Duncan Rolph

March 10, 2020

The coronavirus’s impact on the stock market has ignited meaningful conversations between clients and advisors who have become inured by thoughts of 2008. But for those of us whose businesses were born from the ashes of that recession, there’s a different mindset on risk tolerance. The biggest one-day stock market drop in history didn’t come from a business flaw or Wall Street malfeasance – it got a virus . The coronavirus and the shutdown in China were jolts that woke us up to shockwaves hitting the global economy. This comes during the longest bull market in history and strong appreciation in equities in 2019, even when many asset classes have been considered fair to over-valued. It’s tough news but not critical for the well-managed portfolio where risk analysis has made portfolio advisors reduce equity exposure for their clients. No one could have predicted the coronavirus but past is prologue, and it’s time to reflect on what we can learn.

Learning from the Past

The last time a health scare hit China was in 2003, and it proved to be nothing more than a blip. However, 20 years of globalization – led mostly by China – has created a much more interdependent world today. In 2003, China accounted for 4% of global GDP, but today it’s over 17% and growing. Therefore, the impact of China’s economy can quickly cause a ripple effect across everything from iPhones to car parts because most multi-national companies have global supply chains. These disruptions interrupt sales and detract from company earnings and ultimately, their stock price. Additionally, if the coronavirus spreads globally, it will also impact consumer demand. People don’t go out to dinner, don’t take vacations, don’t go shopping or attend conferences.

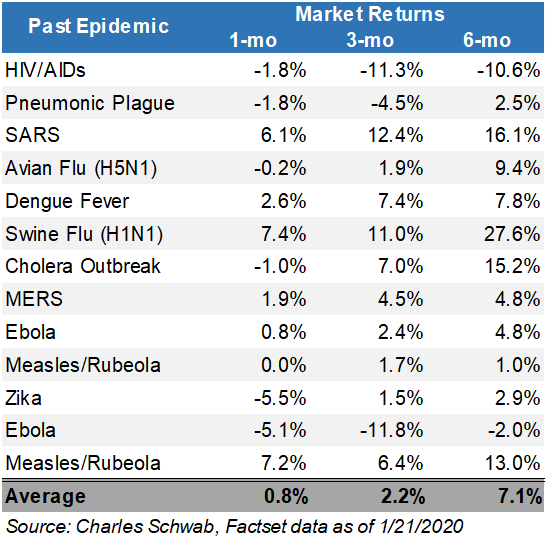

While it is too early to tell the extent to which the virus will hinder global growth, a prolonged slowdown will meaningfully increase the chances of a recession later this year. However, historically, markets have bounced back from global health crises as denoted in the chart below.

Past epidemic market returns

Cheap Money

Given the massive disruption to the global economy caused by the coronavirus, the Fed’s response was to reduce rates by 50 basis points. This brought the 10-year Treasury to a record low hovering just above 1% and means that there is a reasonable chance that the U.S. could join most of the world in experiencing negative yields.

The entire premise of investing money is that the investor expects to make a profit — the higher the expected return, the higher the risk. So, asking someone to invest in a bond that is guaranteed to lose money is hard for most people to even comprehend. After the Great Recession, the U.S. experienced a decade of “cheap money” that has warped most of the world’s capital markets. Investors, especially those with significant cash flow needs such as pensions and retirees, were willing to overlook anemic bond returns because the stock market has more than made up the difference. However, the coronavirus and the growing risk of a global recession have suddenly called that Faustian bargain into question. The problem with negative yields is that it can create a low-return environment for a decade or more, not just a year or two. Changing an investor’s long-term expected rates of return over the long-run has a dramatic impact on the math and in many cases, it just doesn’t work anymore.

Looking Forward

Equity markets had an incredible year in 2019 with the S&P 500 up over 30%. The surge was mostly due to the rebound from the sell-off in December 2018, record low unemployment, and more accommodating interest rate policies from central banks across the globe. Over the last few months, we evaluated that stock prices were exceeding their fundamental valuations compared to historical norms. In response, we reduced equity targets across many accounts and increased exposure to areas of the market that were more defensive in nature such as high-quality multiple/corporate bonds, longer duration U.S. treasuries, structured notes, and cash equivalents. These allocations have dampened losses from the recent equity sell-off.

Looking forward, the fundamental drivers of equity market gains are still in place, such as the strong U.S. labor market and an accommodating Fed policy. However, the coronavirus has clearly impacted Q1 output and companies are already lowering their revenue and earnings estimates.

While it is too early to assess how it will ultimately impact global stocks, the recognition that the coronavirus is closer to becoming a pandemic is causing a meaningful repricing of risk. It is important to watch and see if the current sell-off creates any buying opportunity to invest in areas of the market that may be mispriced or if this is the start of a more prolonged correction.

This article was written by Duncan Rolph from Forbes and was legally licensed by AdvisorStream through the NewsCred publisher network.

© 2024 Forbes Media LLC. All Rights Reserved

This Forbes article was legally licensed through AdvisorStream.