Jacob Lorinc

July 14, 2021

Some Canadians have amassed significant savings since the COVID-19 pandemic began. From eating at home to avoiding travel, households are estimated to have saved more than $170 billion in excess cash. What to do with this extra money?

For many homeowners, now’s the time to think about major financial priorities. Do you focus on paying off a mortgage, or do you accelerate your investing for retirement?

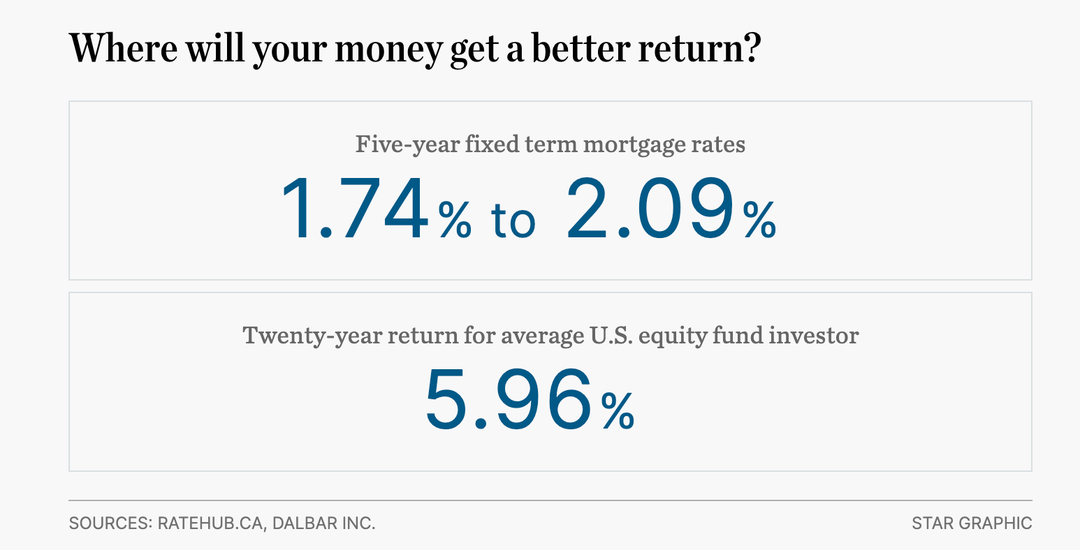

There’s no right or wrong answer, says Dan Hallett, vice-president of research at HighView Financial Group. On the one hand, interest rates are at historic lows, hovering around two per cent, meaning now’s a good time to get ahead on payments for your home. But equities have been rising fast, and stock markets have well-surpassed their pre-pandemic levels — so boosting your investment portfolio might not be such a bad idea, either.

Everyone’s financial situation is different, but this is a pretty good time to get ahead on mortgage payments, says Hallett. “If your mortgage is oversized, and it’s looking like it will take a while to pay off, maybe that’s the place to put your money, given how low interest rates are.”

And future returns on financial assets, meanwhile, which typically hover around five or six per cent, could be lower in the coming years, he says.