Ian McGugan

Aug. 2, 2020

The single biggest challenge facing savers these days isn’t the pervasive uncertainty around the scary new coronavirus. Rather, it is the growing certainty of low returns from tried-and-true investments.

For years, bank accounts and guaranteed investment certificates have offered dismally low payoffs. Now stocks and bonds are also poised to underwhelm expectations.

“Stocks’ prospective returns have come down considerably,” warns Jeremy Siegel, a professor of finance at the University of Pennsylvania. To make matters worse, “bonds’ prospective returns have come down an awful lot more.”

Back in 1994, Mr. Siegel published Stocks for the Long Run, an upbeat investment classic that argued just about everyone should own equities. Today, he still sees an overwhelming case for stocks, but cautions that investors have to dial back their hopes for big returns from either stocks or bonds.

He estimates that a conventional balanced portfolio, consisting of 60 per cent stocks and 40 per cent bonds, is likely to produce a “real,” or after-inflation, return of a mere 2.5 per cent a year over the decade ahead.

This is only about half the payoff that Canadian and U.S. investors are used to reaping from a traditional balanced portfolio, Mr. Siegel says. It is also below what many people need to finance their retirements.

He is not the only one warning of the growing gap between what investors need to hit their goals and what markets are likely to deliver.

“The returns from the type of portfolios that people are traditionally comfortable with are going to be very low,” says Adam Butler, chief investment officer at ReSolve Asset Management in Toronto. “In fact, they are going to be so low that it is nearly guaranteed that investors will not be able to hit their return targets by investing in the portfolios they have come to know and love.”

“This is an expensive market,” says Kendra Kaake, director of investment strategy at SEI Investments Canada, which offers investment management services to institutional clients.

The above-average returns of recent years, especially by U.S. stocks, have effectively borrowed profits from the future, she says. As a result, the return expectations for many portfolios “are going to be anemic” for several years to come.

So what can investors do in this unpromising environment?

They can start by recognizing there is no surefire way to deal with the radical uncertainty that hangs over financial markets in an era of pandemics and unprecedented central bank intervention.

Some authorities argue that investors should embrace more risk to offset the high probability of lower returns ahead. Others recommend leaning in the direction of “factors” that have distinguished winning stocks in the past. Still, others urge investors to take a new look at areas such as commodities, gold and cash.

All these ideas may have merit. But before deciding which approach to take, investors may want to take a step back. Understanding the forces that are dragging prospective returns lower can help savers navigate what lies ahead.

The story behind today’s low return environment begins in the early 1980s, when central bankers in Canada, the United States and other countries raised short-term interest rates to punishing levels – more than 20 per cent in many cases – to cudgel inflationary expectations.

Central banks’ tough-guy act had the desired effect. Both inflation and interest rates have been in steady decline ever since.

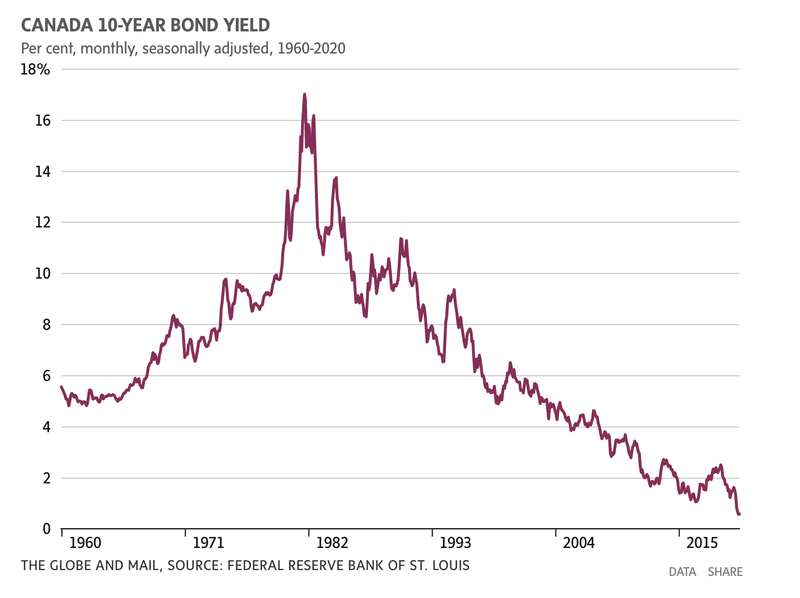

For investors, the long slide in borrowing costs has been a mixed blessing. Among the collateral victims of falling interest rates have been the quoted initial yields, or “coupon rates,” offered by bonds. They have tumbled to a fraction of their old levels.

“Two decades ago, we were clipping 6-per-cent coupons from 10-year government bonds,” Ms. Kaake says. “One decade ago, we were clipping 3.5 per cent. Today, that is below 1 per cent.”

Falling bond yields go a long way to explaining why the potential returns from a balanced portfolio are now so dismal. The benchmark 10-year Government of Canada bond currently pays a mere half a percentage point in interest a year. That feeble payout is not enough to offset the annual bite of inflation, let alone deliver any real return.

Amazingly, though, Canadian yields actually look generous compared with rates in Europe or Japan. In those countries, yields have turned negative across a broad swath of the fixed-income universe. Savers now have to pay a stiff penalty for the privilege of saving.

Why are so many people around the world so eager to hoard bonds despite such miserable payoffs? Economists have produced a long list of possible explanations.

Falling yields may reflect a global savings glut. Or aging workers’ willingness to hold safe assets at any price. Or growing inequality and the desire of the uber-wealthy to keep their fortunes in the most secure assets possible. Or simply a lack of attractive investment opportunities elsewhere.

Whatever the deep roots of lower rates, most policy-makers are eager to ensure that rates remain at near-zero or even negative levels. Since the financial crisis a decade ago, many central banks have hoovered up bonds in an effort to keep a lid on yields. (Bond yields move in the opposite direction to bond prices, so persistent bond-buying by monetary authorities pushes down yields, everything else being equal.)

One reason central banks want to restrain yields is because low payoffs on bonds help to boost the appeal of competing assets, such as stocks and real estate. By driving up the prices of these other assets, low bond yields encourage risk-taking and economic growth.

However, low yields can propel stock prices only so far. Wall Street now looks exceptionally expensive on many metrics.

Its dividend yield, for instance, is unusually low compared with its own history. Meanwhile, its total value relative to the underlying U.S. economy is exceptionally large. The q-ratio, which calculates how the stock market’s value compares with the replacement value of its assets, is in red-alarm territory. So are various measures of share prices versus long-run underlying profits.

“That doesn’t mean stock prices necessarily have to fall from here,” says Larry Swedroe, chief research officer at Buckingham Wealth Partners in St. Louis and author of several books on the science of investing. But it does suggest the scope for future gains is limited, barring even deeper cuts to interest rates or an unusual surge in profitability.

Investors should be cautious and prepare for a wide range of potential outcomes, Mr. Swedroe says. Among those possibilities is a protracted swoon in the stock market.

History shows it is not unusual for stocks to sputter for a decade or more. Over the past century, there have been three periods of at least 13 years when stocks failed to keep up with riskless short-term government securities, he notes. From 1929 to 1943, from 1966 to 1982, and from 2000 to 2012, stocks produced worse returns than keeping your money in cash equivalents.

“To put that another way, bonds beat stocks in 45 of the past 91 years,” he says.

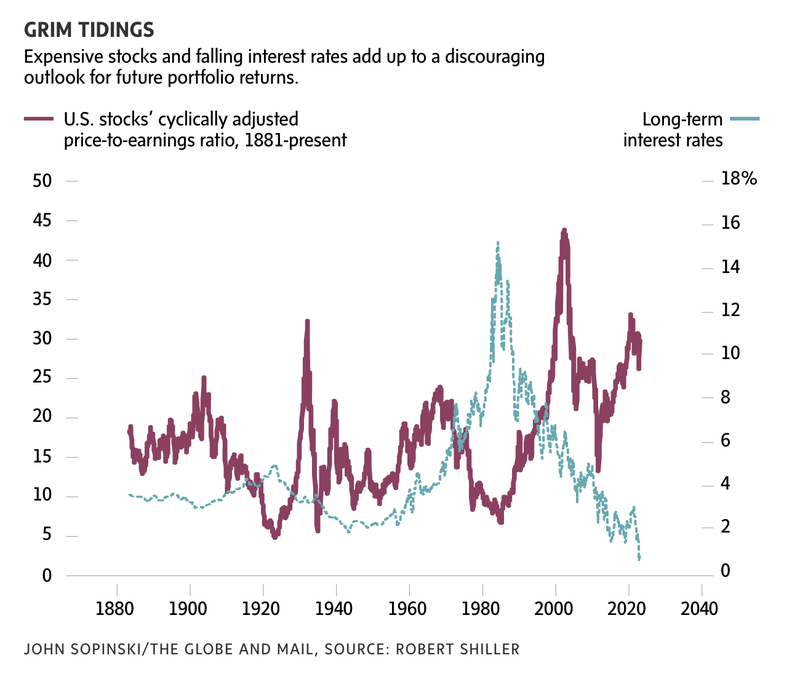

Could we be on the brink of another such period? One of the more reliable ways to detect brewing problems is to look at how today’s share prices stack up against the long-run earnings power of the companies represented in the market. This metric, which compares current share prices with underlying corporate earnings over the prior decade, is known as the cyclically adjusted price-to-earnings ratio, or CAPE.

Over the past century, there has been a reasonably strong relationship between CAPE and subsequent returns. When CAPE is low, stocks are cheap and future returns tend to be strong. When CAPE is high, stocks are expensive and future returns often disappoint.

The CAPE ratio stood at 26.5 in mid-July, according to a recent Goldman Sachs report. That is well above its long-run average of 17. The elevated current reading suggests stocks will post an annualized return of only 2.7 per cent over the next decade, according to Goldman analysts.

To be sure, CAPE is far from a perfect indicator. The Goldman team also explored four more optimistic approaches to valuing the market. They concluded that U.S. stocks are likely to generate a nominal return of only around 6 per cent a year over the decade ahead, including both capital gains and dividends. That would be less than half of the 13.6-per-cent-a-year return they averaged over the past decade.

Investors should note that the 6 per cent projected return is not adjusted for inflation, taxes or management expenses. Subtract those costs and the real prospective payoff from holding today’s hottest stock market looks tepid indeed.

How you view this situation depends on your attitude toward risk.

Mr. Siegel, for instance, sees a strong case for holding even more stocks than usual. He suggests investors move from a classic 60/40 blend of stocks and bonds to a mix of 75 per cent stocks and 25 per cent bonds. In his recommended asset allocation, dividend-paying stocks replace some of the space that used to be devoted to bonds.

This is not because he expects stocks to do well versus their historical averages. In fact, he agrees stocks are primed to produce lower-than-normal returns. However, he argues that the extra return an investor earns from holding stocks rather than bonds – the equity risk premium, in the jargon – has moved to unusually wide levels.

Investors have historically reaped about 3.5 percentage points of extra return from owning stocks, he says. Right now, the gap is more like six percentage points in real terms.

At today’s yields, bond investors are locking in a real return of about negative 1 per cent, Mr. Siegel says. Stock investors, in contrast, are likely to derive something more like a 5 per cent real return. To his way of thinking, this unusually large equity risk premium argues for holding an uncommonly large percentage of stocks in your portfolio.

But doesn’t holding a lot of stocks also increase the volatility of your portfolio? Maybe so, but Mr. Siegel says a 75/25 asset allocation actually reduces risk over all, especially for retirees who are drawing down their portfolios.

“We have done simulations, and with the gap between stocks and bonds being as high as it is, the probability of running out of money is actually lower with a 75/25 portfolio than with a 60/40 portfolio,” he says. “The reason is that you are getting so much extra income that you are more than offsetting the extra volatility.”

Not everyone is convinced by this logic. Dan Bortolotti, a portfolio manager at PWL Capital, a wealth manager in Toronto, says one of the most common mistakes that investors make is to overestimate their capacity for handling volatility. He recalls the panicked calls he received in March from clients who wanted to move their portfolios into cash after markets tumbled.

“No one cares about simulations or standard deviations when markets are crashing,” Mr. Bortolotti says. “They care about downside protection. And they think about the potential downside in terms of dollars, not percentages. If my portfolio fell $200,000 in March, that is the only number I care about.”

He agrees potential returns from bonds are extremely low, but argues that investors who view bonds purely from a return perspective are missing the point. “The reason we hold bonds is not to provide optimal performance in theory,” he says. “It is to put a damper on volatility so we can sleep at night. That doesn’t change when interest rates are low.”

In today’s low-rate environment, investors often reach for alternatives that aren’t really alternatives, he notes. The most common example is using dividend stocks as a replacement for bonds. While both may offer a yield, they act in very different ways during a crisis.

Bonds tend to hold up well in market downturns and can actually generate capital gains if interest rates fall. In contrast, dividend stocks usually fall in line with the overall market and sometimes get hit twice – once in the market plunge and then again when the company cuts its dividend.

The difference between the two assets was illustrated in March, when bonds soldiered through the market downturn with only modest losses while dividend stocks plummeted.

“Low bond yields are not a problem that is easily solved,” Mr. Bortolotti says. “You cannot simply choose another investment with a higher potential return and not expect it to affect the volatility of your portfolio.”

There may be no consensus about the best strategy for a low-return economy, but there are lots of intriguing ideas.

Mr. Swedroe, the financial author, suggests investors should tilt their stock holdings toward equities that display characteristics, or factors, that have historically been associated with stronger returns.

One example is the value factor. Buying stocks that trade at low multiples of earnings and cash flow has generated above-average returns across most periods. It has not worked well over the past decade, but its protracted underperformance could signal that a resurgence is near.

For his part, Mr. Butler of ReSolve stresses international diversification. He points out that Canada’s stock market accounts for only about 2 per cent of global stocks. Focusing too much on Canada is likely to hurt returns, he says.

He also recommends thinking beyond the usual stock-and-bond categories when it comes to constructing your portfolio. “The future may not look a lot like the past 30 years,” he says. Especially if inflation stages a comeback, holding commodities, gold, cash and real-return bonds could help boost portfolio returns.

For older investors, it also makes sense to explore annuities. Bonnie-Jeanne MacDonald, director of financial security research at the National Institute on Ageing at Ryerson University, notes these products can be an effective way for retirees to generate a safe income, especially if leaving a bequest is not a top priority.

The best way for Canadians to acquire an expanded annuity is simply to delay the start of their Canada Pension Plan benefits. Putting off CPP from 65 to 70 results in a nearly 50-per-cent jump in the monthly payout a retiree will receive. Better yet, that payout is inflation-protected and fully guaranteed by Ottawa. “It is the safest, most inexpensive pension that money can buy,” Ms. MacDonald says.

Another excellent piece of practical wisdom comes from Mr. Swedroe. He notes that investors tend to dwell too much on pure market considerations. By doing so, they create false alternatives for themselves. They often wind up taking on more risk than they can bear in pursuit of the returns they think they need.

“You shouldn’t ratchet up your risk to uncomfortable levels simply because returns look like they’re going to be lower than historical averages,” he says. “You have a lot of other levers to pull first. Working longer? Saving more? Those can be your best strategies, and they work in any sort of economic environment.”

FIVE STRATEGIES FOR A LOW-RETURN WORLD

KNOW YOUR ALTERNATIVES

Today’s miserably low bond yields imply inflation is dead. But some experts see signs that yesterday’s bogeyman is ready to rise again.

Jeremy Siegel of the University of Pennsylvania thinks the rapid growth of cash in chequing accounts and other readily available forms of money, as a result of stimulus payments, will lead to growing inflationary pressure next year, especially as governments pour more money into the economy to address lingering unemployment. “I’m not talking about a return to the 1970s,” he says. “But inflation of 3, 4, 5 per cent a year is likely. We might see that for two to three years.”

Most investors are ill-prepared to deal with any inflationary flicker, Adam Butler of ReSolve Asset Management says. He suggests buying inflation protection in the form of assets such as gold, commodities and real-return bonds, where the payout is tied to the rate of inflation.

For risk-averse investors, strategies such as Harry Browne’s Permanent Portfolio – an equal blend of stocks, bonds, gold and cash – also merit consideration, he says. So do global risk parity strategies that attempt to build portfolios that can weather any economic environment.

THINK GLOBALLY

If there is one truth universally agreed upon in a low-return world, it is that investors must diversify geographically. “Canada accounts for only about 2 per cent of global financial markets,” Adam Butler of ReSolve Asset Management says. “Canadian investors have to be internationally diversified if they want to tap into the range of opportunities out there.”

Diversification means venturing over the border into the United States, but also far beyond. “Most international markets look significantly cheaper than the U.S.,” financial author Larry Swedroe says. Emerging markets, in particular, hold appeal for bargain-hunters, he says.

REMEMBER MARCH

Stocks appear likely to do better than bonds in the years to come. But that doesn’t mean you should necessarily load up on volatile equities.

“You have to know yourself,” says Dan Bortolotti at PWL Capital in Toronto. “If you were quaking in your boots when the market was falling in March, you’re not a good candidate for a riskier portfolio. On the other hand, if you saw the March plunge as a buying opportunity, maybe you can handle a bit more risk.”

Mr. Swedroe agrees. “You should not take on more risk than you can handle,” he says. “Before you raise your exposure to stocks, you should look at all the other levers you have to pull – things like working longer, or saving more.”

DON’T GIVE UP ON VALUE

Value investing was a disaster over the past decade. But Mr. Siegel says investors shouldn’t give up on buying stocks that are trading at low prices compared with fundamentals, such as earnings or cash flow. “There is nearly a record wedge between growth and value stocks in terms of valuation,” he says. “I do believe going forward that a value investor will recover much of what he or she lost in terms of relative performance during the past 10 years.”

WAIT FOR GOOD DOUGH

Older investors shouldn’t limit themselves to stocks and bonds. “If someone is looking for a safe income in retirement and leaving a legacy is not your biggest consideration, then annuities make a lot of sense, " says Bonnie-Jeanne MacDonald of the National Institute on Ageing at Ryerson University.

The best annuity of them all, she says, is the inflation-protected, guaranteed payout that Ottawa provides to retirees in the form of Canada Pension Plan payments. To maximize the value of this payout, you should consider delaying the start of your CPP benefits to age 70, rather than collecting earlier. This results in at least a 42 per cent increase in the real value of what you will collect each month compared with starting CPP at age 65. (Closer to 50 per cent, in all probability, once other adjustments are made.)

This Globe and Mail article was legally licensed by AdvisorStream.

© Copyright 2025 The Globe and Mail Inc. All rights reserved.