By Ashlea Ebeling

July 10, 2023

It is becoming harder for older Americans to leave retirement savings to their grandchildren without sticking them with a big tax bill.

ILLUSTRATION BY ALEX NABAUM

Most heirs other than spouses must draw down inherited retirement accounts within 10 years, under rules that took effect in 2020. They used to have decades.

The timing change has grandparents ripping up their estate plans and drawing up new trusts to maximize their family’s after-tax wealth, financial planners and estate lawyers say. Some are also making immediate moves, such as embarking on a series of Roth conversions or making big generation-skipping lifetime-gifts.

A lot of money and taxes are at stake. Americans held $12.5 trillion in IRAs as of March 31, and 52% of households headed by someone 65 or older have one, according to the Investment Company Institute.

Linda O’Brien, an 83-year-old widow in Old Tappan, N.J., started converting her traditional IRA into a Roth IRA last year. She did this so that her children and grandchildren will inherit the money tax-free, instead of owing income taxes on the required distributions.

Once the money is in the Roth, it grows tax-free, and the grandchildren can take it out tax-free when they inherit it. Essentially she’s prepaying the taxes. O’Brien split her new Roth IRA three ways down the family tree, one-third each to two childless children, and one-third between two granddaughters, skipping over their mom.

“It would be foolish of me to leave that third to my daughter,” O’Brien said, noting that she doesn’t need it. Her grandson works on Wall Street and her granddaughter is a rising senior at Stanford University, so she’s not concerned that they’ll squander the money.

“This will give them a leg up,” she said.

Naming grandchildren as beneficiaries on individual retirement accounts used to be a popular estate-planning move before the 2020 changes because young heirs could stretch out annual required minimum distributions over their lifetimes.

The 10-year window changed the math. Now, inherited IRAs can cause a big tax bill, especially if distributions fall during the grandchildren’s, or their parents’, highest earning years. Minor grandchildren might need to file a tax return to report the IRA payouts, and the income could be taxed at the parents’ rate.

“Now the traditional IRA is one of our last options to leave to grandchildren,” said Mark Brown, an estate lawyer in Palm Beach Gardens, Fla.

Leaving a Roth IRA avoids some of the problems of the accelerated tax hit from an inherited traditional IRA. Grandparents can move money from a traditional IRA to a Roth and pay income taxes on the transfer.

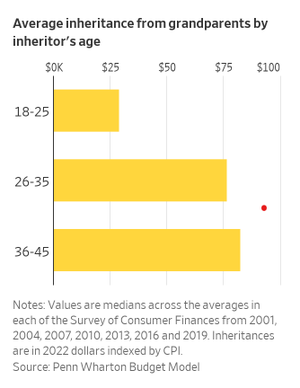

The odds of getting an inheritance from your grandparents are low, but of those who get one, the average amount is substantial, according to Jon Huntley, a senior economist at the Penn Wharton Budget Model. For example, those 18 to 25 had a 2% chance of getting an inheritance from a grandparent over five years, and it typically averaged about $29,000, Huntley found, using Survey of Consumer Finance data from 2001 to 2019.

Here’s more to consider when planning your legacy to your grandchildren.

Skipping a generation

Many grandparents start making lifetime gifts to grandchildren as soon as they are born, from paying for diapers and preschool to setting up college 529 savings plans and special trusts to save estate and generation-skipping transfer taxes. Part of the estate-planning discussion is how soon you want heirs to benefit and how much you want to control how they spend the money.

By leaving an IRA outright to grandchildren, even with the 10-year payout period, there is a danger that they’ll see the IRA inheritance as a windfall and the money can be gone quickly, said Caroline McKay, a senior wealth strategist at CIBC Private Wealth in Boston.

It is important to talk about how you would like them to use the money, for a house down payment or to start a business perhaps.

“The more transparency around what the money was meant for, the more likely they’ll respect the grandparents’ wishes,” she said.

Administrative headaches

Inherited IRAs come with complications for heirs beyond the required payouts. You can’t convert an inherited traditional IRA to a Roth IRA. You can’t add money to an inherited IRA. And you can’t combine an inherited IRA with your own IRA.

Some IRA custodians, including Schwab and Vanguard, make it easy for a minor inherited IRA to be set up with a parent or another adult named to handle the account until the minor reaches the age of majority, which varies by state.

In some cases, a guardian might need to be appointed by a court.

When to use a trust

Leaving an IRA in a trust brings more complications, but one reason to do it is if you have concerns about how your grandchildren or their partners might handle an inheritance. A trustee would distribute the money based on the terms you set out in the trust.

“Do you want the grandchildren to have all that money at age 18?” said Susan Hirshman, director of wealth management at Schwab Wealth Advisory.

For Ralph and Cindy Dorio, of Spring Hill, Fla., the answer was no when it came to their 20-year-old granddaughter who has a 1-year-old child.

They wanted their granddaughter to have her deceased mother’s share of their estate, including their IRAs. They split the IRAs 50-50 between her and her uncle, but they decided to leave her share in a trust with her uncle as trustee to manage.

“We’re not handing a million dollars over to her directly,” Ralph said.

Write to Ashlea Ebeling at ashlea.ebeling@wsj.com

Dow Jones & Company, Inc.