By Ronda Lee

Sept. 2, 2021

Flood insurance is not required for homeowners unless they live in a high-risk flood zone. However, the majority of homeowners who experienced flooding in 2020 did not live in flood zones and were not covered under their homeowners insurance. According to FEMA, 30% of all flood damage claims happens in low to moderate-risk zones, where flood insurance is not required.

iStock-451680177.jpg

- Flood insurance is not included in standard homeowners insurance policies.

- You're only legally required to have flood insurance in a high-risk flood zone, but the majority of flooding in 2020 happened outside of flood zones.

- One inch of flood damage alone can cost a household up to $20,000.

"Flooding is one of the most common and costly natural disasters in the US, and given we are in the midst of an above-average hurricane season, consumers need to ensure that they will not be left exposed if their homes are hit hard by a storm," said Ralph Blust, CEO of the National Flood Services. NFS administers flood insurance on behalf of FEMA and the National Flood Insurance Program (NFIP).

Blust told Insider many homeowners believe they are prepared for a flood, but the reality is that only 12% actually have flood coverage. He said homeowners need to understand how, or if, flood damage is covered under their current insurance policies, especially if they are in a hurricane area.

What is flood insurance?

Flood insurance is an addition to your homeowners insurance policy that can cover flood-related damage. A flood is defined as surface water entering the inside of your home structure through existing openings that are above ground level.

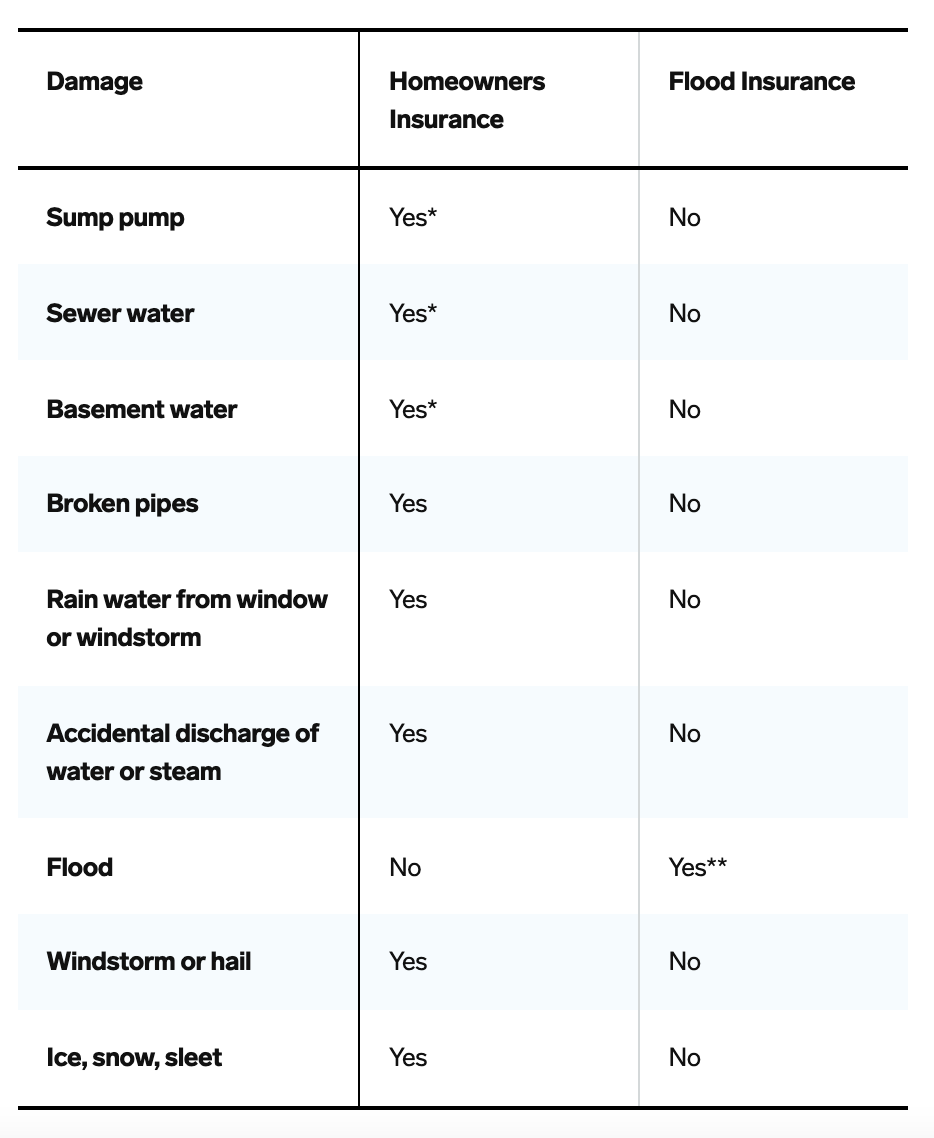

Blust noted that flood insurance specifically excludes water damage from sump pumps, sewer water, broken pipes, rain from an open window, and rain from windstorms.

Quick tip: Only about 14% of US homes are in areas that require flood insurance, but it could be still be worth it if you live outside a high-risk area. A standard homeowners policy will not provide any coverage for flood damage.

How is flood insurance different from homeowners insurance?

Homeowners insurance offers protection for the dwelling, personal belongings, and personal liability. Unlike car insurance, homeowners insurance is not required by state law. However, if you have a mortgage, your lender will require homeowners insurance to protect the investment.

Homeowners insurance covers the property from damage, referred to as insurance perils. A peril is an event that may damage your home or belongings, like theft, fire, or a storm. The type of peril coverage you have depends on the type of homeowners insurance you purchased. Common insurance perils include fire, lightning, theft, ice, snow, sleet, smoke, vandalism, and freezing.

Floods, earthquakes, government seizures, mudslides, ordinance updates, sewer backups, and sinkholes are all perils that won't be covered by homeowners insurance, according to Hippo Insurance. Those will require add-on coverage using a rider policy.

*Available as add-on coverage if not part of policy

**Flood insurance is available through the NFIP and approved insurers

For FEMA-backed flood insurance policies through the NFIP, there is no basement coverage. Flood insurance is only for water that comes in above ground level. Blust said that flood insurance offers virtually no coverage for homes with anything below ground— like basements.

Standard homeowners policies have water damage included, but for basements much depends on how the water got there. Was the water due to a frozen pipe or damage from improper maintenance of appliances and the home? He noted that NFIP provides little coverage for water floods from streets. Again, this may be covered under your standard homeowners policy for water damage, but check with your agent.

There's a difference in how flood insurance pays out, too

Blust said that the flood insurance application process is more detailed and time-consuming than getting a homeowners insurance policy. He also noted that a flood insurance policy's coverage is different from the coverage you get with a standard homeowners insurance policy.

Homeowners insurance policies typically use "replacement cost" when paying out for covered damage. Replacement cost is the cost to replace the item with a new or used product. However, flood insurance is based on the "actual cash value" (ACV) of property damaged. For example, if a leather sofa is damaged by flood, the actual cash value takes into consideration depreciation of the item. Actual cash value is usually lower than the replacement cost value.

Blust said that actual cash value is default for flood insurance policies, but you can request "replacement cost" value as an add-on. This should be done before signing your flood insurance policy, as it will increase your premium costs based on the difference between the replacement cost value and the actual cash value. It will vary based on the value of your belongings. It may require creating a home inventory and providing a list of the appraised value. However, it varies with flood insurance providers.

What is the National Flood Insurance Program (NFIP)?

FEMA created the National Flood Insurance Program (NFIP) in the 1960s because conventional insurers wouldn't provide flood coverage to homeowners. This led to significant home foreclosures from flood damage. Blust said floods happen in all 50 states every year and the most catastrophic events with flooding are hurricanes — more than a river or levee.

FEMA uses flood maps that identify flood zones to provide coverage for homeowners. The FDIC requires homeowners to purchase flood insurance if you're in the highest-risk flood zone. Flood zones vary based on region and locality. FEMA has a website for flood maps where you can enter your location and see what zone you are in. As weather patterns change, FEMA updates flood maps.

In the 1980s, FEMA allowed insurance companies to offer flood insurance known as "Write Your Own Flood" policies. Blust said that these programs are typically connected to FEMA, but outsourced. For example, National Flood Services is the largest flood service operator administered on behalf of insurers and FEMA.

Do you need flood insurance?

If you are in a high-risk flood zone, you're required to purchase flood coverage identical to or better than what is offered by FEMA through NFIP. However, Blust said only around 14% of structures in the US are in a designated high-risk flood zone. Still, due to climate and weather changes, we're seeing more storms and damage happening outside target flood areas.

Blust noted that although most homes are not in high-risk flood zones, homeowners are three times more likely to incur a water event than a fire event over the life of a home. Yet, only 12% of homeowners are covered for flood protection, while a larger number of homeowners have fire coverage.

Blust noted that homeowners have a false sense of security if there have been no previous floods. He said storms are increasing in frequency and intensity due to climate change — for instance, the typical pattern of hurricanes is changing.

For example, Blust said Hurricane Harvey's damage to Houston was five miles off the coast, where it had never flooded in the past five years and most of those homeowners didn't have flood insurance. If 20 homes were damaged and only five homes had flood insurance, it could greatly impact the community, with empty neighborhoods and businesses that aren't able to bounce back.

Homeowners who live outside of high-risk flood zones and do not have flood insurance will pay for damage out-of-pocket because flood damage isn't covered under homeowners insurance. According to Blust, one inch of flood damage alone can cost a household up to $20,000.

How much does flood insurance cost?

The average annual homeowners insurance premium in the United States in 2017 was $1,211, according to the National Association of Insurance Commissioners (NAIC). Flood insurance will be an addition to your homeowners insurance policy.

Blust said the average cost of a NFIP policy is $700 per year, which may seem like a high expense, but again, one inch of flood damage alone can cost up to $20,000 to repair. He said the average flood premium is around $830 annually from an approved flood insurance provider, but a preferred risk policy with a $250,000 coverage limit is around $500.

Renters flood insurance is available through approved National Flood Insurance Program (NFIP) providers like the National Flood Services for around $99 a year.

Factors that determine your flood insurance premium include proximity to water and whether or not the structure is elevated. The closer you are to water increases your rate.

How do I get flood insurance?

Due to the risk, most homeowners insurance providers do not provide flood insurance. Ask your homeowners insurance provider if they provide flood insurance. If not, you will need to get flood insurance through approved NFIP providers like the National Flood Services. Check the NFIP website for flood insurance providers.

If you are unclear about your homeowners insurance peril coverage, contact your homeowners insurance provider, especially if you live in disaster-prone areas. It is recommended that you review your policy coverage yearly.

Subscribe to Business Insider's Financial Insights Newsletter

This Business Insider article was legally licensed by AdvisorStream