By AMY FONTINELLE

Dec. 2, 2022

A health savings account (HSA) is designed to help people with high-deductible insurance plans pay their out-of-pocket medical costs, but it can be surprisingly effective as a retirement savings tool, too.

Here is a look at what these accounts are, who can open one, and how to make the best use of an HSA if you are fortunate enough to have access to one.

iStock image

KEY TAKEAWAYS

- Health savings accounts (HSAs) are available only to those who choose high-deductible health insurance plans (HDHPs).1

- For some, a high-deductible plan works best because the monthly premiums are relatively low.

- The HSA can be used to cover costs that are not covered by the HDHP.1

- The money paid into an HSA is tax-free.1

- If you save some or all of your HSA money each year, you can pile up a significant and tax-exempt addition to your retirement savings.

Why Max Out Your HSA Contributions?

The HSA account has triple tax advantages:1

- The money is not taxed before you pay it in.

- The interest and earnings on the money are not taxed.

- Withdrawals are not taxed if used for allowable medical expenses.

That makes maxing out your HSA an ideal retirement savings strategy.

What Is a Health Savings Account (HSA)?

HSAs are tax-advantaged savings accounts designed to help people who have high-deductible health plans (HDHPs) pay for out-of-pocket medical expenses.1 While these accounts have been available since 2004, many eligible Americans are not taking advantage of them.

According to the Kaiser Family Foundation, these types of high-deductible health plans are made available by about 22% of the employers who offer health benefits. Twenty-one percent of covered workers were enrolled in an HSA-qualified plan in 2021.2 However, only 9% of health savings account owners invest a portion of their funds. The rest, 91%, hold cash.3

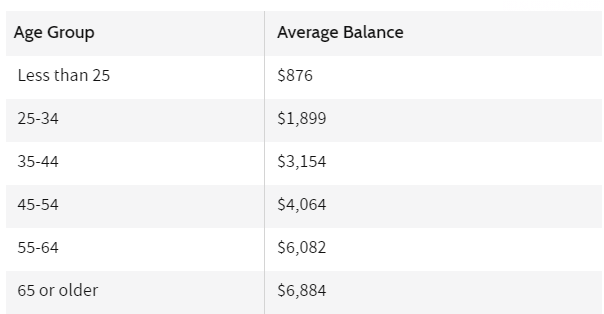

Data reported from the Employee Benefit Research Institute (EBRI) shows that the balance in HSAs varies greatly depending on the age range of the account holders. The following table shows the age group of the account holders and the average balance in their HSAs by the end of year 2020:4

There's good reason to aim for the maximum annual contribution. For the 2022 tax year, that's $3,650 for those with individual health plans and $7,300 for those with family coverage.5 For 2023, the numbers increase to $3,850 for individuals and $7,750 for family coverage.6

This means that consumers who have HSAs but don't contribute the maximum as well as consumers who are eligible for HSAs but haven’t opened one are missing out on an extraordinary option for funding their retirement years.

It’s time to start a new trend.

Why Use an HSA for Retirement?

According to a Wall Street Journal interview with Michael Kitces, the former director of financial planning at Pinnacle Advisory Group Inc. in Columbia, Md, HSAs are "the most tax-preferred account available."7

He also advised, "Using one to save for retirement medical expenses is a better strategy than using retirement accounts" such as a company 401(k) or an Individual Retirement Account (IRA).7

Benefits of an HSA

Your contributions to an HSA can be made via payroll deductions, or from your own funds if you're self-employed. They are tax-deductible, even if you don't itemize your taxes.1 The money paid into an HSA is considered "pre-tax," meaning that it reduces your federal and state income tax liability—and they're not subject to FICA taxes, either.

Your account balance grows tax-free. Any interest, dividends, or capital gains you earn are non-taxable.

TIP: Any contributions your employer makes to your HSA are not included in your taxable income.8

Withdrawals for qualified medical expenses are tax-free. This is a key way in which an HSA is superior to a traditional 401(k) or IRA as a retirement vehicle. Once you begin to withdraw funds from those plans, you pay income tax on that money regardless of how the funds are used.

Unlike a 401(k) or IRA, an HSA does not require the account holder to begin withdrawing funds at a certain age. The account can remain untouched as long as you like, although you are no longer allowed to contribute once you enroll in Medicare.9 You become eligible for Medicare at age 65.10

What's more, the balance can be carried over from year to year; you are not legally obligated to "use it or lose it," as with a flexible spending account (FSA). An HSA can move with you to a new job, too. You own the account, not your employer, which means the account is fully portable and goes when and where you do.1

Who Can Open an HSA?

To qualify for an HSA, you must have a high-deductible health plan and no other health insurance. You must not yet qualify for Medicare, and you cannot be claimed as a dependent on someone else's tax return.1

A primary concern many consumers have about foregoing a preferred provider organization (PPO), health maintenance organization (HMO), or other health insurance in favor of a high-deductible health plan is that they will not be able to afford their medical expenses.

In 2022, the deductible for an HDHP is at least $1,400 for self-only coverage and $2,800 for family coverage. The figures rise in 2023 to $1,500 for individuals and $3,000 for families.1112 Note that this is the minimum. A high-deductible plan may set a larger deductible.

Depending on your coverage, your annual out-of-pocket expenses in 2022 could run as high as $7,050 for individual coverage or $14,100 for family coverage under an HDHP. The maximum increases to $7,500 and $15,000 in 2023.1112

Those high potential expenses are one reason these plans are more popular among affluent families who will benefit from the tax advantages and can afford the risk.

PPO vs. HSA

However, a lower-deductible plan such as a preferred provider organization (PPO) could also have high costs because you’re paying the extra money regardless of your actual medical expenses that year. With an HDHP, you're spending more closely matches your actual healthcare costs.

Of course, if you know your healthcare costs for the year are likely to be high—a woman who is pregnant, for instance, or anyone with a chronic medical condition—a health plan with a high deductible may not be the best choice. But keep in mind that HDHPs completely cover some preventive care services before you meet your deductible.

All in all, an HDHP might be more budget-friendly than you think—especially when you consider its advantages for retirement. Let’s take a look at how you could be using the features of an HSA to help fund your retirement.

Max Out Contributions by Age 65

As mentioned above, your HSA contributions are tax-deductible until you sign up for Medicare. The 2023 contribution limits are $3,850 for individuals and $7,750 for family coverage, including employer contributions. The contribution limits are adjusted annually for inflation.6

$7,300

The contribution limit for a family HSA in 2022. The contribution limit for an individual is $3,650.13

If you have an HSA and you're 55 or older, you can make an extra "catch-up" contribution of $1,000 per year and a spouse who is 55 or older can do the same if each of you has your own HSA account.1

You can contribute up to the maximum regardless of your income, and your entire contribution is tax-deductible. You can even contribute in years when you have no income. You can also contribute if you're self-employed.

"Maxing out contributions before age 65 allows you to save for general retirement expenses beyond medical expenses," says Mark Hebner, founder and president of Index Fund Advisors Inc. in Irvine, Calif., and author of "Index Funds: The 12-Step Recovery Program for Active Investors." Although you will not receive the tax exemption," Hebner adds, "it gives retirees more access to more resources to fund general living expenses."

Don't Spend Your Contributions

This may sound counterintuitive, but we're looking at an HSA primarily as an investment tool. Granted, the basic idea behind an HSA is to give people with a high-deductible health plan a tax break to make their out-of-pocket medical expenses more manageable.

But that triple tax advantage means that the best way to use an HSA is to treat it as an investment tool that will improve your financial picture in retirement. And the best way to do that is to spend little or none of your HSA contributions during your working years and pay cash out of pocket for your medical bills.

In other words, think of your HSA contributions the same way you think of your contributions to any other retirement account: untouchable until you retire. Remember, the IRS does not require you to take distributions from your HSA in any year, before or during retirement.

If you absolutely must spend some of your contributions before retirement, be sure to spend them on qualified medical expenses. These distributions are not taxable. If you are forced to spend the money on anything else before you’re 65, you will pay a 20% penalty as well as the income tax on the withdrawals.1

Invest Your Contributions Wisely

The key to maximizing your unspent contributions, of course, is to invest them wisely. Your investment strategy should be similar to the one you’re using for your other retirement assets, such as a 401(k) plan or an IRA. When deciding how to invest your HSA assets, make sure to consider your portfolio as a whole so your overall diversification strategy and risk profile are where you want them to be.

Your employer might make it easy for you to open an HSA with a particular administrator, but the choice of where to put your money is yours. An HSA is not as restrictive as a 401(k); it’s more like an IRA.

Since some administrators only let you put your money in a savings account, where you’ll barely earn any interest, make sure to shop around for a plan with high-quality, low-cost investment options, such as Vanguard or Fidelity funds.

How Much Could You Receive?

Let's do some simple math to see how handsomely this HSA savings and investment strategy can pay off.

We’ll use something close to a best-case scenario and say that you’re currently 21, you make the maximum allowable contribution every year to a self-only plan, and you contribute every year until you’re 65. We’ll assume that you invest all your contributions, automatically reinvest all your returns in the stock market earning an average annual return of 8% and that your plan has no fees. By retirement, your HSA would have more than $1.2 million.

What about a more conservative estimate? Suppose you’re now 40 years old and you only put in $100 per month until you’re 65. You keep your investment choices conservative and earn an average annual return of 3%. You’d still end up with nearly $45,000 by retirement.

Try out an online HSA calculator to play with the numbers for your own situation.

Maximize Your HSA Assets

Here are some options for using your accumulated HSA contributions and investment returns in retirement. Remember, distributions for qualified medical expenses are not taxable, so you want to use the money exclusively for those expenses as much as possible. There are no required minimum distributions, so you can keep the money invested until you need it.1

If you must use withdrawals for another purpose, the money will be taxable. However, after age 65, you won’t owe the 20% penalty.1 Using HSA assets for purposes other than qualified medical expenses is generally less detrimental to your finances once you’ve reached retirement age because you may be in a lower tax bracket if you’ve stopped working, reduced your hours, or changed jobs.

Timing Is Everything

By waiting as long as possible to spend your HSA assets, you maximize your potential investment returns and give yourself as much money as possible to work with. You’ll also want to consider market fluctuations when taking distributions, the same way you would when taking distributions from an investment account. You obviously want to avoid selling investments at a loss to pay for medical expenses.

Choose a Beneficiary

When you open your HSA, you will be asked to designate a beneficiary to whom any funds still in the account should go upon your death.

If you're married, the best person to choose is your spouse because they can inherit the balance tax-free. (As with any investment with a beneficiary, however, you should revisit your designations from time to time because death, divorce, or other life changes may alter your choices.)

Anyone else you leave your HSA to will be subject to tax on the plan’s fair market value when they inherit it.14

Your plan administrator will have a designation-of-beneficiary form you can fill out to formalize your choice.

Pay Health Expenses in Retirement

Fidelity Investments’ most recent Retirement Health Care Cost survey calculates that the cost of healthcare throughout retirement for a couple who both turn 65 in 2022 is $315,000, up from $300,000 in 2021.1516

The money saved in an HSA can help with such skyrocketing costs.

Qualified payments for which tax-free HSA withdrawals can be made include:17

- Office-visit copayments

- Health insurance deductibles

- Dental expenses

- Vision care (eye exams and eyeglasses)

- Prescription drugs and insulin

- Medicare premiums

- A portion of the premiums for a tax-qualified long-term care insurance policy

- Hearing aids

- Hospital and physical therapy bills

- Wheelchairs and walkers

- X-rays

You can also use your HSA balance to pay for in-home nursing care, retirement community fees for lifetime care, long-term care services, nursing home fees, and meals and lodging that are necessary while obtaining medical care away from home. You can even use your HSA for modifications, such as ramps, grab bars, and handrails, that make your home easier to use as you age.17

One strategy might be to bunch qualified medical costs into a single year and tap the HSA for tax-free funds to pay them, compared with withdrawing from other retirement accounts that would trigger taxable income.

“Using HSA money to pay for medical expenses and long-term care insurance in retirement is a great benefit for investors given the tax exemption on any withdrawals made to fund either," says Hebner. "In other words, it’s the most cost-effective way to fund those expenses because they provide investors the highest after-tax value."

Also, note that there are limitations on how much you can pay tax-free for long-term care insurance based on your age.

Reimburse Yourself for Expenses

With an HSA you are not required to take a distribution to reimburse yourself in the same year you incur a particular medical expense. The key limitation is that you can’t use an HSA balance to reimburse yourself for medical expenses you incurred before you established the account.

So keep your receipts for all healthcare expenses you pay out of pocket after you establish your HSA. If in your later years, you find yourself with more money in your HSA than you know what to do with, you can use your HSA balance to reimburse yourself for those earlier expenses.1

Warnings About HSA Retirement Use

The strategies described in this article are based on federal tax law. Most states follow federal tax law when it comes to HSAs, but not all do. Even if you live in a state that taxes HSAs, you’ll still get federal tax benefits.

The taxation of these plans could change in the future at either the state or federal levels. The plans could even be eliminated altogether, but if that happens, we would likely see the existing account holders exempted, as was the case with Archer MSAs.

How Can I Qualify to Open a Health Savings Account (HSA)?

The HSA is available only to people who choose a high-deductible health insurance plan. Granted, a high-deductible plan is not for everyone. The monthly premiums are lower but the potential costs are higher.

High-deductible plans best suit people who are currently healthy, have no ongoing medical issues that require regular treatment, and dislike paying more monthly than they have to in premiums. It helps if they also have enough savings to bear the costs of an unexpected medical crisis.

In any case, that's what the HSA is intended to do: it helps cover costs that aren't covered by the insurance.1

What Can I Use My HSA for After Retiring?

Once you're 65, you can use the money for any purpose. If the purpose is a qualified medical expense, the withdrawal is tax-free. If it's for any other purpose, the withdrawal is taxable as income. You won't, however, be subject to the 20% penalty for non-medical use of the funds. That is imposed only on people under age 65.1

Can I Use My HSA Account to Pay My Insurance Premium?

No. The monthly insurance premium does not qualify as an eligible medical expense. You can, however, use it to reimburse yourself for deductibles and copays.18

The Bottom Line

A health savings account, available to consumers who choose a high-deductible health plan, has been largely overlooked as an investment tool, but with its triple tax advantage, it provides an excellent way to save, invest, and take distributions without paying taxes.

The next time you’re choosing a health insurance plan, take a closer look at whether a high-deductible health plan might work for you. If so, open an HSA and start contributing as soon as you’re eligible.

By maximizing your contributions, investing them, and leaving the balance untouched until retirement, you’ll generate a significant addition to your other retirement options.

Of course, you can't let the savings tail wag the medical dog. Hoarding your HSA monies rather than attending to your health is not recommended. However, if you’re financially able to use post-tax dollars for your current healthcare costs while saving your pre-tax HSA dollars for later, you could build a nice nest egg to use in retirement.

Article Sources:

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

- Internal Revenue Service. "Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans."

- Kaiser Family Foundation. "2021 Employer Health Benefits Survey."

- Employee Benefit Research Institute. "Trends in Health Savings Account Balances, Contributions, Distributions, and Investments and the Impact of COVID-19," Page 15.

- EBRI. "Trends in HSA Balances, Contributions, Distributions, and Investments, 2011-2020."

- Internal Revenue Service. "Rev. Proc. 2021-25," Page 1.

- Internal Revenue Service. "Rev. Proc. 2022-24," Page 1.

- The Wall Street Journal. "HSAs Offer Tax Benefits Beyond 401(k)s."

- Internal Revenue Service. "Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans," Page 3.

- Wellesley College. "Changes to your HSA When You Reach 65," Page 1.

- Social Security Administration. "Medicare Benefits."

- Internal Revenue Service. "Rev. Proc. 2021-25," Page 2.

- Internal Revenue Service. "Rev. Proc. 2022-24," Page 2.

- Internal Revenue Service. "Rev. Proc. 2022-24."

- Internal Revenue Service. "Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans," Page 10.

- Fidelity Investments. "Fidelity’s 20th Annual Retiree Health Care Cost Estimate Hits New High: A Couple Retiring Today Will Need $300,000 to Cover Medical Expenses, an 88% Increase Since 2002," Page 1.

- Fidelity. "How to Plan for Rising Health Care Costs."

- Internal Revenue Service. "Publication 502, Medical and Dental Insurance."

- U.S. Centers for Medicare & Medicaid Services. "Health Savings Account (HSA)."