By JIM PROBASCO

Jan. 5, 2021

President Trump recently signed the Consolidated Appropriations Act, 2021 into law.

iStock-1218894362.jpg

KEY TAKEAWAYS

- A third round of Paycheck Protection Program (PPP) loans was authorized by the passage of H.R. 133: Consolidated Appropriations Act, 2021 into law Dec. 27, 2020.

- First-time PPP loans are available for the lesser of $10 million or 2.5 times your average monthly payroll.

- Second-draw loans up to $2 million are available for businesses that have used funds in their Round 1 or Round 2 loan.

- 100% of your loan could be forgiven if you follow guidelines.

- Passage of the PPP Flexibility Act of 2020 relaxes many PPP loan guidelines.

- You can apply for both a PPP and EIDL loan.

- Check eligibility before you apply.

- You can apply through any SBA approved 7(a) lender.

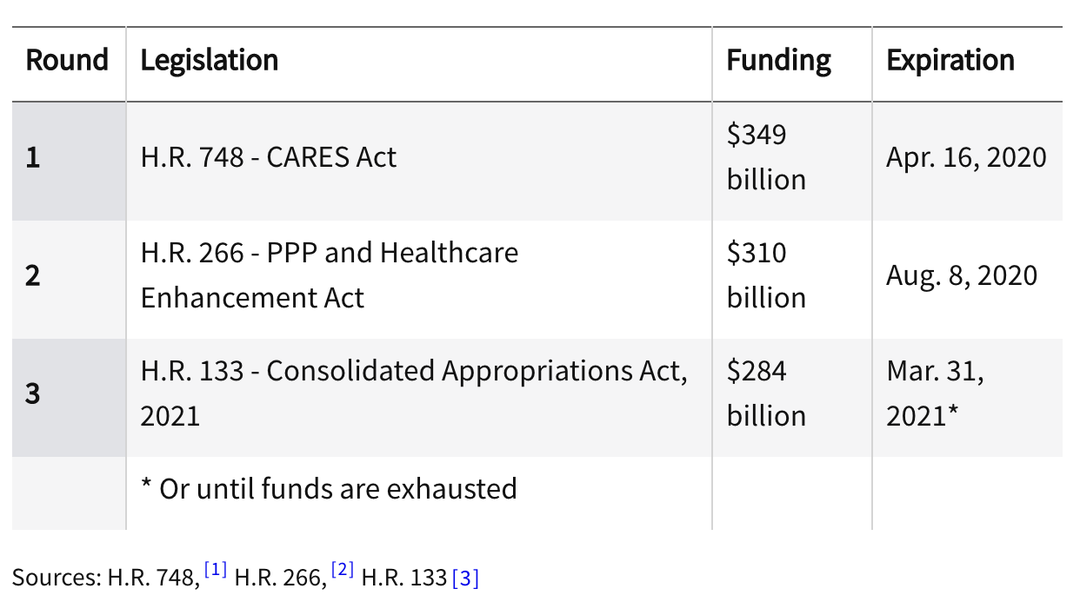

This act includes new funding for the Paycheck Protection Program (PPP) which expired Aug. 8, 2020. The PPP was created by the CARES Act and originally included $349 billion in funding. That money was gone within two weeks resulting in a second round of funding totaling $320 billion. Round 2 loans ended Aug. 8, 2020 and there has been no additional funding until now.

Round 3 funding, $284 billion, expands on the original PPP goals of providing loans to businesses for payroll and other costs to help those businesses remain viable and allow their workers to pay their bills. The table below outlines all three rounds of PPP loan funding to date.

Although official guidance on Round 3 PPP funding has not yet been issued by the Small Business Administration (SBA), it is expected within a matter of days and required by Jan. 6, 2021.3 Meanwhile, H.R. 133, H.R. 266, and H.R. 748 (CARES Act) provide information about how the rounds differ and how they are the same.

PPP Round 3 Eligibility

New PPP funding allows you to apply for a loan whether you received an initial PPP loan or not. The eligibility rules for each category of borrower are somewhat different.

First-Time Borrower

If you were not able to receive a PPP loan in Round 1 or Round 2 funding, you can apply for Round 3 funding of up to $10 million as a new applicant. The program rules for you will be essentially the same as for the first round to include:

- Any business categorized under "Accommodation or Food Services," such as restaurants and hotels that have 500 or fewer employees per location

- Tribal businesses

- Independently owned franchises

- Self-employed workers, independent contractors, gig workers, and sole proprietors.2 1

Additional changes for first-time borrowers under Round 3 address concerns about small businesses that were unable to obtain a PPP loan in Round 1 or Round 2. Round 3 specifically sets aside $35 billion for first-time borrowers with 500 or fewer employees and $15 billion for first-time loans to businesses with 10 or fewer employees, as well as businesses in distressed areas.

Round 3 also provides that debtors in bankruptcy are now eligible for PPP loans and the loans will be treated as administrative expenses.1

Second Time Borrower

If you received PPP funding in Round 1 or Round 2, you may be eligible for Round 3 funding in what's known as a second draw, as long as you've used all of your Round 1 or Round 2 funds (or will use them).

Second-draw loans cannot exceed $2,000,000 and only go to small businesses with 300 or fewer employees. You must also demonstrate that you experienced a loss of at least 25% of gross receipts in any quarter during 2020 compared to the same quarter in 2019.

As with first-time borrowers, Round 3 also sets aside funds ($25 billion) for second-draw loans for small businesses with 10 or fewer employees or that are located in distressed areas.3

Second-Time Borrower Exclusions

Round 3 guidelines for second-draw loans exclude you from a second-draw loan if your company:

- Is ineligible under existing SBA regulations;

- Is primarily engaged in lobbying or other political activities;

- Is owned by an entity created in or with significant operations in the People's Republic of China or the Special Administrative Region of Hong Kong;

- Includes a board member who is a resident of the People's Republic of China;

- Is a recipient of a shuttered venue operator grant under Section 24 of the Act.3

You should also be aware that while it is not yet clear whether a second-draw loan removes or changes the necessity certification requirement of previous PPP loans. To be safe, you should include a statement that current economic uncertainty makes the loan request necessary on your PPP loan application once it becomes available.

Where to Apply for a Round 3 PPP Loan

Although specifics are not yet available, it is anticipated that the application process will be similar to that for Round 1 and Round 2 PPP loans.

Round 1 and Round 2 loans were administered by approved SBA lenders and were actually a new form of the existing SBA 7(a) loan program. You could apply for your PPP loan through any of the 1,800 participating SBA approved 7(a) lenders or through any participating federally insured depository institution, federally insured credit union, and Farm Credit System institution.

Other lenders were available to make PPP loans once they were approved and enrolled in the program. You started by consulting with your local lender as to whether it was participating. If you had trouble locating a lender, you could use the SBA Paycheck Protection Program lender search tool.

Until guidelines and application instructions are forthcoming, check with your local lender and monitor the Small Business Administration PPP program website for updates.4

There will be scammers. Just as with the first two rounds, if you are a small business owner you can anticipate hearing from scammers promising to help you obtain a PPP loan. Only go through approved lenders or the SBA.

Round 3 PPP Application Deadline

The Consolidated Appropriations Act, 2021 extends the Paycheck Protection Program (PPP) through March 31, 2021, or until funds are depleted. The amount of funds currently available is $284 billion. Maximum loans of $10 million will be available to first-time borrowers and loans up to $2 million may be offered to second draw, small business owners.3

How to Apply for a Round 3 PPP Loan

Pending guidelines from the SBA, it is likely future loans will follow a pattern similar to that followed with previous PPP loans. You will likely start by downloading and filling out a loan application from the SBA website. The application should be self-explanatory and lay out the documentation you will need.4

Choose Your Own Covered Period

Round 1 and Round 2 PPP loans stipulated that the time during which you had to use your loan proceeds (covered period) would be an eight-week period beginning on the date you received your loan proceeds. That was later expanded to 24 weeks.

Round 3 allows you to choose any length period between 8 weeks and 24 weeks, giving you more control over how to handle reductions in your workforce, if needed, once PPP funds are depleted.3

Use of Round 3 PPP Funds

The Consolidated Appropriations Act, 2021 expands the types of expenses for which you can use Round 3 PPP funds. This also applies to existing PPP loan funds (unless you have already obtained forgiveness). In addition to payroll, rent, covered mortgage interest, and utilities, the Paycheck Protection Program will now let you use loan proceeds for:3

- Certain operations expenses including business software, business-related cloud computing services, product or service delivery, payroll processing, payment, and tracking costs, HR and billing functions, tracking of supplies, inventory, records, and expenses

- Covered property damage costs including costs related to damage or vandalism caused by looting or public disturbances in 2020 that were not covered by insurance or other compensation

- Listed supplier costs including payments to a supplier of goods that are essential to operations and made pursuant to a contract or order in effect at any time before the covered period or, with respect to perishable goods, in effect at any time during the covered period

- Covered worker protection expenses including operating or capital expenditures required to comply with requirements or guidance issued by the CDC, HHS, OSHA, or any state or local government during the period beginning March 1, 2020, and ending on the date when the national emergency expires

Tax Treatment of Round 3 PPP Loans

Round 3 PPP loans will not be included in your company's taxable income. If your loan is forgiven, expenses paid with the proceeds of your loan will be tax-deductible. Further, this rule applies to new, existing, and previous PPP loans. In addition, any income tax basis increase that results from your PPP loan will remain even if the PPP loan is eventually forgiven.3

Disclaimer: This preliminary information regarding PPP funding in the Consolidated Appropriations Act, 2021, is based on legislation that is subject to further guidance and updating by the Small Business Administration.

Article Sources:

- U.S. Congress. "H.R. 748." Accessed Jan. 3, 2021.

- U.S. Congress. "H.R.266 - Paycheck Protection Program and Health Care Enhancement Act." Accessed Jan. 3, 2021.

- U.S. Congress. "H.R.133 - Consolidated Appropriations Act, 2021." Accessed Jan. 3, 2021.

- Small Business Administration. "PPP Loan Details." Accessed Jan. 3, 2021.