By James Mackintosh

July 14, 2023

I’m confused. Contradictory economic gauges are telling different stories, standard leading indicators are in question, and markets appear to be prepping for both boom and bust.

ILLUSTRATION BY ALEXANDRA CITRIN-SAFADI; IMAGES: ISTOCK

To be fair, confusion should be the default state for anyone trying to predict where the economy or markets are heading. Overconfidence and inflexibility spell doom for investors, and I’m rarely sure about what to do. Still, these are unusual times.

The three most perplexing divergences are in finance, the structure of the economy and the way economic data is measured.

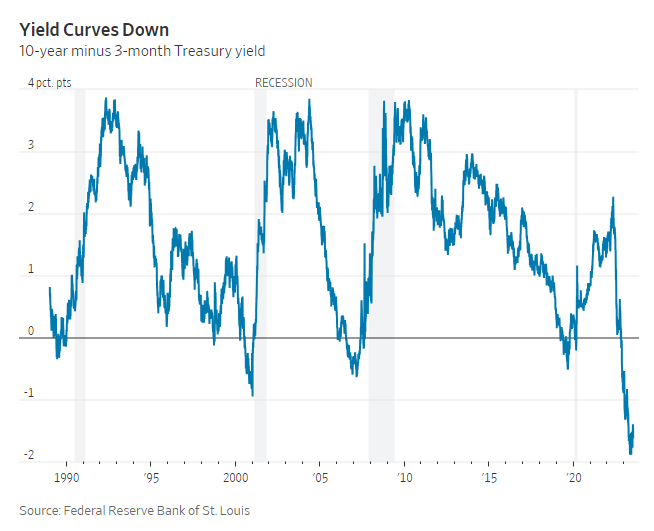

The financial divergence has received a lot of coverage, so briefly: Bond markets are predicting a slowdown, while stocks are readying for a decent economy.

Yields on long-dated bonds are far below those on short-dated bonds—in what is known as an inverted yield curve. Investors expect a lot of rate cuts, which has historically almost always been followed by recession.

Stocks have been rallying since May, and the S&P 500 is up more than 20% from its October low. While it is possible to quibble (equal-weighted to reduce the impact of the giant tech stocks, the S&P is up less, as are smaller stocks), the gains have been led by cyclicals most exposed to economic growth, with defensive sectors lagging behind. The stock market expects a soft landing for the economy.

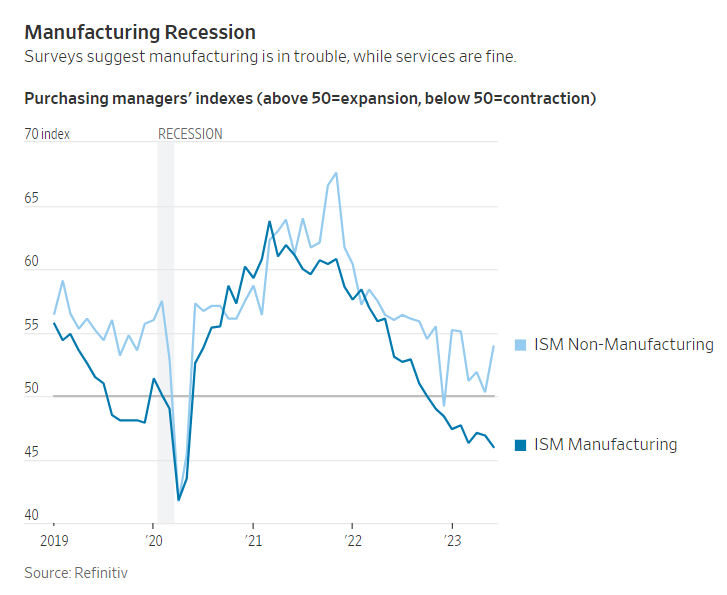

The split in the economy shows up as manufacturing in trouble while services boom. In itself this isn’t a problem—there are always winners and losers. But manufacturing has historically acted as an early warning of the state of the economy, so it gets far more attention than its current low share of GDP would otherwise justify.

The gap between the Institute for Supply Management’s manufacturing and services surveys is the third-largest since the services gauge was created in the late 1990s. The survey shows manufacturing contracting at a pace usually seen only in recession, and it is getting worse; only three times since World War II has industry been this bad without triggering a recession. Meanwhile, services are expanding and getting better.

Construction is also divided. New private housing permits and housing starts had fallen at a speed rarely seen outside recessions as higher interest rates started to bite and the postpandemic building boom faded, although they have rebounded a bit recently. Yet, overall construction spending is at a new high, helped by a 76% year-over-year leap in new factories, widely attributed to Inflation Reduction Act subsidies.

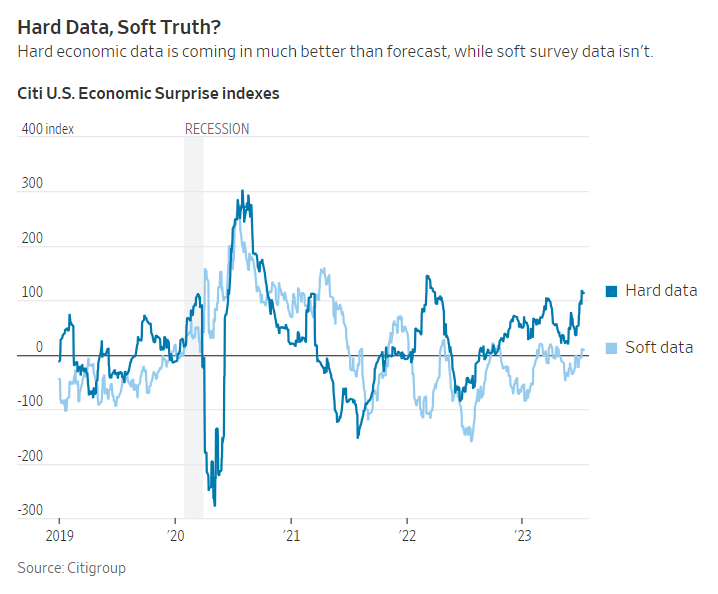

The measurement of these divides is itself divided, depending on whether the numbers come from “soft” sentiment or “hard” data. The ISM survey is soft, as it measures opinion; unemployment or industrial production relies on hard numbers.

Figures compiled by Citigroup show that hard data has been coming in well above expectations all year, while soft surveys disappointed compared with forecasts most of the time, although they are now slightly better.

Even within hard data, measures show both good and bad times. GDP has been growing, but if you calculate the size of the economy from income instead of spending, known as gross domestic income, it fell for each of the past two quarters. The two measures ought to be the same.

Each divide can be explained. Manufacturing is in the doldrums because of pandemic-related swings, which led to a boom in production followed by a sharp fall as demand shifted to services. Housing is sensitive to interest rates. Subsidies naturally encourage activity. The national accounts are hard to measure and subject to large revisions years after being published.

Gerard Minack, of Minack Advisors in Sydney, says the bond market always looks further ahead than the stock market, so the financial divide is more about current strength against future slowdown. He still predicts a recession.

Similarly, the hard/soft divide is related to the consensus late last year that recession was on the way. The negative mood showed up as poor sentiment in the surveys, but the continued strong demand meant that the layoffs and spending cuts that usually follow haven’t happened.

Spencer Hill, an economist at Goldman Sachs, calculated that the average error in using 19 business surveys to predict GDP growth over the past two years was twice as high as in the two years before the pandemic, which he says can be explained by depressed sentiment. He argues that less weight should be placed on these indicators as a result, and thinks the economy is stronger than the surveys suggest.

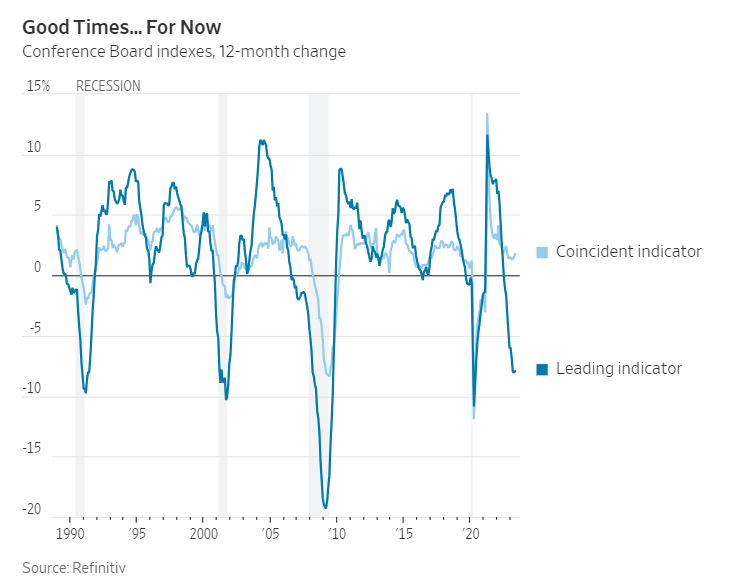

Composite indicators attempt to combine a number of measures to produce a forecast, with the Conference Board’s leading indicator pointing solidly to recession in the near future, even as its coincident indicator says everything is fine at the moment. But if the individual measures underlying the composite are doing unusual things, maybe combining them produces a less reliable forecast than usual.

Investors left scratching their heads over all this should just diversify across cyclical and defensive stocks and bonds in the hope of doing OK, but not great, in any scenario.

I remain concerned that trouble is on the way, but am confused enough by the postpandemic weirdness that I’m inclined to avoid significant bets on the economy. Even if you can see a clearer way to the future, the fog around the signposts suggests it is worth keeping your portfolio nimble, just in case.

Write to James Mackintosh at james.mackintosh@wsj.com

Dow Jones & Company, Inc.