Michelle Singletary

March 28, 2019

For many households, their tax refund is the largest infusion of cash during the year aside from their regular paychecks.

So what to do with what many consider their yearly bonus?

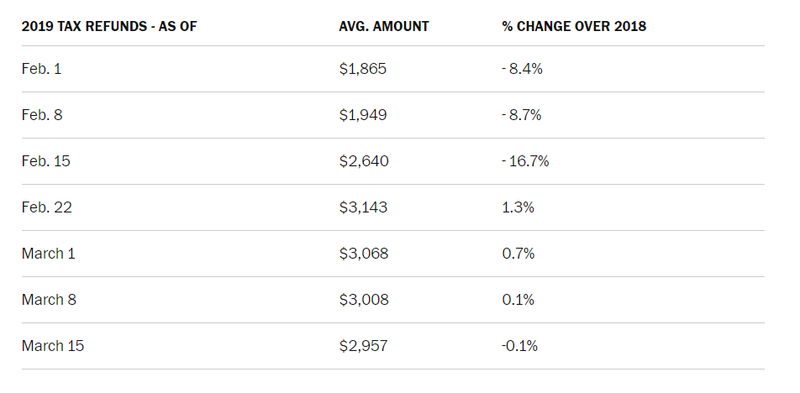

I must, before I give my suggestions on what you might do with your refund, remind those who may not know why it's not wise to wait for this "windfall." As of March 15, the average refund was $2,957.

When you repeatedly get a refund on purpose you are giving Uncle Sam an interest-free loan. If you're carrying debt you are losing money with this strategy. In this case, it's better if you adjust your paycheck withholdings to receive your money throughout the year.

Source: IRS, 2019 Filing Season Statistics

A lot of serial refund recipients view their refund as a forced savings plan. If that's you and you have no plans on giving up on getting a large refund, at least make sure the money is well used. Here's what you should and shouldn't do with the money.

— Establish an emergency fund . I know you may be tired of this tried and true advice but it's so vital to creating financial stability. The Federal Reserve in a report last year found that many households don't have enough saved to cover a $400 financial emergency.

"Four in 10 adults, if faced with an unexpected expense of $400, would either not be able to cover it or would cover it by selling something or borrowing money," the report said.

When you can't meet a sudden expense, the options to finding money can be less than optimal, such as a payday loan or getting further into credit-card debt.

— Boost your rainy-day fund . Let's say you have an emergency fund but it's pretty pitiful. You may not be able to save enough for the recommended three to six months of living expenses, but at least set a goal to have one month's worth of the money it takes to run your household.

— Set aside money for a 'life happens' fund . This savings pot is different from your emergency fund, which you want to remain untouched until you have a serious financial crisis, such as a job loss. The life happens savings is for the things in life that happen, such as a car repair. Let's say you don't have any savings but got back this year $2,000. Put a $1,000 toward the one month of living expenses in the emergency fund. Take the remaining $1,000 and put it in the life happens fund. As you draw down on the latter savings, you put back money when you can to maintain a certain level to handle unplanned expenses.

— Pay down your consumer debt. You may be thinking your $2,900 tax refund won't make a large enough dent in your $10,000 of credit-card debt so why bother. But it does make a difference. Or maybe you can use the money to reduce the principal on one of your student loans. The point is to get started on an aggressive plan to get rid of your debt.

Here's what you shouldn't do with your refund.

— Don't treat yourself if you don't have emergency and life happens funds. Yes, you work hard and you deserve some self-care. But fun should come after being sure you have enough funds to at least cover a $400 emergency.

— Don't buy a new or used car. You might see ads from auto dealers encouraging you to use your refund as a down payment on a new car. Stop. Can you really afford to add another debt to your budget? It might be better to use your refund to repair your current vehicle. Or maybe use some of the money to get your car detailed so it feels new to you.

— Don't lend money you need back . Tis the season for refunds and that can lead to hands out for help. Avoid personal loans to friends and family. Instead, if you can afford it, make it a gift not a loan. And certainly don't give money to someone who has shown a pattern of financial irresponsibility.

Here's what some readers have done with their refunds this year.

— "We put our refund toward our property tax and built up an emergency fund. You need to replace appliances so it is important to have the money on hand."

— We put $1,000 in the grandkids college fund and $1,000 toward annual homeowners association dues," wrote Kevin Harris from Staunton, Va .

— "What I intend to do with this year's tax refund is (mostly) pay off this year's extra dental bills."

— "I will be spending much of my tax refund this year as I have spent it nearly every year since becoming a homeowner: Making improvements on my home," wrote Linda Goodrich from Roanoke, Va .

— "Every year we use our tax refund to pay our property taxes. This year we need new tires for our car. It's nice not to have to worry about big-ticket items."

— "My husband and I will upgrade the back entrance to our house with a safer one — a platform and steps," wrote Nancy Randall from Adelphi, MD . "Also, we will take a five-day trip to Maine this summer. Our savings are in good shape."

— "One of the smartest things I did many years ago was put my refund into an emergency savings account," wrote Michael Rief of Ohio . "An emergency fund darn near takes all the stress out of life. I never had to worry when things broke down or my work hours were interrupted for whatever reason. I know some folks frown on my plan but . . . The withholding forces me to tighten my budget because I know if I get my hands on it, I'm gonna spend it on something stupid."

— "This April I'm going to flip my refund back to the IRS to pay first and second quarter estimated taxes. Then if I make more, I can always send in more. But there is nothing sweeter, at least in my book, than knowing I'm ahead rather than behind."

— "We spent our MUCH smaller refund this year on a week-long getaway to Canada so that we could escape the in-your-face 24-hour news cycle of the ever-present presence of our mean and nasty president."

Last week I asked: Have you fallen prey to a tax debt settlement company?

"I was sold a bill of goods by a Florida tax firm who did file back returns for me," wrote Jaes from California . "They said everything would cost $4,000. I paid. Over time there were 'delays' and 'difficulties' reaching the 'agent' in charge of my case. They managed to get me to pay them another $10,000 over a couple of years without any results or tax reductions, even though I had health problems at the time. Yes, I was incredibly stupid to let them bill me this way. They refused to spend any more time on my case unless I sent them another $2,000. I told them there would be no more money until there were some positive results forthcoming. I was shuffled around to several employees who 'handled' my case over the time. I chalked it up to me being honest but gullible."

Follow Michelle Singletary on Twitter @SingletaryM and Facebook.

This article was written by Michelle Singletary from The Washington Post and was legally licensed by AdvisorStream through the NewsCred publisher network.