By Trina Paul

Oct. 23, 2023

For the past year, you’ve probably heard that a recession is on the horizon. Though economists have been predicting a downturn for months, a recession seems nowhere in sight: the labor market is strong, the stock market is thriving, and inflation has cooled since last year. So, where is the recession, and why do people still think it will happen?

To predict a recession, economists look at certain indicators with a solid track record of signaling a downturn. One of those indicators is the yield curve. And right now, the yield curve is flashing red.

iStock-497754124

What is the yield curve?

The yield curve is a line that plots yields, or interest rates, of bonds with different maturities and equal credit quality. Though yield curves can be plotted with bonds of any maturity, some of the most common yield curves used are the spreads between either the three-month treasury bill or two-year and ten-year Treasury notes, which are used to indicate the spread between short-term and long-term Treasury securities.

Generally, a yield curve is upward-sloping, with short-term bonds offering lower yields and long-term bonds providing higher yields. In other words, you should be compensated with a higher yield when you tie up your money for longer periods.

Sometimes a yield curve can invert and start sloping downward. When this happens, short-term bonds have higher yields than long-term bonds, and investors are not rewarded for parting with their money for longer periods.

Why is the yield curve used to predict recessions?

When the yield curve inverts, investors expect the Fed to reduce its benchmark rate—the federal funds rate—in the future, which drives down yields for longer-term bonds.

According to Jeanette Garretty, chief economist and managing director at Robertson Stephens, a wealth-management company based in California, an inverted yield curve is used to predict recessions because it indicates what investors think the Fed will do with its benchmark rate in the future.

“What tends to happen before recessions is the Fed is raising interest rates, [or] setting that policy rate at the short end, and you have market participants getting more pessimistic, and they're betting that interest rates are going to fall in the future,” says Andrew Patterson, senior international economist at Vanguard. “So you have a situation where you could have the short end of the yield curve having higher yields than longer-dated maturities.”

If the economy is currently experiencing high inflation and low unemployment rates, the Fed will raise interest rates to reduce demand and tamp down on inflation. Once rate hikes affect the economy—by cooling inflation and causing unemployment to rise—the Fed may need to cut rates to encourage consumers and businesses to spend again.

So how long does it take after the yield curve inverts for a recession to occur? Both Garretty and Patterson estimate that it takes around six to 12 months before a downturn happens.

Even though economists frequently rely on the yield curve to predict recessions, it’s not always a fool-proof indicator.

“Every recession that we've seen has been preceded by an inverted yield curve,” says Garretty. “That’s not to say that every inverted yield curve has pointed to a recession.”

The yield curve has only had one false positive since 1955: In 1966, there was an inversion of the yield curve that was not followed by a recession, according to a 2018 San Francisco Federal Reserve Bank report from 2018.

What is the yield curve telling us right now?

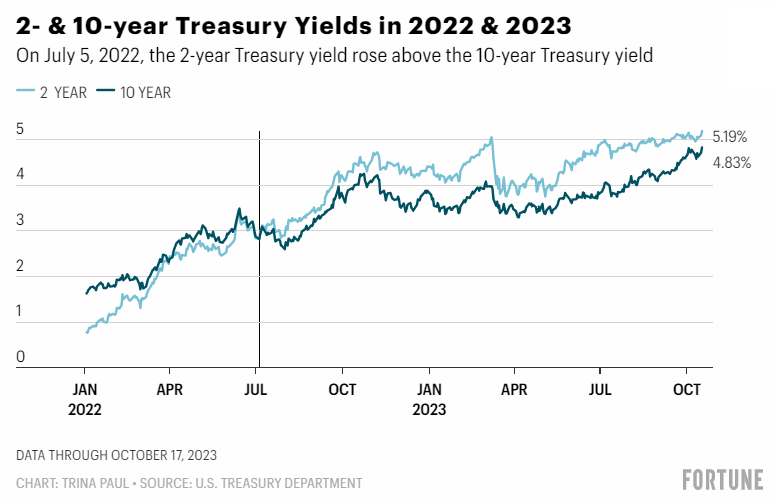

On July 5, 2022, the yield curve between the two-year and ten-year Treasury notes inverted, and it’s stayed that way since then. It’s been more than one year since the yield curve inverted, and the economy is still humming along—unemployment is at 3.8%, inflation has cooled to 3.7% year-over-year, and consumers are still spending.

“The U.S. is not in a recession,” says Garretty. “The labor market is generating a lot of income for people—they are getting real gains in their wages…Nobody's happy with these price increases, but they have the income that allows them to manage it.”

Though it seems like the economy and consumers have yet to feel the impact of the Fed’s rate hikes—which have risen from near-zero to more than 5% in the past 18 months—Patterson doesn’t rule out the possibility of a recession occurring just yet.

“Even though a yield curve of this duration has typically resulted in a recession in the past, there's good reason to believe a recession has been delayed for reasons like the housing market remaining resilient and the strength of the labor market,” says Patterson. “Recession remains our base case. Sometime in 2024.”

Only time will tell whether the recent yield curve inversion accurately predicts a recession.

“If forecasting recessions was as easy as looking at the yield curve…you would see a lot more economists saying things like on November 16 at two o'clock, there will be a recession—it’s clearly not that easy,” says Garretty.

Recession-proofing your finances

Though it’s uncertain whether a recession is on the horizon, there are a few ways to prepare, like analyzing your spending, paying off debt, investing, and building up your emergency fund.

Prioritize paying off your credit card debt

With interest rates at their highest level in more than 20 years, it’s become very expensive to hold credit card debt: The average credit card annual percentage rate (APR) clocks in at more than 20%.

Paying off your credit card debt can involve taking a closer look at your spending—are there any discretionary expenses you could cut? Or do you need to boost your income by starting a side hustle or aiming for a promotion at work?

If you have debt on multiple cards, you could also employ one of the popular debt payoff strategies—the avalanche or snowball methods.

With the snowball method, you pay the smallest balance off first before moving to the larger ones, which allows you to score a quick win. If you want to focus on saving more money, you can use the avalanche method, where you prioritize paying off your highest interest rate debt before moving to the lower rate debt.

Build up your emergency fund

Of course, when recessions occur, unemployment typically rises, too. To be prepared for a layoff, experts typically suggest having three to six months' worth of living expenses stashed in your emergency fund. Saving can be as easy as automating monthly payments from your checking account to a high-yield savings account. Hint: You can earn more than 5% on a high-yield savings account right now.

Invest in recession-proof assets

During an economic downturn, the value of stocks typically slides as consumers and businesses spend less. However, there are some assets that are less susceptible to volatility during a recession.

Stuart Katz, chief investment officer at Robertson Stephens Wealth Management, recommends investing in companies that provide consistent dividends during a recession or periods of high inflation, as these companies typically have more resilient business models.

Another option is defensive stocks which are from sectors like healthcare or utilities. These stocks are considered less sensitive to changes in the economy because consumers still need to pay electricity and medical bills regardless of how the economy is performing.

And lastly, rather than investing in individual stocks, consider putting your money to work in a low-fee exchange traded fund (ETF) or mutual fund that’s dividend-generating and invested in defensive stocks. ETFs and mutual funds enable you to invest in many companies simultaneously, providing you with instant diversification.

The takeaway

The current inverted yield curve tells us what investors think will happen to the economy in the future: The Fed will need to cut interest rates because of a recession. However, when the yield curve inverts, it’s not always an indicator of an economic downturn—even if it has been in the past.

Regardless of whether a recession occurs, it never hurts to be ready for one, whether it’s by adding to your emergency fund or paying off high-interest rate debt.

c.2025 Fortune Magazine. Distributed by The New York Times Licensing Group.

This Fortune article was legally licensed by AdvisorStream.