owns a second house, worth $1.2 million, that he rents for $3,500 a month. He owes about $500,000 on each house but isn’t rushing to pay his mortgages off because the interest rates are below 3%.

Hwu invests almost all of the more than $1 million in his retirement accounts in equity funds and individual stocks, including Apple, Microsoft and Nvidia.

He gets $2,700 a month in Social Security benefits, which he started taking at 65. He receives about $130,000 a year in pension payments and earned about $300,000 from his per diem work last year.

Travel is his big splurge, at $100,000 a year. Other expenses come to about $4,000 a month, not counting his mortgage payments.

He also pays $6,800 annually for a long-term-care insurance policy.

“With my mom living to 98, there will be a time when I am not able to take care of myself,” he said. “I want to cut down on the burden on my kids.”

PHOTO: REBECCA STUMPF FOR THE WALL STREET JOURNAL

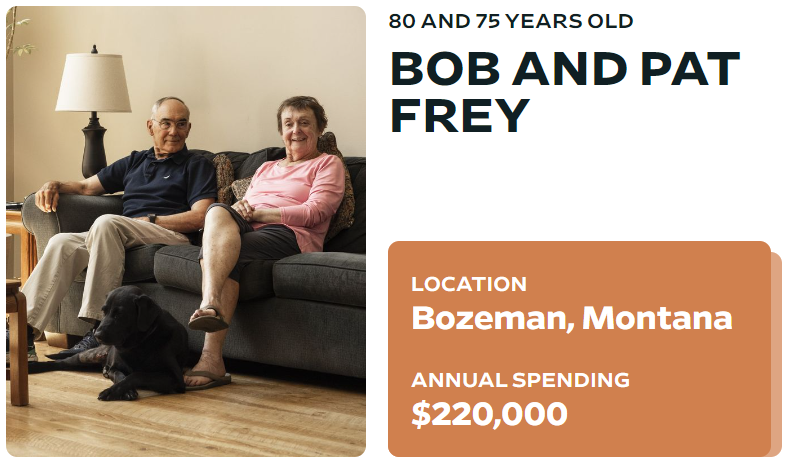

Growing up, Bob Frey never imagined he would retire a multimillionaire.

After graduating from West Point, he received his master’s degree while on active duty and then his veterinary degree with an Army reserve scholarship and the GI Bill. He spent 26 years as a reserve officer, retiring at age 60. He maxed out his retirement plan contributions starting in his 30s.

Times were sometimes tough, like when he borrowed about $150,000 to start a veterinary practice. He sold three businesses over the years, including two veterinary practices. These exits greatly added to his worth, he said.

These days, Bob, 80, and his wife, Pat Frey, 75, have socked away about $6.1 million, almost half of which is invested in individual retirement accounts.

Frey gets a $60,000 annual military pension, plus about $14,000 a year in veterans’ disability compensation because of hearing loss he developed after serving in Vietnam. The couple collects about $56,000 in total from Social Security.

“We have more money than we can spend in our lifetimes,” he said.

The couple, married for more than 30 years, have five adult children between them. They moved to Bozeman, Mont., in the early 1990s for a fresh start and to be closer to nature. Pat continued her nursing career and Bob retrained as a certified financial planner.

The Freys, despite their wealth, generally avoid its trappings. Bob said he hasn’t bought a new sports coat in about 20 years. Living in Montana, the couple said they don’t have much use for formal clothes and would rather knock around in jeans and sneakers. Pat frequently takes nature walks with a friend.

The Freys expect to spend about $1.5 million to help pay for the education of their nine grandchildren. They also donate roughly $40,000 a year to their favorite charities, including their church.

The couple have no debt and don’t tinker much with their investments, of which about 70% is invested in stock funds. They may leave about $1 million to charity upon their deaths, Bob said.

The Freys, too, value travel and allocate about $35,000 a year to seeing the world. They have visited New Zealand five times, and Bob often combines his love for fly fishing and travel on trips to Alaska, Mexico and South America.

They also enjoy separate trips with their friends. Pat regularly travels to Europe and the Galápagos Islands with a friend. She skips Bob’s hunting trips.

“I have no desire to sleep in a tent and carry an elk out of the woods,” she said.

Write to Veronica Dagher at Veronica.Dagher@wsj.com and Anne Tergesen at anne.tergesen@wsj.com

Dow Jones & Company, Inc.