IAN MCGUGAN

April 18, 2022

We all wonder how any middle-class earner can buy a house at today’s prices. But our indignation on that point may be reducing our focus on an equally important question: Even if you can afford to buy a house, should you?

The answer hinges on what you think will transpire over the next couple of decades. If home prices continue to surge higher, homeowners will grow richer and richer while renters fall even further behind.

But if home prices stagnate or even fall over the next couple of decades, the reverse is true. People who have strained to gain a foothold in today’s real estate market will face years of zero or negative returns on their investment. The truly lucky people will be those who avoided buying a house at today’s lofty prices.

So which is it? In talking to housing market experts in recent months for other stories, I’ve been struck by how unsure even the gurus are about the long-term outlook for home prices. As one economist said to me, “There is no more efficient way to look like a fool than to make a housing price forecast.”

Absolutely true. So, allow me to put on the dunce cap and sum up some of the views I’ve encountered.

The case for a big fall

Housing bears have argued for years that Canadian real estate is absurdly overpriced when compared with historical norms. After the enormous gains of the past two years, their case is stronger than ever.

“The outlook for affordability is grim,” Royal Bank of Canada warned in a recent report. The total cost of home ownership – including mortgage payments, property taxes and utility bills – is now at its highest level compared with median incomes since 1990, by the bank’s calculations.

If this ratio were to move back toward its long-term average through a decline in home prices, some local markets could be hard hit. Halifax home prices would have to tumble 26 per cent just to get back to the level of affordability that prevailed at the end of 2019, RBC estimated. Ottawa property would have to slide 24 per cent and Toronto real estate 22 per cent.

The most likely catalyst for declines would be significantly higher borrowing costs. In early 2020, the Bank of Canada dropped interest rates to nearly zero to cushion the economic blow of the pandemic. That gusher of essentially free money helped propel home prices more than 30 per cent higher over the next couple of years.

The gusher is now dry. In an emphatic reversal of its pandemic-era policy, the Bank of Canada doubled its key policy rate this week and signalled more hikes will follow.

Higher interest rates are unlikely to shake the housing market so long as households continue to bask in a robust jobs market and pandemic wealth. Over the longer run, though, Canadians are painfully exposed to every upward tick of monetary policy.

Household debt has now reached a record 186.2 per cent of household disposable income, compared with 181.1 per cent just before the pandemic and 152.6 per cent at the time of the financial crisis in 2008, according to Statistics Canada.

Given that towering level of indebtedness, any sustained move toward higher interest rates could threaten Canada’s housing bonanza.

The case for more gains

Housing bulls like to take a global perspective. They argue Canada’s housing prices may be high against their own history, but aren’t outrageous compared with international rivals.

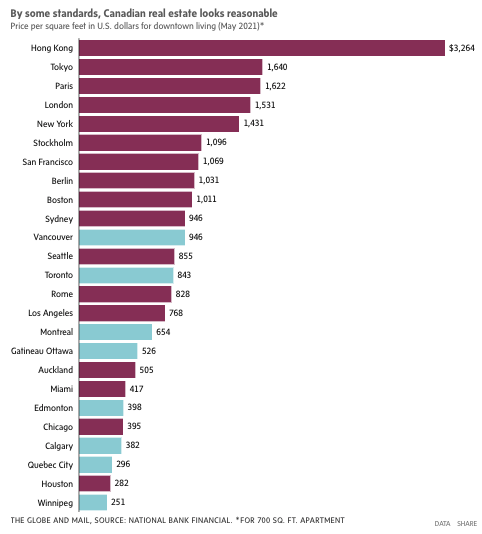

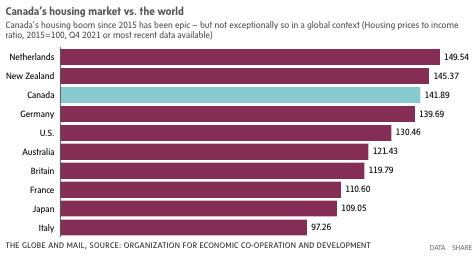

A 700-square-foot apartment in prime areas of Vancouver and Toronto costs less than in places such as Boston, Stockholm, and Berlin, National Bank Financial estimates. When calculated in terms of home prices to household incomes, the run-up in Canadian housing prices since 2015 is high, but not outlandishly so when compared with other advanced economies, according to data from the Organization for Economic Co-operation and Development.

For now, strong demand continues to support Canadian home prices. The federal Liberals have substantially boosted Canada’s immigration target to more than 400,000 newcomers a year. Yet Canada is building significantly fewer new homes per capita than it did back in the 1970s and ’80s. As long as we continue to construct only 200,000 or so new units a year while admitting 400,000 new Canadians, it is difficult to see how home prices can slide too far.

Could a burst of new construction change this picture? The federal government’s Budget 2022 included a program to accelerate housing development, but much of the real power in this area resides with provinces and municipalities. It is those levels of government that control zoning restrictions and building permits. Until they move, not much will happen.

Some provinces are thinking about it. A recent Ontario task force on housing affordability suggested the province sweep away many restrictions on new construction and set a bold goal of adding 1.5 million homes over the next 10 years. For now, though, that remains a recommendation, not policy.

The bottom line

From under my dunce cap, the outlook for home prices over the next two decades seems moderately unattractive. Strong demand will continue to offer support, but higher interest rates are likely to constitute a powerful headwind. Over the longer haul, political pressure to do something about home prices is likely to result in more construction and more supply.

This doesn’t mean buying a house right now is necessarily a bad idea, but it does suggest future gains are unlikely to repeat the boom of the past few years. New buyers may want to keep their hopes in check.

This Globe and Mail article was legally licensed by AdvisorStream.

© Copyright 2024 The Globe and Mail Inc. All rights reserved.