By Joe Pinsker and Callum Borchers

Oct. 13, 2023

Across the country, people want to find better jobs, bigger homes and even nicer gyms. But making any of those leaps right now could leave them worse off financially in the long run.

PHOTO ILLUSTRATION BY RACHEL MENDELSON/THE WALL STREET JOURNAL, ISTOCK (5)

Low interest rates, high salaries and membership discounts scored before and during the pandemic often can’t be matched today, binding people in golden handcuffs. Many feel comfortable, but stuck.

Some who job-hopped when the labor market was at its tightest negotiated hefty raises or work-from-home arrangements that other employers might not match today. Homeowners eager to reach for another rung on the property ladder are staying put because they aren’t willing to let go of sub-3% mortgages that are unlikely to be available again soon, if ever. Today’s higher rates effectively limit their budgets, putting more expensive homes further out of reach.

While economists say the constant pursuit of new and better opportunities is a sign of a strong economy, it can also fuel inflation. Businesses paid premiums for talent in recent years, and flush workers helped drive up prices of homes, cars and other goods. As the Federal Reserve tries to stamp out inflation by raising interest rates, many consumers have less buying power and are holding on to what they have.

“That is what the Fed is trying to do. That’s the point of raising interest rates,” says Dana M. Peterson, chief economist at the Conference Board, a business-research nonprofit. If people continue to feel stuck even after the Fed eventually lowers rates, that’s when there would be cause for worry, Peterson says.

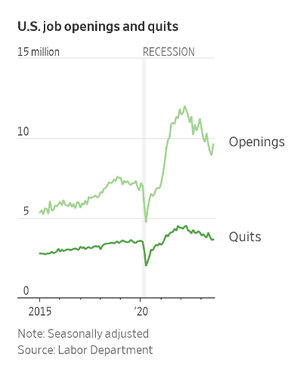

Home sales are now mired in the worst slump in more than a decade and workers are quitting jobs at a rate that has slowed to the prepandemic norm.

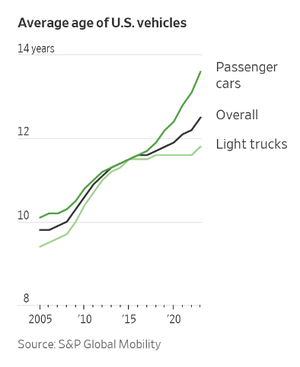

Pessimistic Americans are driving from the same old homes to the same old jobs in the same old cars. The average age of cars and light trucks in the U.S. is at a record 12½ years, according to S&P Global Mobility. Kelley Blue Book reports new-vehicle prices have plateaued at 25% above prepandemic levels and inventory shortages persist for certain models, stalling some trade-ins.

In matters big and small, people feel they cannot improve on their current situations. They’re mentally or emotionally ready for a change but can’t bring themselves to walk away.

“It’s very hard to tell whether the grass is actually greener,” says Justin Sousa, a software engineer in Massachusetts.

In more than six years at his company, Sousa periodically craved new challenges and entertained other offers. He says his employer always countered the poaching attempts and sometimes awarded bonuses to keep him. The promise of another headhunter dangling a raise never felt far off until the recent spate of tech-sector layoffs.

So Sousa, 36, is standing pat. He figures a job change now would be a lateral move, and he has no plan to test the market, especially with twins on the way.

Jumping ship is usually the best way to earn more money, but job switchers’ wage-growth advantage over those who hang around is the smallest in three years at 0.4 percentage points, according to the Federal Reserve Bank of Atlanta. Wage hikes are harder to come by in many industries. Across 20,000 job titles on ZipRecruiter, the average advertised salary for most roles is less than it was last year.

Those who are locked into favorable positions won’t get much sympathy, though there can be collateral damage. People hoping to buy houses for the first time have limited options when existing owners can’t afford to trade up from their starter homes. Ambitious workers can find themselves blocked from promotions if the people above them don’t move on.

Fewer innovations spring from startups when would-be entrepreneurs opt to play it safe in their current jobs. Applications to form new businesses dipped 0.9% in August to a seasonally adjusted total of 466,163, according to the Census Bureau. That’s more than 15% below a peak in the summer of 2020.

For many, things haven’t necessarily taken a turn for the worse. Rather, their grip is slipping on a piece of the American dream: the feeling that something better is achievable.

Home is where the bargain is

Many homeowners feel trapped by their low mortgage rates. John Dealbreuin is looking to make the most of the house he feels stuck in.

Dealbreuin, a 44-year-old early retiree in South San Francisco, wants a bigger house so that he can invite his parents, ages 78 and 83, to move from India to live with him. But he’s reluctant to part with the home he bought a decade ago—and the 3.3% mortgage he carries on it.

Dealbreuin decided to stay put and build a 300-square-foot guest unit in his backyard. If his parents ultimately decide to remain in India, he says: “I’d be disappointed that I wouldn’t be here with them, but I don’t look at this as money lost because it’s still adding value to my property.”

The current average rate for a 30-year, fixed-rate mortgage is 7.57%, according to Freddie Mac. In the second quarter this year, 60% of homeowners with a mortgage had a rate of 4% or lower, according to an analysis of government data by First American Financial Corporation.

The larger the gap between homeowners’ mortgage rates and the going rate for a new loan, the less likely they are to move, according to a recent working paper from researchers at the University of Illinois and the University of Pennsylvania.

Their findings suggest that people with 3% mortgages today could be about 30% to 40% less likely to move than they otherwise would be, says Lu Liu, an author of the paper and a finance professor at Penn’s Wharton School.

When homeowners don’t move, that limits the number of houses that are bought and sold. And Liu found that those who locked in low mortgage rates are less likely to move in response to wage growth in nearby areas, potentially making the labor market less dynamic.

Not all that glitters…

Some cuffs are merely gold-plated.

Mario Moreta’s monthly gym membership in New York City would cost about $200 if he joined today, but he is grandfathered in at $85 a month, a steep discount even when he got it years ago. It feels like a steal—except when the hot water is out in the showers, live DJs blare music he dislikes, and he has to wake up two hours early to go in the morning and avoid the evening crowds.

“I’m getting what I’m paying for,” says the 29-year-old finance manager at a retail brand. “It’s not meant for me to go to a spa every day.”

Though it can often be financially prudent to stay the course, people tend to overvalue things that belong to them, says Annie Duke, a former professional poker player and author of “Quit: The Power of Knowing When to Walk Away.”

Behavioral scientists call this the endowment effect. Whether a coffee mug or a house, Duke says, “we have this issue of not wanting to give it up.”

She recommends asking two questions to improve decision making: How much would you be willing to pay to be happier in this area of your life? And, if you were considering entering an arrangement just like this one today, knowing all you know now, would you choose it?

Write to Joe Pinsker at joe.pinsker@wsj.com and Callum Borchers at callum.borchers@wsj.com

Dow Jones & Company, Inc.