PATRICK BRETHOUR

Oct. 30, 2020

Chrystia Freeland sketched out her philosophy as Finance Minister in a speech this week to the Toronto Global Forum, attempting to carve out a middle lane for her and the Liberals in the debate over the direction of federal finances.

Edging away from the left, the Deputy Prime Minister and Finance Minister rejected out of hand the increasingly popular theory that government spending can continue to rise until it generates inflationary pressures.

But Ms. Freeland also rejected the idea of any immediate pullback in federal spending during – or immediately after – the pandemic, resisting the increasing calls for a quick return to the discipline of fiscal anchors for the government.

“This is positioning for her,” said Alexandre Laurin, director of research at the C.D. Howe Institute, noting that Ms. Freeland’s presentation paid tribute to the merits of fiscal responsibility, including a nod to her own family’s roots in northern Alberta.

The speech was conspicuously devoid of hard numbers; those will come in a fiscal update expected next month. However, the Finance Minister did give some hints on how the government will handle the continuing fiscal response to the coronavirus, and the need for economic stimulus once an effective vaccine ends the pandemic.

LOW INTEREST RATES ARE AN OPPORTUNITY TO SPEND

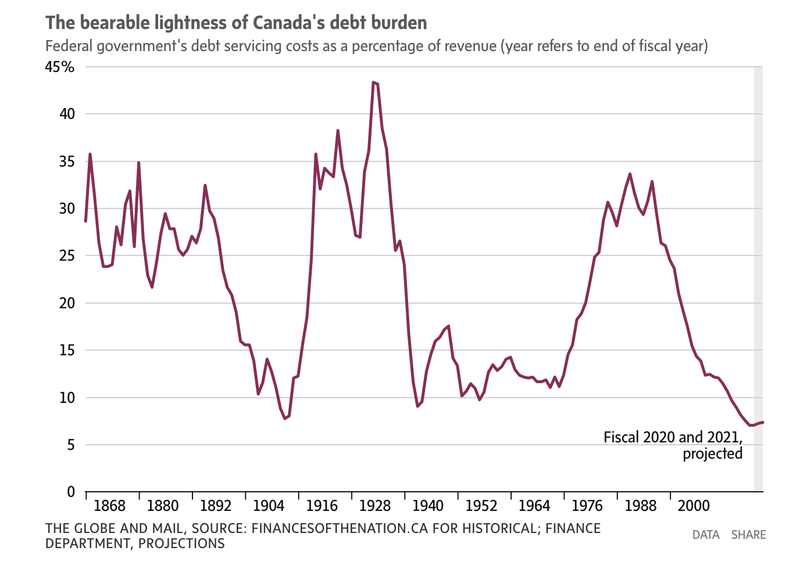

The government has made this point repeatedly, but Ms. Freeland made the case in detail. Falling interest rates (in part a consequence of the Bank of Canada reducing its benchmark rate to effectively zero, as well as intervening in bond markets) have reduced the federal government’s debt servicing costs, even with this year’s record deficit.

As the chart below shows, that assertion is correct. Calculated as a percentage of revenue, debt servicing costs are near historic lows. That ratio is projected to rise slightly from fiscal 2018-19 because of the revenue hit from the coronavirus in the next two years. (Measured in dollars, debt servicing costs are actually down in this fiscal year, an indication of just how low interest rates are.)

But there is an important caveat in measuring debt servicing costs against federal revenues. If revenues are low, the debt burden seems greater. In part, that’s why the debt of the 19th-century seems so great: Taxes, and revenue, were lower in those decades.

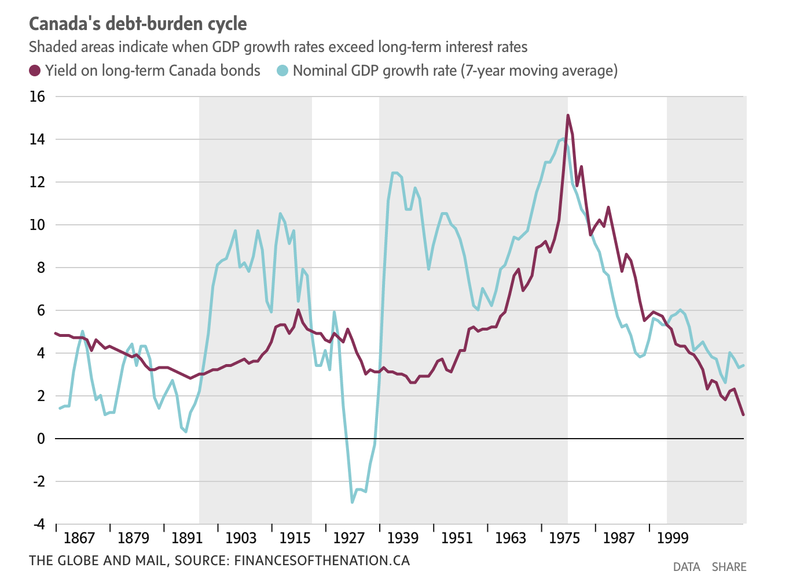

Speaking of history, Ms. Freeland attempted to defuse worries that the Liberals are setting the stage for a return to persistent high deficits and spiraling debt that erode Canada’s credit standing. One of the most significant contributors to that debt spiral was the unrelenting arithmetic of interest rates consistently exceeding economic growth in the 1980s and 1990s. That increased debt servicing costs faster than government revenues, barring significant tax increases, making deficit reduction an uphill battle. Ms. Freeland says those two decades were an anomaly, an exception to most of the past 80 years, in which GDP growth has been higher than interest rates – including today.

On this front, the Finance Minister is on less firm ground. As University of Toronto economist Michael Smart points out, a broader look at Canada’s economic history gives a much different picture. As the chart below shows, interest rates and growth rates have moved through several cycles during Canada’s history. The shaded areas indicate when GDP growth rates are higher than interest rates.

It is indeed true that the 1980s and ’90s look to be an aberration from the past 80 years, but those two decades look less like an exception and more like part of a pattern when the longer-term view is taken.

Université Laval economist Stephen Gordon amplified that point in a Twitter thread, saying governments should not take it for granted that interest rates will remain lower than growth rates, particularly if Canada and other countries lean heavily on that differential to justify big deficits. “Large amounts of borrowing will push interest rates up, everything else being equal,” he wrote.

THIS IS NO TIME FOR AUSTERITY

Faced with concerns over where spending is headed after the pandemic, the Liberals have often responded by rebutting a point no one is making – that spending should be cut now, in the midst of the pandemic. “This is not the time for austerity,” the government said in last month’s Speech from the Throne.

Ms. Freeland continued in that vein in her speech, saying individuals and companies should receive financial support during the coronavirus crisis. “For a government to abandon them at a time like this would be monstrous.”

Any serious economist would agree. So do the Opposition Conservatives, although they have critiqued how the government has rolled out that support.

But the Liberal response sidesteps the critics' point: The lack of clarity over the government’s plans for spending, and for controlling the growth of debt, once the pandemic has ended, hopefully next year.

THIS IS NO TIME FOR A BUDGET

Ms. Freeland said fiscal anchors, which constrain spending, will only be reinstituted once the pandemic has passed. This is in keeping with the Liberals’ wider argument that the current economic situation is so uncertain that it is not possible to issue a credible federal budget.

That contention, however, runs up against the fact that other countries have issued budgets, as have some Canadian provinces. And the Bank of Canada, subject to the same uncertainties, gave its view of long-term trends this week.

“It’s not a question of can or can’t,” observed Trevor Tombe, an associate professor at the University of Calgary, and co-director of FinancesofheNation.ca.

A budget and fiscal anchors would provide a vision of government spending in the medium and long term. But the strictures imposed by fiscal anchors would also force the government to decide, or at least disclose its decisions, about the broad direction of spending and taxation levels once the pandemic eases.

NEXT YEAR IS NO TIME FOR AUSTERITY, EITHER

There will be no rapid reduction in postpandemic federal spending, based on the hints in Ms. Freeland’s speech. She criticized the Conservatives' response to the 2008-09 financial crisis, saying that “premature fiscal tightening” prolonged the economic pain of that recession.

Aggressive spending will be needed, she said, given that the current economic contraction is more severe than in 2008. “It stands to reason we will need to invest more, not less,” she said.

What might the price be? Prof. Tombe noted that federal deficit spending in 2008-09 was 6.6 per cent of GDP when the amount that had to be borrowed for infrastructure spending is included. That is the equivalent today of about $150-billion based on current dollars and the current size of the economy.

However, Prof. Tombe said it’s difficult to assess the eventual size of federal stimulus spending, given the number of variables. And the government itself has yet to make public any numbers.

BUT THERE ARE LIMITS

Federal stimulus spending should be “timely, targeted and temporary.” That was the phrasing of the Conservative government 12 years ago as it announced measures to combat the financial crisis. Interestingly, Ms. Freeland’s language closely tracked that of the Conservatives in 2008-09. Without making any specific commitments, Ms. Freeland said the Liberals’ stimulus spending would be “limited and temporary” – and targeted.

This Globe and Mail article was legally licensed by AdvisorStream.

© Copyright 2024 The Globe and Mail Inc. All rights reserved.