Neil Irwin

Feb. 5, 2021

Many parts of the GameStop story — the wild swings over the past couple of weeks in shares of the video game retailer and a few dozen other out-of-favor stocks — are not exactly new.

Long before Reddit, the Yahoo message boards of the late 1990s democratized the expression of strong opinions about stocks (they didn’t call them “stonks” in those days).

Short squeezes and market-cornering were maneuvers well before Randolph and Mortimer Duke — the fictional securities-fraud-committing villains of the 1983 comedy “Trading Places” — were greedy little boys.

What has been weird to watch, if you’ve spent your life plodding away at building a retirement fund, reading books about personal finance, weighing fee structures and tax implications of various investment vehicles, is the mix of righteous anger and gleeful anarchism driving it all. Many of the traders driving the GameStop mania in recent days want to strike it rich and bring down what they view as a corrupt, rigged system along the way.

Yes, there is abundant greed and venality on Wall Street. But the reality is that the stock market has also offered a path for ordinary people to build wealth — and more so in the last generation than ever before. You haven’t needed to burn down the system. All you’ve had to do is take the laziest, simplest approach to stock investing imaginable and have a little patience.

Ever since Vanguard introduced its S&P 500 index fund 45 years ago, ordinary investors have been able to invest in broad stock indexes in a tax-efficient manner, with extremely low fees. Any schlub on the street can put money to work harvesting a small share of the earnings of hundreds of leading companies, led by some of the sharpest corporate executives on earth and their millions of employees. You haven’t had to do much of anything!

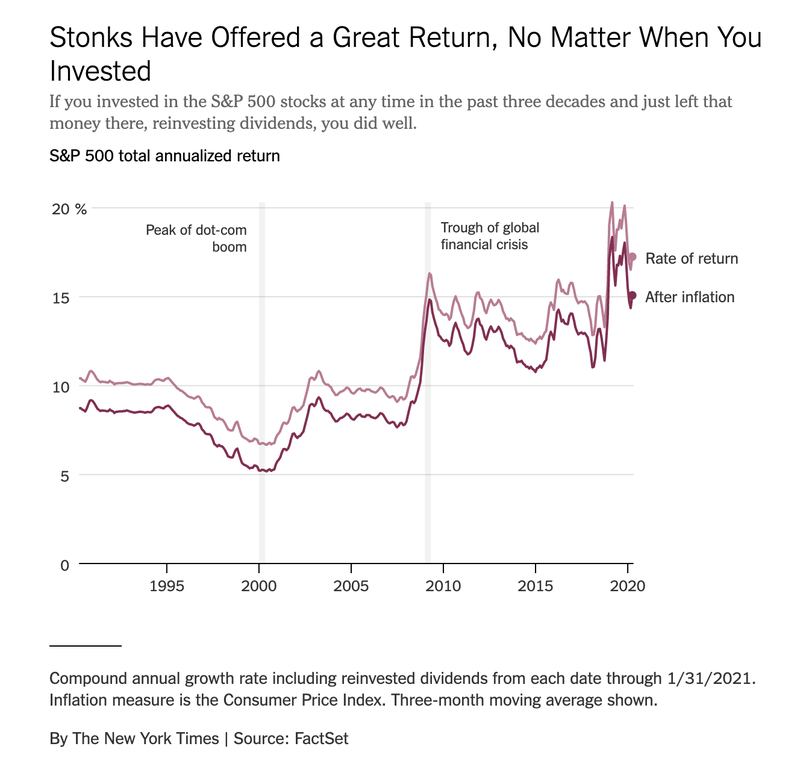

Your returns would have been strong even if you had terrible timing. Suppose you had received a $10,000 windfall in March 2000, the peak of the dot-com bubble and a moment at which we can all agree stocks were overpriced. Yet even with such unfortunate timing, if you invested that money in a low-fee S&P 500 index fund and reinvested dividends for the past 20 years, your $10,000 would have turned into nearly $28,000 by the end of this past month — a 5% annual return when adjusted for inflation.

And that was the single worst month in decades to begin investing. On average, if you were to select a month between 1990 and 2019 to begin investing, your annualized return through January 2021 would have been 9.8% after inflation. Simply for having the patience to sit on your hands.

(Those returns would have been reduced by a few hundredths of a percentage point by mutual fund fees, and more by taxes if the money was not in a tax-advantaged account.)

GameStop vs. Wall Street

Let Us Help You Understand

It gets better. Most people don’t receive and invest a single windfall, but rather chip in savings gradually.

So suppose you had begun saving $100 a month at the start of the year 2000 — again, near the peak of a bubble — and had continued doing so ever since, increasing your savings along with inflation, putting the money into an S&P 500 index fund and reinvesting dividends. Over the past 21 years, you would have contributed about $32,500, yet your portfolio at the end of January would be worth more than $103,000.

You achieved a 10.5% annualized rate of return, because while some of your savings was invested at market peaks, your slow-but-steady approach ensured you were also buying shares during periods when the market was depressed, as in 2002 and 2009.

As recently as the 1970s, this strategy would have been hard to carry out. Modern index funds didn’t exist until John C. Bogle invented the concept for Vanguard in 1976. Mutual funds in the past had much higher fees than they do today. Buying lots of different individual stocks would have required high brokerage fees as well, making it all but impossible for people with modest savings.

Moreover, the advantages of a “buy the index” approach were not as well understood until recent decades. Academic finance research in the second half of the 20th century had a series of findings about the efficiency of markets that, taken together, imply that the best long-term investing strategy for most people is simply to put money into the market as a whole and minimize fees and taxes. Personal finance advisers and commentators widely embraced this finding, with adjustments that depend on the investor’s risk preferences, particularly investing some slice of the portfolio in safer bonds.

The result: In recent decades, following the most obvious conventional wisdom of how to invest has been possible even for small investors.

If the market is rigged, it is rigged in a way that allows people to achieve a substantial return on their money by watching television or playing golf or taking a nap, rather than by spending their hours scouring message boards or developing elaborate theories of how to enact revenge on perfidious hedge funds or learning what the gamma of an option is.

Think of Corporate America — the hundreds of large companies in which you are investing if you put your money into index funds — as a sports franchise.

There are people who try to make money by betting for or against the franchise. They may put in lots of effort calculating proper odds and once in a while may win big, turning a small wager into a big score. The very best at this — the sharps, in sports betting terminology — will even win more than they lose and be able to make a living out of it.

But overall, the system is a zero-sum game, and most people who play are going to lose money once the sportsbooks’ cut is accounted for. If you decide to try to make a fortune by betting on professional sports, you might even conclude that the system is rigged against you, because in a sense it is. The consistent winners are going to be highly skilled sports bettors who have been doing this a long time; and the casino, which takes a share of every pot.

In this analogy, those fortune-hunting newcomers are the people who have taken to trading options on GameStop and other stocks in recent months.

Then there are people who work hard to make that franchise operate: the team executives, the coaches, the players. They put in long hours to make the franchise a success, and while part of their pay is linked to the franchise’s success, the bulk of their compensation is cash in exchange for their labor. They can be well compensated, but theirs are rare talents and they have to work really hard.

They are the equivalent of the executives and employees of the companies whose stock shares trade on public exchanges.

Then there are the passive owners of the sports franchise. For instance, the owner of a minority share who doesn’t even have to help hire and fire team presidents. Other people do all the work of running the team. These owners just enjoy the benefits of earnings, year after year.

It is not without risk: The franchise might sign an overpriced free agent, or ticket sales might collapse because of a pandemic. But if they are patient, they can expect that their investment will eventually pay off. And that is true even though they spend their time doing something other than examining point spreads and drawing up plays.

There are no guarantees in life. Some people who are aggressively trading meme stocks will presumably walk away with significant profits. Index funds won’t generate the kind of overnight payoffs that buyers of GameStop options are evidently looking for. And the decades ahead may offer lower returns to stock investors than the decades just past.

But the extraordinary payoffs of being a passive stock market investor are not something to overlook. When you are offered a free lunch — a reasonable expectation of good returns with zero effort and only moderate risk — it makes sense to eat it.

c.2024 The New York Times Company