By Laura Saunders

Aug. 25, 2023

For more than five million Americans, even a dollar of extra income can boost annual Medicare premiums by hundreds or thousands of dollars—but refunds of these surcharges are sometimes available.

iStock image

Many Medicare recipients don’t know this, says Drew Tignanelli, a CPA and adviser who has obtained dozens of refunds for clients: “We warn them when they could get hit hard and tell them to call us when they get the letter.”

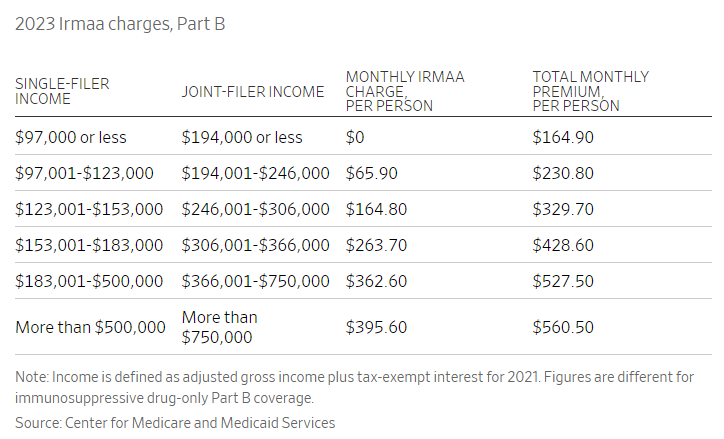

At issue are Medicare premium surcharges for higher earners. While working, employees and their employers together pay 2.9% of wages into the Medicare trust fund, and self-employed taxpayers pay an equivalent tax. There’s a 0.9% surtax for higher earners as well. When people enroll in Medicare, they typically owe premiums for Part B (for doctors) and Part D (for drug coverage). The Part B annual premium, which is about $1,980 for 2023, is typically higher than the Part D premium.

But Congress has also decided that higher-earning seniors should shoulder more of their Medicare costs and imposed surcharges for Parts B and D based on income. These surcharges are known as Irmaa, for Income-Related Monthly Adjustment Amounts. For many taxpayers, they are calculated by the Social Security Administration based on income-tax records and deducted from Social Security payments.

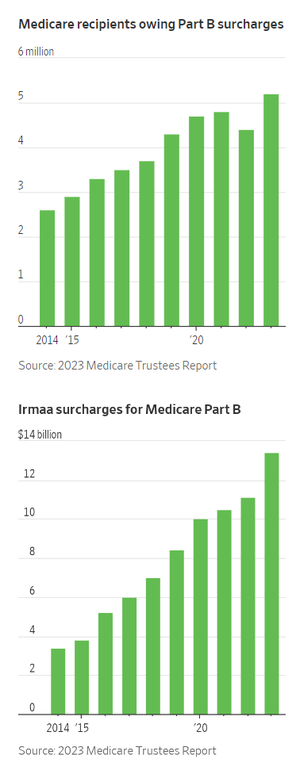

Over the last decade the number of recipients owing Part B Irmaa has doubled, to 5.2 million for 2023, while the amount collected has more than tripled, to $13.4 billion.Irmaa surcharges are unpopular with many who owe them, in part because they’re often deducted from Social Security benefits. The lower monthly payment can come as a shock—especially as the surcharge doesn’t reduce taxable Social Security benefits. Recipients who delay claiming Social Security are billed for premiums.

Another sore point is that Irmaa income brackets are “cliffs.” This means even one extra dollar can bring a much higher premium. For example, a couple who had $246,000 of 2021 income owes total Part B premiums of about $5,540 for 2023. That rises to $7,913 if their 2021 income was $246,001.

What many miss is that Irmaa rules can allow refunds if a Medicare recipient’s current income is lower than it was two years earlier. So recipients with a “work stoppage” like retirement often are eligible for refunds if their income has dropped.

Jeff Davidson, a 67-year-old retired fintech consultant who lives in New York City, qualified for an Irmaa rollback for another reason, a “work reduction.” During the pandemic, he had a 2021 income spike from consulting work and a large one-time IRA withdrawal that raised his 2023 Irmaa payments.

Getting the refund wasn’t easy. Davidson says it took seven months after requesting it in January until approval. He spoke many times with Social Security staffers who were unfailingly polite and tried to help, although the office making the decision moved slowly.

Davidson was meticulous and persistent, however, and now he’s saving about $3,500 in 2023 Irmaa. “It was an opaque process with a lot of frustration, but it worked out,” he says.

In easy-to-prove cases, such as retirement or the death of a spouse, the wait time is typically two to three months, says Heather Schreiber, a consultant specializing in Social Security and Medicare.

Here’s more to know about Irmaa rollbacks.

Plan ahead

Medicare typically takes effect at age 65, so Irmaa is first calculated based on tax-return income when the recipient was 63. Remember this when planning, such as while scheduling periodic Roth IRA conversions that will boost income.

Under current law, tax-free income from Health Savings Accounts or Roth IRA withdrawals won’t raise Irmaa. However, investment income taxed at 0% are included in adjusted gross income and can raise it.

If someone can’t avoid a gain that raises Irmaa for one year and income falls the following year, the surcharge will likely drop as well.

Know the approved reasons for Irmaa refunds

There are seven: death of a spouse; marriage; divorce or annulment; work reduction; work stoppage (such as retirement); loss of income from income-producing property; and loss or reduction of certain pension income.

What’s not a good reason? Among others: boosts to income because of taxable investment gains, Roth IRA conversions, and taxable gains on the sale of a home above the $250,000 or $500,000 exemption or a vacation home.

Ask anyway

Schreiber and others suggest requesting a refund if the issue is in a gray area but seems sympathetic. In one case, a Medicare recipient faced higher Irmaa after selling a second home to pay medical bills for a gravely ill spouse. After seeing the bills, the staffer approved a refund.

Sometimes the result of such a request depends on the person handling it. “It can be the luck of the draw, but always ask,” she adds.

Know the lingo

Technically, a refund request for one of the seven permitted reasons is known as a “new initial determination.” Submit form SSA-44 soon after getting the letter, says Casey Schwarz, an attorney with the Medicare Rights Center.

By contrast, a “reconsideration” is for adjustments that don’t fit into one of the seven categories, says Schreiber. She advises asking a Social Security staffer how to make such a request, and do it soon.

Prepare carefully

Simple cases may only require a phone call. Consider making an appointment for a face-to-face visit to the Social Security office if circumstances are more complex, say because you filed an amended tax return that lowered Irmaa income.

Before the first contact, make sure to gather proof supporting your request, such as a tax return or death certificate. Tignanelli says that when a tax return hasn’t yet been filed, he sometimes makes a projected return and signs it to bolster the request.

Remember that if both spouses are covered by Medicare, then each typically has to file for new determinations or appeals—even if they file a joint tax return.

Be organized and tenacious

Keep good records, including date, name of contact, case reference and issues discussed. If an action is promised by a specified date and doesn’t happen, follow up.

Write to Laura Saunders at Laura.Saunders@wsj.com

Dow Jones & Company, Inc.